For many Americans, the question of when to take Social Security is one of the biggest retirement decisions they will ever make. You can claim retirement benefits as early as age 62, but doing so usually means accepting a permanently reduced monthly benefit compared with waiting until full retirement age or age 70. That tradeoff makes the decision feel high-stakes—and for good reason.

The standard advice often sounds simple: “Delay Social Security as long as possible.” In many cases, that can be excellent advice. Waiting can increase your monthly benefit, and the increase continues until age 70. But retirement planning is not only about maximizing a monthly check. It is also about cash flow, health, family needs, taxes, work plans, investment risk, and quality of life.

For some retirees, taking Social Security at 62 can be a rational, strategic, and even empowering decision.

This article explores five reasons to take Social Security at age 62, along with the tradeoffs you should understand before filing.

First, What Happens If You Claim Social Security at 62?

Age 62 is the earliest age most workers can begin receiving Social Security retirement benefits. However, claiming early reduces your monthly payment because you are starting benefits before your full retirement age.

For many people born in 1960 or later, full retirement age is 67. If your full retirement age is 67 and you claim at 62, you are claiming 60 months early. That can reduce your retirement benefit to about 70% of your full retirement age benefit, meaning a roughly 30% permanent reduction before cost-of-living adjustments.

That reduction is important. It should not be brushed aside. But it also does not automatically mean claiming at 62 is a mistake.

The better question is this:

Does taking a smaller check sooner improve your overall retirement plan more than waiting for a larger check later?

For some people, the answer is yes.

Reason 1: You Need Income Now and Want to Reduce Financial Stress

The most obvious reason to take Social Security at 62 is also one of the most legitimate: you need the income.

Not everyone reaches their early 60s with a large investment portfolio, a pension, rental income, or a high-paying job they can comfortably keep. Some people are laid off in their early 60s. Others are caring for a spouse, helping adult children, dealing with health expenses, or simply burned out after decades of physically or emotionally demanding work.

In these situations, Social Security can serve its original purpose: providing a reliable income floor.

Claiming at 62 may help you:

- Pay essential living expenses.

- Reduce credit card debt or avoid new debt.

- Leave a stressful or unhealthy job.

- Bridge the gap until other income sources begin.

- Preserve dignity and independence in early retirement.

Financial planning advice often assumes people have the flexibility to delay. But flexibility is not universal. If the choice is between taking Social Security at 62 or draining emergency savings, taking on high-interest debt, or staying in work that is harming your health, early claiming may be the more practical option.

There is also an emotional component. Retirement is not only a math problem. If claiming at 62 gives you breathing room, lowers anxiety, and helps you create a stable monthly budget, that value matters.

Cash Flow Can Be More Important Than Maximization

A higher monthly benefit at age 67 or 70 is valuable only if you can comfortably get there. For retirees with limited savings, delaying Social Security may require drawing heavily from investments or cash reserves. That can leave them vulnerable to market downturns, unexpected medical costs, home repairs, or inflation.

Taking Social Security at 62 can provide predictable monthly income and reduce pressure on other assets. While the monthly check is smaller, the earlier income may help stabilize your household finances at a time when stability matters most.

Important Caution: The Earnings Test

If you claim at 62 and continue working, you need to understand the Social Security earnings test. If you are under full retirement age for the entire year and earn above the annual earnings limit, Social Security may withhold part of your benefits.

This does not mean working while claiming is always bad. But it does mean you should run the numbers before filing if you expect meaningful earned income before full retirement age.

Reason 2: Your Health or Family Longevity Suggests Claiming Earlier

One of the strongest reasons to take Social Security at 62 is a shorter-than-average life expectancy.

Social Security is designed so that, in a broad actuarial sense, claiming early gives you smaller checks for more years, while delaying gives you larger checks for fewer years. But individual lives do not follow averages.

If you have serious health concerns, a chronic condition, or a family history of shorter lifespans, taking benefits at 62 may allow you to receive more total value from the system during the years when you are most able to use the money.

