What Happens to Retirement Income When One Spouse Dies?

Losing a spouse is emotionally devastating. But on top of the grief, the surviving spouse often faces a second shock: retirement income may change almost immediately.

Many couples build their retirement plan around two Social Security checks, two lives, shared expenses, and joint tax filing. But when one spouse dies, some income may stop, some income may continue, taxes may change, Medicare costs may change, and the surviving spouse may still have many of the same household expenses.

In this article, we’ll walk through five important things couples should understand about retirement income after one spouse dies. The goal isn’t to scare you. The goal is to help you plan ahead so the surviving spouse isn’t left with confusion, income gaps, or avoidable financial stress.

Key Point / Summary

When one spouse dies, retirement income often changes because one Social Security check may stop, pension income may change, taxes may increase, and the surviving spouse may have fewer income sources while many expenses remain.

Short on time? Here are the five key things we’ll cover:

- One Social Security check usually goes away.

- Pension income may continue, reduce, or stop.

- The surviving spouse may face a higher tax burden.

- Investment withdrawals may need to change.

- A good retirement plan should test the surviving spouse scenario before it happens.

Social Security survivor benefits may allow a surviving spouse to receive up to 100% of the deceased spouse’s benefit if the survivor has reached full retirement age for survivors. Benefits can be lower if claimed earlier.

This is why spouse protection should be part of retirement income planning. It’s not enough to know whether the plan works while both spouses are alive. You also need to know whether it works after the first spouse dies.

If you’re within a few years of retirement, a Retirement Readiness Review can help test your income plan for both spouses and for the surviving spouse, so you can see potential gaps before they become real problems.

What Happens to Retirement Income When One Spouse Dies?

When one spouse dies, household income often drops faster than household expenses.

That’s the problem.

The surviving spouse may lose one Social Security check. Pension income may be reduced depending on the payout option selected. Tax filing status may eventually change. Investment withdrawals may need to increase. Medicare premiums may be affected by the survivor’s income and filing status.

Meanwhile, many expenses stay close to the same.

The mortgage or rent may not change. Property taxes may not change. Home insurance may not change. Utilities may drop a little, but probably not by half. Car expenses, home maintenance, healthcare, and basic living costs may still be significant.

That means a retirement plan that looks comfortable for two people may become tighter for one person.

The key is to plan for the survivor before anything happens.

1. One Social Security Check Usually Goes Away

The first major retirement income change after one spouse dies is Social Security.

For many married couples, Social Security is a major part of monthly retirement income. While both spouses are alive, each may receive their own benefit, or one spouse may receive a spousal benefit based on the other spouse’s earnings record.

But after one spouse dies, the household generally does not keep both Social Security checks.

Instead, the surviving spouse may be eligible for a survivor benefit. In many cases, the surviving spouse receives the higher of the two benefits, not both.

That means if one spouse was receiving $3,000 per month and the other was receiving $2,000 per month, the surviving spouse may continue with the $3,000 benefit, but the $2,000 benefit may stop.

That’s a $2,000 monthly income reduction.

This is why Social Security claiming decisions should be made as a household, not just as two individuals.

If the higher-earning spouse delays Social Security, it may increase not only their own benefit, but also the potential survivor benefit available to the spouse who lives longer.

That can be extremely important.

Many couples focus on maximizing income while both spouses are alive. But the surviving spouse may be the one who needs the larger benefit the most.

For example, if one spouse handles most of the financial decisions or has a longer life expectancy, protecting their future income should be part of the plan.

Social Security survivor benefits can be complex. The survivor’s age, the deceased spouse’s benefit, claiming history, and whether benefits are claimed before survivor full retirement age can all matter. Survivor benefits for spouses and ex-spouses can start as a reduced benefit before full retirement age and can reach up to 100% at full retirement age for survivors.

The important point is simple: when one spouse dies, Social Security income can drop.

That drop needs to be tested before retirement.

A Retirement Readiness Review can help compare Social Security claiming strategies and show how income may change after the first spouse dies.

- The household usually does not keep both Social Security checks.

