How Do I Turn My Savings Into Retirement Income?

Saving for retirement is one challenge. Turning those savings into steady retirement income is a completely different challenge.

When you’re working, your paycheck solves a lot of problems. It shows up on a schedule. Taxes are usually withheld automatically. You know roughly how much you can spend. But when you retire, that paycheck stops, and suddenly your savings have to become the paycheck. That’s where many people feel the most uncertainty.

In this article, we’ll walk through five smart ways to think about turning your savings into retirement income. The goal isn’t to find one perfect strategy. The goal is to build a system that helps you pay your bills, enjoy your life, manage taxes, reduce investment stress, and avoid making emotional decisions during bad markets.

Key Point / Summary

Turning savings into retirement income means creating a plan for how money will move from your accounts into your checking account in a reliable, tax-aware, and sustainable way.

Short on time? Here are the five key steps to follow:

- Know your retirement income gap.

- Separate predictable income from investment-based income.

- Create a withdrawal strategy from your accounts.

- Build a cash reserve and market downturn plan.

- Review and adjust your income plan every year.

The mistake many retirees make is assuming that having a large account balance automatically means they have a retirement income plan.

It doesn’t.

A $1 million portfolio, $750,000 portfolio, or $500,000 portfolio is not the same thing as a monthly paycheck. You still need to decide how much to withdraw, which accounts to use first, how to handle taxes, how much risk to take, and what happens when markets are down.

If you’re within a few years of retirement, this is exactly what a Retirement Readiness Review is designed to help with. We take your current numbers, define your goals, test different strategies, and help you see how your savings could become retirement income without forcing you to move your money or buy financial products.

How Do I Turn My Savings Into Retirement Income?

You turn savings into retirement income by building a withdrawal system around your spending needs, guaranteed income sources, tax situation, investment risk, and long-term goals.

That may sound complicated, but the basic idea is simple:

You need to know how much income you need, how much is already covered by predictable sources, and how much must come from your savings.

For most retirees, income may come from several places:

- Social Security

- Pensions

- 401(k)s

- IRAs

- Roth IRAs

- Taxable investment accounts

- Cash savings

- Annuities

- Rental income

- Part-time work

- Business income

The key is coordinating these income sources so they work together.

Retirement income planning is not just about pulling money randomly from whichever account is easiest. That can create unnecessary taxes, increase investment risk, or cause you to spend down accounts too quickly.

The better approach is to build a paycheck system before retirement begins.