That point is crucial. Social Security claiming is personal. A healthy retiree with long-lived parents, strong savings, and low expenses may benefit from delaying. A retiree with major health issues, limited savings, and a desire to enjoy retirement while physically able may reasonably choose age 62.

The Break-Even Question

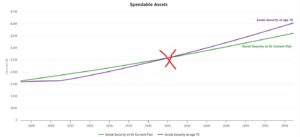

Many retirees think about a “break-even age.” This is the age at which the total dollars received by delaying benefits catches up to the total dollars received by claiming early.

For example, claiming at 62 gives you eight years of payments before age 70. Waiting until 70 gives you a larger monthly payment, but you receive nothing from Social Security during those eight years. The delayed strategy only pulls ahead if you live long enough for the larger monthly checks to make up for the payments you skipped.

The exact break-even point depends on your benefit amount, birth year, cost-of-living adjustments, taxes, and other variables. But the basic idea is straightforward: if you do not expect to live well into retirement, early claiming can make financial sense.

Quality of Life Matters

There is another factor that spreadsheets often miss: your most active retirement years may be your early 60s.

Money received at 62 may help you travel, visit family, pursue hobbies, move closer to loved ones, or reduce work hours while you still have the health and energy to enjoy those choices. A larger check at 70 is useful, but it may not replace opportunities missed between 62 and 70.

This does not mean everyone should claim early. It means health, mobility, family history, and personal goals deserve a central place in the decision.

Reason 3: You Want to Retire Early Without Draining Your Investments

Another compelling reason to take Social Security at 62 is to reduce withdrawals from your retirement portfolio.

If you retire before full retirement age, you may need income from savings, investments, part-time work, a pension, or Social Security. Without Social Security, you might need to pull more heavily from a 401(k), IRA, brokerage account, or cash reserves.

That can be risky, especially if the market is down during your first years of retirement.

Sequence-of-Returns Risk

Retirement planners often talk about sequence-of-returns risk. This is the danger of experiencing poor investment returns early in retirement while you are simultaneously withdrawing from your portfolio. Losses early in retirement can be especially damaging because your portfolio has less time and less principal available to recover.

Claiming Social Security at 62 can reduce the amount you need to withdraw from investments during those early years. Even a smaller monthly Social Security check may help cover groceries, utilities, insurance premiums, property taxes, or other core expenses.

This can be particularly useful if:

- Markets are volatile when you retire.

- Your portfolio is smaller than planned.

- You want to avoid selling investments during a downturn.

- You have a conservative risk tolerance.

- You want more predictable income and less dependence on market performance.

Early Social Security as a Portfolio Buffer

Think of early Social Security as a buffer. It may not fully fund your retirement, but it can reduce the burden on your portfolio. That can help you preserve assets for later years, emergencies, healthcare expenses, or legacy goals.

For example, suppose you need $4,000 per month to cover expenses. Without Social Security, you might need to withdraw the full amount from savings. With a $1,600 monthly Social Security benefit, your portfolio only needs to provide $2,400 per month. That difference could matter significantly over several years.

Of course, delaying Social Security may produce a higher guaranteed benefit later. For some retirees, using savings first and delaying benefits can be a strong strategy. But for others, especially those with smaller portfolios or high concern about market risk, claiming at 62 can help create a more balanced retirement income plan.

Reason 4: You Want More Freedom, Flexibility, and Control Over Your Time

Taking Social Security at 62 may allow you to design a retirement that is not strictly “all work” or “all retirement.”

Many people in their early 60s do not necessarily want to stop working forever. They may want to work part time, consult, start a small business, help with grandchildren, volunteer, care for aging parents, or shift into lower-stress work.

Social Security can make that transition easier.

A Bridge to Semi-Retirement

Claiming at 62 can support a semi-retirement strategy. Instead of working full time until 67 or 70, you might use Social Security to reduce your required work hours.