- The surviving spouse may receive the higher benefit.

- The smaller benefit often goes away.

- Delaying the higher earner’s benefit may increase survivor protection.

- Social Security should be planned for both spouses, not just individually.

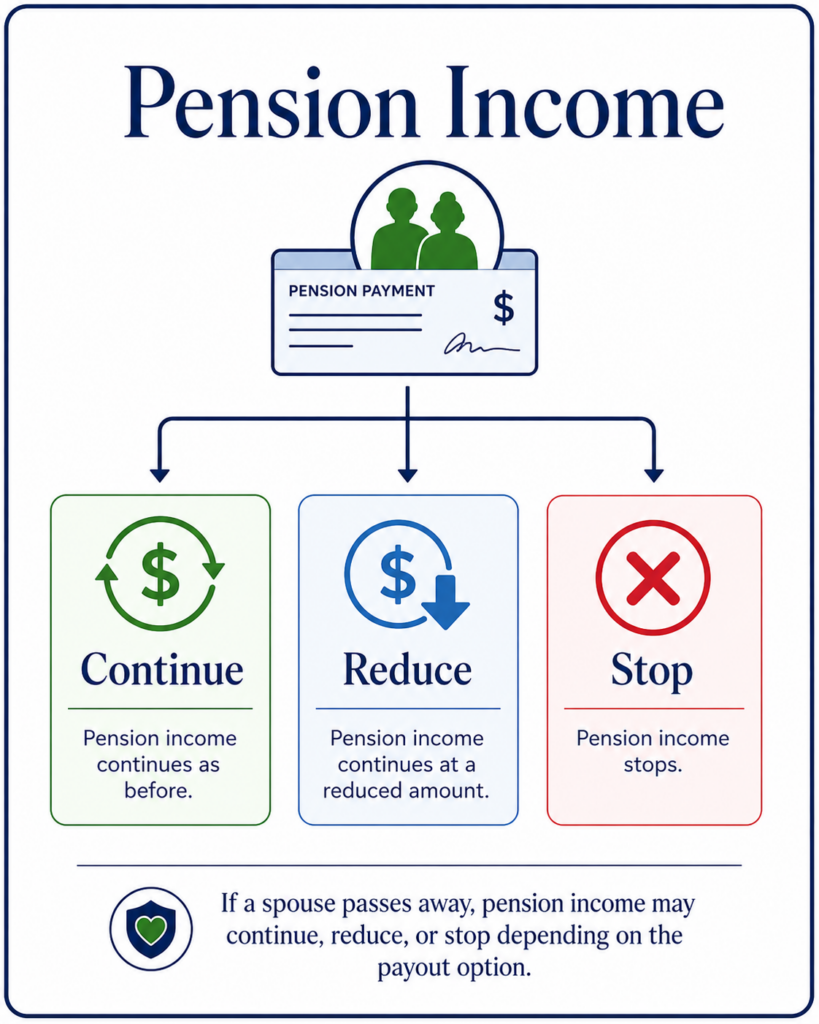

2. Pension Income May Continue, Reduce, or Stop

The second major issue is pension income.

If one or both spouses have a pension, the pension election can have a huge impact on the surviving spouse.

Many pensions offer several payout options. A single-life pension may pay the highest monthly amount while the pension holder is alive, but it may stop when that person dies. A joint-and-survivor pension may pay a lower monthly amount while both spouses are alive, but continue some income to the surviving spouse after the pension holder dies.

This decision can be permanent.

That’s why it’s so important.

For example, a pension might offer:

- A single-life payout.

- A 100% joint-and-survivor payout.

- A 75% joint-and-survivor payout.

- A 50% joint-and-survivor payout.

- A period-certain option.

- A lump-sum option.

The single-life option may look attractive because it often provides the largest monthly check at the beginning. But if that income disappears when the pension holder dies, the surviving spouse may face a major income problem.

On the other hand, a joint-and-survivor option may provide less income at first but more protection later.

There is no automatically right answer.