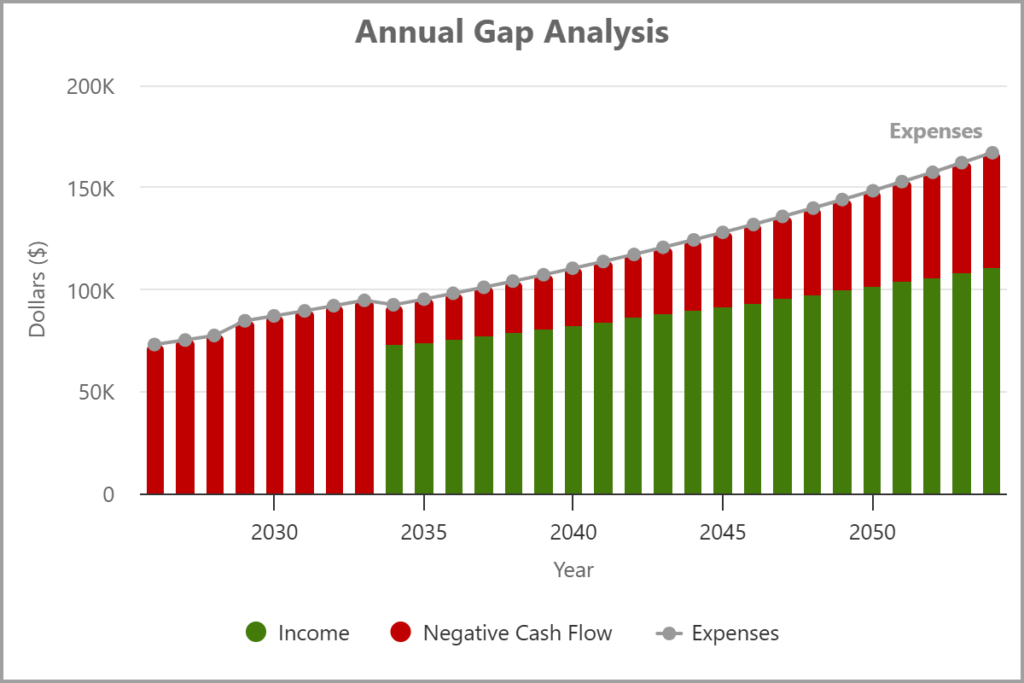

1. Know Your Retirement Income Gap

The first step in turning savings into retirement income is knowing your retirement income gap.

Your income gap is the difference between the income you need and the predictable income you already have.

For example, let’s say you want $7,000 per month in retirement income. If Social Security and pensions provide $4,500 per month, your income gap is $2,500 per month. That $2,500 has to come from somewhere, usually your savings and investments.

This is one of the most important numbers in your retirement plan.

Many people make the mistake of starting with their account balance. They say, “I have $800,000 saved. Is that enough?” But that question is incomplete. The better question is, “How much income does my $800,000 need to produce every month, and for how long?”

That changes everything.

A person with $800,000 saved and a $1,500 monthly income gap may be in a very different position than someone with $800,000 saved and a $5,000 monthly income gap. Same savings. Completely different retirement pressure.

To calculate your income gap, start with your retirement expenses.

Break them into two categories:

Essential expenses are the bills that must be paid.

These may include:

- Housing

- Utilities

- Groceries

- Insurance

- Property taxes

- Transportation

- Healthcare

- Basic home maintenance

- Debt payments

Lifestyle expenses are the things that make retirement enjoyable.

These may include:

- Travel

- Hobbies

- Dining out

- Entertainment

- Gifts

- Home improvements

- Family support

- Charitable giving

- Major purchases

This matters because not all spending has the same priority.

If predictable income covers most or all of your essential expenses, retirement may feel more stable. If your investments must cover basic bills every month, you need a more thoughtful withdrawal and risk management strategy.

Once you know your monthly spending target, subtract your predictable income sources.

Predictable income may include:

- Social Security

- Pension payments

- Annuity income

- Rental income, if reliable

- Part-time work, if planned

The remaining amount is your income gap.

That gap is the job your savings must perform.

This is the point where retirement planning becomes real. Your savings are no longer just a balance on a statement. They become a tool designed to fill a monthly need.

A Retirement Readiness Review can help you calculate your income gap and test whether your savings can realistically support it.

- Start with monthly expenses, not account balances.

- Separate essential expenses from lifestyle expenses.

- Add up predictable retirement income sources.

- Calculate the gap that savings must cover.

- The smaller the gap, the less pressure on your investments.

This step may seem straight forward but many of my client had difficulty figuring out where their money was going each month. Tracking every expense that occurs monthly, annually, or quarterly can seem overwhelming. However, I have found a tool called Monarch Money that can be very helpful in the task of confidently figuring out your monthly spending. You simply link your spending accounts, like your checking and credit cards and Monarch will organize your spending much easier than spreadsheets alone.

I don’t receive any compensation from Monarch; I have just found this tool to be very helpful to people who have a difficult time figuring out their spending patterns.

2. Separate Predictable Income From Investment-Based Variable Income

The second step is understanding the difference between predictable income and investment-based income.

This is important because not all retirement income works the same way.

Predictable income is income you can generally count on for a specific amount or time period. Social Security and pensions are common examples. Some annuities may also provide predictable lifetime income.

Investment-based income is different. It comes from accounts that fluctuate in value, such as 401(k)s, IRAs, Roth IRAs, and taxable investment accounts.

Investment-based income can be very powerful, but it’s not guaranteed. The account value can go up or down. The income you take from it has to be managed carefully because taking too much, especially during bad markets, can damage the plan.