That can be especially attractive if your current job is physically demanding. Construction workers, nurses, warehouse employees, teachers, first responders, restaurant workers, caregivers, and tradespeople may find it difficult to continue full-time work deep into their 60s. For them, taking Social Security at 62 may be less about “retiring early” and more about making work sustainable.

A smaller Social Security benefit combined with part-time income may provide enough cash flow to cover expenses while giving you back time and energy.

Watch the Earnings Limit

Again, the earnings test matters. If you claim before full retirement age and earn above the annual limit, some benefits may be withheld. Once you reach full retirement age, there is no limit on how much you can earn while receiving Social Security benefits.

This makes early claiming more attractive for people who plan to stop working, work only modestly, or earn below the limit. It may be less attractive for people who expect to keep a high income until full retirement age.

Flexibility Has Real Value

Financial advisors often focus on lifetime benefit maximization. That is important. But retirement satisfaction often depends on flexibility.

Taking Social Security at 62 may help you:

- Leave a job you no longer enjoy.

- Spend more time with a spouse or grandchildren.

- Care for a loved one without fully sacrificing income.

- Move to a lower-cost area.

- Start a passion project.

- Reduce work stress before health problems worsen.

There is no universal formula for valuing time. But for many people, the ability to reclaim time in their early 60s is worth more than a larger check later.

Reason 5: You Are Concerned About Uncertainty and Prefer Money Sooner

Some retirees take Social Security at 62 because they prefer the certainty of receiving benefits now.

This is not always the mathematically optimal choice. But it is understandable. Retirement planning involves uncertainty around health, markets, inflation, taxes, family needs, and future Social Security policy.

Social Security remains a foundational retirement program, but many Americans worry about long-term program funding and potential legislative changes. While current retirees and near-retirees should be careful not to make fear-based decisions, uncertainty can influence how people think about claiming.

“Money Now” Can Feel More Secure Than “Money Later”

For some households, taking benefits at 62 provides psychological security. The monthly payment arrives. The budget becomes clearer. The retiree feels less dependent on investment markets, employers, or future policy decisions.

Peace of mind is not trivial. Stress can affect health, relationships, and decision-making. If claiming early helps you feel more stable and confident, that emotional benefit belongs in the calculation.

Early Benefits Can Support Family Priorities

Some people also claim early because they have family priorities that matter now. They may want to help a spouse retire, support a disabled family member, spend time with grandchildren, or fund experiences while the family is healthy and together.

A purely financial analysis might say waiting is better. A life-centered analysis might say the earlier income helps support the people and experiences that matter most.

The Tradeoff Is Permanent

That said, the tradeoff is real. Claiming at 62 usually locks in a lower monthly benefit for life, aside from future cost-of-living adjustments.

If you live into your late 80s or 90s, delaying could provide significantly more lifetime income. This is especially important for retirees who expect Social Security to be their main source of income later in life.

When Taking Social Security at 62 May Be a Good Idea

Taking Social Security at 62 may make sense if several of the following apply:

- You need income immediately.

- You have stopped working or earn below the earnings-test limit.

- You have health concerns or shorter family longevity.

- You want to avoid drawing too heavily from investments.

- You are retiring from physically demanding work.

- You value time and flexibility more than maximum lifetime benefits.

- You have a spouse with a stronger benefit record or other household income.

- You have run the numbers and understand the permanent reduction.

This is where the decision becomes less about age and more about context.

Age 62 is not automatically “too early.” Age 70 is not automatically “best.” The right claiming age is the one that fits your health, finances, work plans, spouse, taxes, and retirement goals.

Tax Considerations Before Claiming at 62

Taxes should also be part of the decision. Social Security benefits may be taxable depending on your combined income.

This does not mean you lose 85% of your benefit. It means up to 85% of your benefit may be included in taxable income. The actual tax cost depends on your broader income, deductions, and tax bracket.

Claiming at 62 could increase taxable income if you also have wages, pension income, IRA withdrawals, or investment income. On the other hand, a smaller early benefit may create less taxable Social Security income than a larger delayed benefit later. The best approach depends on your retirement income timeline.