If the surviving spouse has plenty of their own income, assets, insurance, and Social Security, a single-life option may be considered in some cases. But if the surviving spouse depends heavily on the pension, giving up survivor protection could be dangerous.

This is also where life insurance sometimes enters the conversation.

Some people choose a higher single-life pension and use life insurance to protect the surviving spouse. That strategy can work in certain situations, but it must be tested carefully. Insurance premiums, health, policy guarantees, investment assumptions, and actual survivor needs all matter.

The worst approach is choosing a pension option based only on the largest monthly check.

That decision should be tested against real scenarios:

- What happens if the pension holder dies first?

- What happens if the surviving spouse lives 20 more years?

- What income remains?

- How much does the survivor need?

- How will taxes change?

- Will investments need to make up the difference?

- Is there life insurance?

- Is the survivor comfortable managing the plan?

Pension decisions are often made at retirement, but the consequences can last for decades.

A Retirement Readiness Review can help evaluate pension options before retirement so you can see how each choice affects both spouses.

- Pension elections can greatly affect survivor income.

- Single-life pensions may stop at death.

- Joint-and-survivor options may protect the surviving spouse.

- The highest monthly payout is not always the safest choice.

- Pension decisions should be tested before they become permanent.

3. The Surviving Spouse May Face a Higher Tax Burden

The third issue is taxes.

Many widows and widowers are surprised by how much taxes can change after one spouse dies.

In the year of death, the surviving spouse may generally still be able to file a joint return with the deceased spouse.

In some cases, for the two years following the year of death, the surviving spouse may qualify for qualifying surviving spouse filing status if certain requirements are met. That status uses the same tax rates as married filing jointly.

But eventually, many surviving spouses file as single.

That can create what some people call the “widow’s penalty” or “survivor tax penalty.”

The reason is simple: income may not drop as much as tax brackets and deductions do.

For example, the surviving spouse may still have:

- The higher Social Security benefit.

- Pension survivor income.

- IRA withdrawals.

- Required minimum distributions.

- Investment income.

- Rental income.

- Annuity income.

But they may no longer have married filing jointly tax brackets.

That can make the same or slightly lower income more expensive from a tax standpoint.

This can be especially important if most of the couple’s retirement savings are in traditional IRAs or 401(k)s. Required minimum distributions may continue, and those withdrawals are generally taxable.

Medicare costs may also be affected. Income-related monthly adjustment amounts, commonly called IRMAA, are based on income and filing status. A surviving spouse may cross a threshold more easily after filing status changes.

This doesn’t mean taxes will always explode after the first spouse dies. But it does mean the survivor’s tax picture should be tested.

Possible planning strategies may include:

- Roth conversions before one spouse dies.

- Earlier IRA withdrawals in lower tax years.

- Using taxable accounts strategically.

- Managing capital gains.

- Coordinating charitable giving.

- Reviewing beneficiary designations.

- Planning for RMDs.

- Considering qualified charitable distributions if eligible.

- Managing Medicare income thresholds.

These strategies are not right for everyone. But they are worth discussing before retirement, not after the surviving spouse is already dealing with grief.

Taxes are not just a math problem. They affect cash flow.

If the surviving spouse pays more in taxes, they may have less income available for living expenses. That can increase withdrawals from investments, which can create even more taxable income.

One decision touches another.

That’s why survivor tax planning matters.

A Retirement Readiness Review can help test the survivor’s tax situation so you can see whether the plan still works after filing status changes.

- The surviving spouse may eventually file as single.

- Tax brackets and deductions may become less favorable.

- Income may not drop as much as taxes change.

- Medicare IRMAA thresholds can be affected by filing status.

- Tax planning should include the surviving spouse scenario.

4. Investment Withdrawals May Need to Change

The fourth issue is investment withdrawals.

When one spouse dies, the retirement income plan may need to be rebuilt.

The surviving spouse may have less Social Security income, reduced pension income, higher taxes, and many of the same expenses. That means investments may need to produce more income than before.

This is where the retirement withdrawal strategy matters.