This is why retirees often feel nervous about income from investments.

When you’re working and contributing to your 401(k), market downturns are uncomfortable but often manageable. You’re still getting a paycheck. You may even be buying investments at lower prices.

But when you’re retired, the situation changes. You may be selling investments to create income. If the market drops and you still need withdrawals, you could be forced to sell at lower values. That can create stress and potentially reduce how long your money lasts.

That doesn’t mean investments are bad for retirement income.

Not at all.

Investments can help your money grow, keep up with inflation, provide flexibility, and leave money for emergencies or heirs. But investment income needs a plan.

One helpful way to think about retirement income is to divide your expenses into two buckets:

Needs and wants.

Your needs are essential expenses. Your wants are lifestyle expenses.

Some retirees prefer to cover as many needs as possible with predictable income. Then they use investment-based income for travel, hobbies, upgrades, and flexible spending.

That doesn’t mean everyone needs an annuity or pension. It simply means you should understand how much of your lifestyle depends on market performance.

For example, if Social Security covers your basic bills and your investment withdrawals mainly pay for travel, you may have flexibility during a downturn. You could reduce travel temporarily if markets are bad.

But if your investments are paying your mortgage, food, utilities, and healthcare, then downturns may feel much more serious.

This is why retirement income planning is not just about maximizing returns. It’s about matching the right income source to the right expense.

Predictable income can provide stability.

Investment income can provide growth and flexibility.

A good retirement plan often uses both.

The key is understanding which part of your income is dependable and which part depends on market performance.

- Predictable income may include Social Security, pensions, and some annuities.

- Investment income may come from 401(k)s, IRAs, Roth IRAs, and taxable accounts.

- Essential expenses may be better matched with more dependable income sources.

- Lifestyle expenses may have more flexibility during bad markets.

- A strong retirement income plan balances stability, growth, and flexibility.

3. Create a Withdrawal Strategy From Your Accounts

The third step is creating a withdrawal strategy.

This is where many retirees get stuck.

They’ve spent years saving into different accounts, but they haven’t thought through which accounts to spend from first. Should they use cash? Taxable accounts? Traditional IRAs? Roth IRAs? 401(k)s? Should they take Social Security early to avoid withdrawals? Should they delay Social Security and use investments first?

These choices can have a major impact on taxes, investment growth, required minimum distributions, Medicare premiums, and how long your money lasts.

A withdrawal strategy should answer several questions:

- Which account do I use first?

- How much do I withdraw each month?

- How much should I withhold for taxes?

- Should withdrawals be monthly, quarterly, or annual?

- Should I spend taxable money before IRA money?

- Should I preserve Roth accounts for later?

- Should I do Roth conversions before required minimum distributions begin?

- How does Social Security timing affect withdrawals?

- How do I avoid selling investments during a downturn?

There is no single withdrawal order that works for everyone.

Some people may benefit from spending taxable accounts first. Others may benefit from taking IRA withdrawals earlier to manage future taxes. Some may want to preserve Roth accounts as long as possible. Others may use Roth money strategically to avoid pushing income too high in certain years.

The important point is this: withdrawal order matters.

For example, traditional IRA and 401(k) withdrawals are generally taxable as ordinary income. Roth IRA withdrawals may be tax-free if requirements are met. Taxable brokerage accounts may create capital gains or losses depending on what is sold. Cash savings may not create much tax impact but can run out quickly if overused.

If you pull money randomly, you may accidentally create higher taxes than necessary.

You may also create future problems.

For example, some retirees avoid touching their IRA because they don’t want to pay taxes. That sounds reasonable. But eventually, required minimum distributions may force money out. If the IRA has grown large, those forced withdrawals may create higher taxable income later.

In some cases, taking controlled IRA withdrawals earlier in retirement may be worth considering. In other cases, it may not.

This is why tax planning and income planning need to work together.

Your withdrawal strategy should also match your investment allocation.

If you need $60,000 from your portfolio this year, where will it come from? Cash? Bonds? Dividends? Selling stock funds? A combination?