A tax professional or financial planner can help compare scenarios, especially if you are planning Roth conversions, IRA withdrawals, pension elections, or part-time work.

Medicare Reminder: Social Security at 62 Does Not Mean Medicare at 62

One common misconception is that claiming Social Security at 62 also starts Medicare. In most cases, it does not.

Medicare generally begins at age 65 for most people. This matters because health insurance can be one of the biggest costs for early retirees. If you leave work at 62, you may need coverage through a spouse’s plan, COBRA, the Affordable Care Act marketplace, retiree health benefits, or another source until Medicare eligibility.

Before claiming Social Security at 62, make sure your healthcare plan is clear.

How to Decide Whether Taking Social Security at 62 Is Right for You

Before filing, ask yourself these questions:

1. What Is My Full Retirement Age Benefit?

Create or review your Social Security account and compare claiming ages. Look at your estimated benefit at 62, full retirement age, and 70.

2. How Long Do I Realistically Expect to Live?

No one knows the answer with certainty. Still, your health, family history, lifestyle, and medical conditions should inform your decision.

3. Will I Keep Working?

If you will earn above the earnings-test limit before full retirement age, early claiming may be less attractive.

4. How Much Will I Need to Withdraw From Savings If I Delay?

Delaying can increase your monthly benefit, but it may require larger portfolio withdrawals in the meantime.

5. How Does My Spouse Fit Into the Decision?

For married couples, claiming strategies should be coordinated. The higher earner’s claiming age can affect survivor income.

6. What Do I Value Most: Higher Lifetime Income or Earlier Freedom?

Some people want maximum guaranteed income later. Others want more time, flexibility, and reduced stress now. Both priorities are valid.

FAQ: Taking Social Security at 62

Is It a Mistake to Take Social Security at 62?

Not necessarily. It can be a mistake if you claim early without understanding the permanent reduction, earnings test, tax impact, or survivor implications. But it can be a smart decision if you need income, have health concerns, want to retire from demanding work, or need to protect your savings.

How Much Do You Lose by Taking Social Security at 62?

The reduction depends on your full retirement age. For people born in 1960 or later, full retirement age is 67, and claiming at 62 generally results in a benefit around 70% of the full retirement age amount.

Can I Work and Collect Social Security at 62?

Yes, but if you are under full retirement age, the earnings test can reduce your current benefits if your earnings exceed the annual limit.

Will My Benefit Increase Later If I Claim at 62?

Your benefit can receive cost-of-living adjustments, but the early-claiming reduction generally remains built into your benefit. If benefits are withheld because of the earnings test, Social Security may recalculate your benefit at full retirement age to account for months in which benefits were withheld.

Is It Better to Take Social Security at 62 or Wait Until 67?

It depends. Waiting until 67 gives you a higher monthly benefit. Taking benefits at 62 gives you income sooner. The better choice depends on your health, income needs, savings, work plans, taxes, and life expectancy.

Final Thoughts: Taking Social Security at 62 Can Be Smart for the Right Person

The decision to take Social Security at 62 should never be made casually. Claiming early usually means accepting a permanently reduced monthly benefit, and that can affect your income for the rest of your life.

But it is equally wrong to say that everyone should delay.

There are strong reasons to take Social Security at age 62. You may need income now. You may have health concerns. You may want to retire from demanding work. You may want to reduce withdrawals from your portfolio. You may value time, flexibility, and peace of mind more than maximizing a future monthly check.

The smartest Social Security strategy is not the one that looks best in a generic calculator. It is the one that fits your actual life.

Before filing, compare your estimated benefits, consider taxes and healthcare, understand the earnings test, and think carefully about your spouse or dependents. Then make the decision that gives you the best combination of financial security and quality of life.

Bottom line: Taking Social Security at 62 is not right for everyone—but for the right retiree, it can be a practical and well-reasoned choice.