If the couple already had a clear plan, the surviving spouse may have an easier transition. If the couple was simply pulling money randomly from accounts, the surviving spouse may be left trying to figure everything out during one of the hardest seasons of life.

That is not fair to them.

A good retirement income plan should answer:

- Which accounts does the survivor use first?

- How much income is needed each month?

- How much should be withheld for taxes?

- Should the investment allocation change?

- Should withdrawals be reduced?

- Should the home be downsized?

- Should large expenses be delayed?

- Should Roth accounts be preserved or used?

- Should IRA withdrawals change?

- Is there enough cash available?

- Does the survivor know where everything is?

This is also where account titling and beneficiary designations matter.

The surviving spouse should have clear access to the accounts needed for income. Beneficiary designations on IRAs, 401(k)s, life insurance, annuities, and other accounts should be reviewed regularly.

Outdated beneficiary designations can create serious problems.

Investment risk may also need to be reconsidered.

Some surviving spouses are comfortable managing investments. Others are not. Some want to stay invested for growth. Others want more predictable income. Some are comfortable with market volatility. Others may panic during downturns.

The plan should fit the person who may have to live with it.

That means the investment strategy should not be designed only around the more financially confident spouse.

If one spouse handles all the money, the other spouse should still understand the basics:

- Where income comes from.

- Who to call.

- What accounts exist.

- What bills are due.

- How taxes are handled.

- What the plan is during a market downturn.

- What not to do quickly after a death.

One of the best gifts you can give your spouse is a plan they can understand.

That doesn’t mean they need to become an investment expert. But they should not be left in the dark.

A Retirement Readiness Review can help simplify the income plan and create a clearer path for the surviving spouse.

- The surviving spouse may need more income from investments.

- Withdrawal order may need to change.

- Account access and beneficiary designations matter.

- Investment risk should fit the surviving spouse.

- The plan should be simple enough for both spouses to understand.

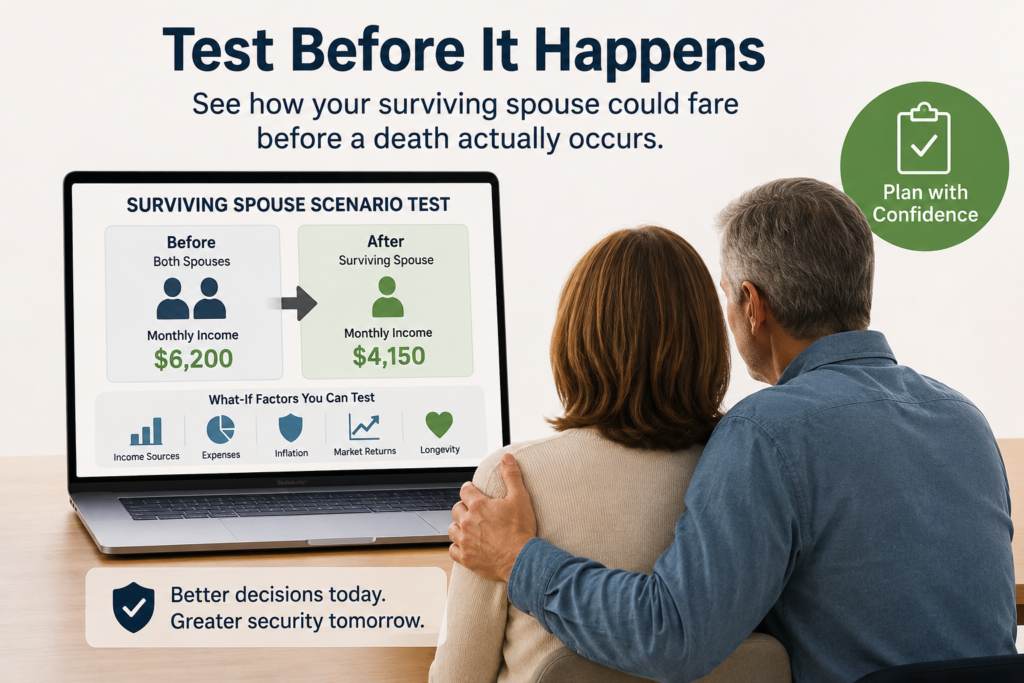

5. A Good Plan Should Test the Surviving Spouse Scenario Before It Happens

The fifth and most important point is this: your retirement plan should be tested for the surviving spouse before anything happens.