You don’t want to decide that during a market panic. You want a system in advance.

A simple retirement paycheck strategy may look like this:

- Keep a cash reserve for near-term spending.

- Refill cash from investments on a schedule.

- Use taxable accounts, IRA accounts, and Roth accounts intentionally.

- Review taxes before year-end.

- Adjust withdrawals annually based on performance and spending.

This type of system helps retirees feel more in control.

Instead of wondering, “Can I spend this?” you can say, “This is the income plan we tested.”

That’s a very different mindset.

A Retirement Readiness Review can help you compare different withdrawal strategies before you retire so you can see the trade-offs clearly.

- Decide which accounts will fund retirement income.

- Coordinate withdrawals with taxes.

- Understand how Social Security timing affects your portfolio.

- Avoid random withdrawals without a strategy.

- Review the withdrawal plan every year.

4. Build a Cash Reserve and Market Downturn Plan

The fourth step is building a cash reserve and market downturn plan.

This is critical because markets will drop at some point during retirement. The question is not whether it will happen. The question is whether you’ll have a plan when it does.

When you’re retired, market downturns feel different.

During your working years, a downturn may be frustrating. But if you’re still earning income and not selling investments, you may be able to wait it out.

In retirement, you may be withdrawing from the portfolio every month. That creates a different kind of risk.

If the market drops and you’re forced to sell investments to pay bills, your portfolio may have less opportunity to recover. This is especially dangerous early in retirement because the first several years can have an outsized impact on long-term success.

That’s why retirees need a downturn strategy.

A cash reserve can help.

The purpose of cash is not to earn the highest return. The purpose of cash is to provide stability, flexibility, and confidence.

A cash reserve may help you:

- Pay bills during market declines.

- Avoid selling investments at a bad time.

- Sleep better during volatility.

- Handle emergency expenses.

- Fund planned large purchases.

- Reduce emotional decision-making.

How much cash should you hold?

There’s no perfect answer. Some retirees are comfortable with six to twelve months of expenses. Others prefer one to three years of portfolio withdrawals in cash or conservative assets. The right amount depends on your guaranteed income, spending needs, risk tolerance, portfolio size, and comfort level.

Too little cash can make you vulnerable.

Too much cash can create other problems. Cash may not keep up with inflation over long periods. If you hold too much, your overall portfolio may not grow enough to support a long retirement.

So, the goal is balance.

You want enough cash to provide breathing room, but not so much that you damage long-term growth.

A downturn plan should also define what you’ll do when markets fall.

For example:

- Will you pause large discretionary purchases?

- Will you reduce travel temporarily?

- Will you spend from cash instead of selling investments?

- Will you rebalance the portfolio?

- Will you delay inflation adjustments to withdrawals?

- Will you review the plan before making changes?

- Will you have a rule for when to restart normal withdrawals?

These decisions are much easier to make before the market drops.

When people don’t have a plan, they often react emotionally. They may sell too much, stop investing, cancel a good strategy, or make permanent changes based on temporary fear.

A good downturn plan doesn’t eliminate discomfort. But it gives you a playbook.

That playbook is one of the most important parts of turning savings into income. Retirement income is not just about good years. It’s about surviving bad years without destroying the plan.

A Retirement Readiness Review can help stress-test your income strategy against market downturns before retirement begins.

- Markets will drop at some point during retirement.

- Cash reserves can help reduce forced selling during downturns.

- Too much cash can create inflation and growth risk.

- A downturn plan should be created before markets fall.

- Emotional decisions are one of the biggest threats to retirement income.

5. Review and Adjust Your Income Plan Every Year

The fifth step is reviewing and adjusting your income plan every year.

A retirement income plan is not something you create once and ignore forever.

Retirement changes. Markets change. Tax laws change. Healthcare costs change. Your spending changes. Your goals change. Your family situation may change.

That means your income plan needs regular maintenance.

Think of your retirement plan like a thermostat, not a light switch.