Most couples want to know, “Can we retire?”

That’s a good question.

But it’s not enough.

You also need to ask:

Can the surviving spouse stay retired if one of us dies?

That question changes the conversation.

A retirement plan may look strong while both spouses are alive. Two Social Security checks, pension income, shared expenses, and joint tax filing may make the numbers look comfortable.

But after the first death, the plan may look different.

You should test:

- What happens if either spouse dies first?

- What income continues?

- What income stops?

- What expenses remain?

- How do taxes change?

- How do Medicare costs change?

- Will investment withdrawals increase?

- Does the surviving spouse need to downsize?

- Is there enough life insurance?

- Are estate documents updated?

- Are beneficiaries correct?

- Is the plan easy to manage?

This is not about being negative. It’s about being responsible.

The truth is, one spouse is likely to outlive the other. That means survivor planning is not a remote possibility. It is a normal part of retirement planning.

The surviving spouse may live many years after the first spouse dies. They may need income for 10, 15, 20, or even 30 more years.

That income needs to be protected.

This is why Social Security claiming, pension elections, annuity choices, investment risk, tax planning, Roth conversions, life insurance, and estate planning should all be coordinated.

None of these decisions stands alone.

For example:

- Delaying Social Security may increase survivor income.

- Choosing a joint pension option may protect the surviving spouse.

- Roth conversions may reduce future tax pressure.

- Life insurance may fill an income gap.

- A cash reserve may provide breathing room.

- Simplifying accounts may reduce stress.

- Updating beneficiaries may prevent avoidable problems.

A strong retirement plan does not just ask what happens if everything goes right.

It asks what happens if life changes.

That’s where real confidence comes from.

A Retirement Readiness Review can help test both the joint retirement plan and the surviving spouse plan, so you can make decisions with your eyes open.

- Survivor planning should happen before retirement.

- The plan should test both spouse-death scenarios.

- Income, taxes, expenses, and investments may all change.

- Survivor protection should be built into Social Security and pension decisions.

- A good plan helps the surviving spouse avoid unnecessary stress.

Conclusion

When one spouse dies, retirement income can change in several important ways.

One Social Security check may go away. Pension income may continue, reduce, or stop depending on the election. Taxes may become less favorable when the surviving spouse eventually files as single. Investment withdrawals may need to increase. Medicare costs and income thresholds may become more important.

At the same time, many household expenses may remain.

That’s why survivor planning is not optional.

A retirement plan that only works while both spouses are alive may not be strong enough. The real test is whether the plan can support the surviving spouse too.

The goal is not to predict everything perfectly. The goal is to avoid obvious surprises. You want to know what income continues, what income stops, what expenses remain, what taxes may look like, and whether the surviving spouse can maintain their lifestyle.

If you’re married and within a few years of retirement, a Retirement Readiness Review can help you test this before decisions become permanent. We’ll look at Social Security, pensions, investments, taxes, income needs, and survivor protection so you can see where the plan is strong and where it may need adjustment.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before life forces decisions on you.

FAQs

Does a surviving spouse keep both Social Security checks?

Usually, no. In many cases, the surviving spouse may receive the higher of the two Social Security benefits, but not both. This means household Social Security income may drop after one spouse dies.

What happens to pension income when one spouse dies?

It depends on the pension option selected. A single-life pension may stop when the pension holder dies. A joint-and-survivor pension may continue some or all of the income to the surviving spouse. This is why pension elections should be reviewed carefully before retirement.

Do taxes increase after one spouse dies?

They can. The surviving spouse may eventually file as single, which can create less favorable tax brackets compared with married filing jointly. If income does not drop as much as the tax brackets change, the surviving spouse may face a higher tax burden.