You don’t turn it on once and forget about it. You check it, adjust it, and make sure it’s still keeping you comfortable.

An annual retirement income review should look at several areas:

- How much did you spend last year?

- Was spending higher or lower than expected?

- How did your investments perform?

- How much income came from Social Security, pensions, or annuities?

- How much did you withdraw from savings?

- What taxes did you pay?

- Are Roth conversions worth considering?

- Are required minimum distributions coming soon?

- Has your healthcare situation changed?

- Do beneficiaries need updating?

- Are large expenses coming next year?

- Is your cash reserve still appropriate?

- Should your investment allocation be adjusted?

- Are you still comfortable with the plan?

This review is important because retirement income planning is full of trade-offs.

For example, if markets had a strong year, you may have more flexibility. You may be able to refill cash reserves, take a special trip, gift money, or rebalance investments.

If markets had a poor year, you may need to be more cautious. You might reduce discretionary spending, delay a major purchase, or use cash reserves temporarily.

If your tax situation changes, you may adjust which accounts you withdraw from.

If one spouse passes away, the entire income plan may need to be rebuilt.

If healthcare expenses rise, spending assumptions may need to change.

The point is not to constantly tinker. The point is to stay aware.

One of the worst things retirees can do is put the plan on autopilot for too long. Small issues can become big problems if ignored.

Annual reviews also help retirees spend with more confidence.

Many people are actually too afraid to spend in retirement. They worked hard to save money, and now they’re nervous about using it. A regular review can show whether spending is still on track.

That can be freeing.

If the plan is healthy, you may feel more comfortable enjoying retirement. If adjustments are needed, you can make them early.

This is why retirement income planning is both financial and emotional. People don’t just need numbers. They need confidence that the numbers still work.

A good income plan should give you permission to enjoy retirement while still protecting your future.

- Review your retirement income plan every year.

- Compare actual spending to planned spending.

- Adjust withdrawals based on markets, taxes, and life changes.

- Refill cash reserves when appropriate.

- Use annual reviews to spend with more confidence.

Conclusion

Turning savings into retirement income is one of the biggest shifts you’ll make when you retire.

During your working years, the goal was mostly to save and grow. In retirement, the goal changes. Now your money has to create income, manage taxes, handle market risk, support your lifestyle, and last for the rest of your life.

That doesn’t happen by accident.

You need to know your retirement income gap. You need to separate predictable income from investment-based income. You need a withdrawal strategy. You need a cash reserve and downturn plan. And you need to review the plan every year.

The good news is that you don’t need a perfect plan. You need a clear, tested, flexible plan.

That’s the real goal.

You want to enter retirement knowing where your paycheck will come from, how much you can spend, which accounts you’ll use, what happens if markets drop, and when to make adjustments.

If you’re within a few years of retirement and wondering how to turn your savings into income, a Retirement Readiness Review can help. We’ll look at your current numbers, define your retirement goals, test income strategies, and help you understand the trade-offs before you retire.

You don’t have to move your money. You don’t have to buy a product. You just need a clear plan for turning what you’ve saved into the income you’ll need.

FAQs

How much can I safely withdraw from my retirement savings?

There’s no one-size-fits-all answer. The amount you can safely withdraw depends on your age, spending needs, investment mix, Social Security, pensions, taxes, inflation, market performance, and how long retirement lasts. A common rule of thumb may help start the conversation, but your actual withdrawal rate should be tested using your real numbers.

Should I use Social Security or my savings first?

It depends. Taking Social Security earlier may reduce the need to withdraw from savings at first, but it may also lock in a smaller monthly benefit. Using savings first may allow Social Security to grow if you delay, but it can put more pressure on your portfolio. The right answer depends on your income needs, health, spouse, taxes, and investments.

Which retirement account should I withdraw from first?

There’s no universal order that works for everyone. Some retirees use taxable accounts first, then tax-deferred accounts, then Roth accounts. Others benefit from using IRA withdrawals earlier or doing Roth conversions. The best withdrawal order should be based on your tax situation, income needs, required minimum distributions, and long-term plan.