IRMAA Explained: The Medicare Surcharge That Can Surprise Retirees

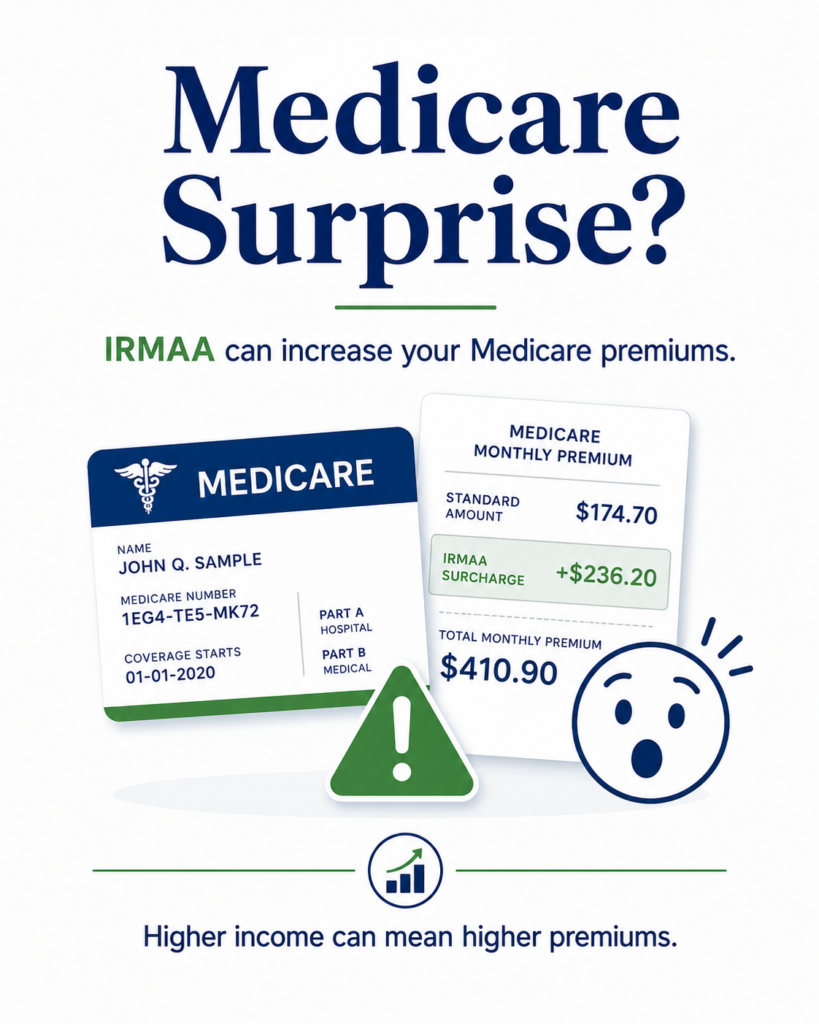

Medicare can already feel confusing, but one of the biggest surprises for retirees is something called IRMAA. It stands for Income-Related Monthly Adjustment Amount, and it’s an extra surcharge some higher-income retirees pay on top of their Medicare Part B and Part D premiums.

The frustrating part is that many retirees don’t realize IRMAA exists until they get a letter saying their Medicare premiums are going up. Even worse, the surcharge is usually based on income from two years earlier, which means a retirement decision you made in the past can affect your Medicare costs later.

In this article, we’ll walk through what IRMAA is, how it works, why retirees get surprised by it, and how better planning may help reduce the risk of unnecessary Medicare surcharges.

Key Point / Summary

IRMAA is an extra Medicare surcharge that can apply when your income is above certain thresholds. It can affect both Medicare Part B and Medicare Part D, and it’s usually based on your tax return from two years ago.

Here are the five key things we’ll cover:

- IRMAA is based on income, not assets.

- IRMAA can affect both Medicare Part B and Part D.

- Retirement income decisions can accidentally trigger IRMAA.

- Some life-changing events may allow you to request a lower surcharge.

- Medicare planning should be coordinated with tax and retirement income planning.

For 2026, the standard Medicare Part B premium is $202.90 per month, and higher-income beneficiaries may pay more because of IRMAA. The 2026 Part B deductible is $283.

This matters because Medicare costs are not separate from retirement planning. IRA withdrawals, Roth conversions, capital gains, pensions, part-time work, and Social Security decisions can all affect taxable income. And taxable income can affect IRMAA.

If you’re within a few years of retirement, a Retirement Readiness Review can help you test your income strategy before surprise Medicare surcharges show up.

What Is IRMAA and Why Does It Surprise Retirees?

IRMAA is an additional amount some Medicare beneficiaries pay if their income is above certain thresholds. It applies to Medicare Part B and Medicare Part D.

The reason it surprises retirees is simple: many people assume Medicare has one standard premium. But higher-income retirees may pay more.

Another surprise is the two-year lookback. In many cases, Medicare uses your income from two years earlier to determine whether IRMAA applies. So, your 2026 Medicare premiums may be based on your 2024 tax return.

That means a big income year can come back to affect you later.

Examples of income events that may trigger IRMAA include:

- Large IRA or 401(k) withdrawals

- Roth conversions

- Capital gains from selling investments

- Pension income

- Part-time work

- Business income

- Rental income

- Sale of property or business assets

- Required minimum distributions

- Taxable Social Security

- Interest and dividends

This is why IRMAA planning matters. You don’t want to make a retirement income decision in isolation and discover later that it increased your Medicare premiums.

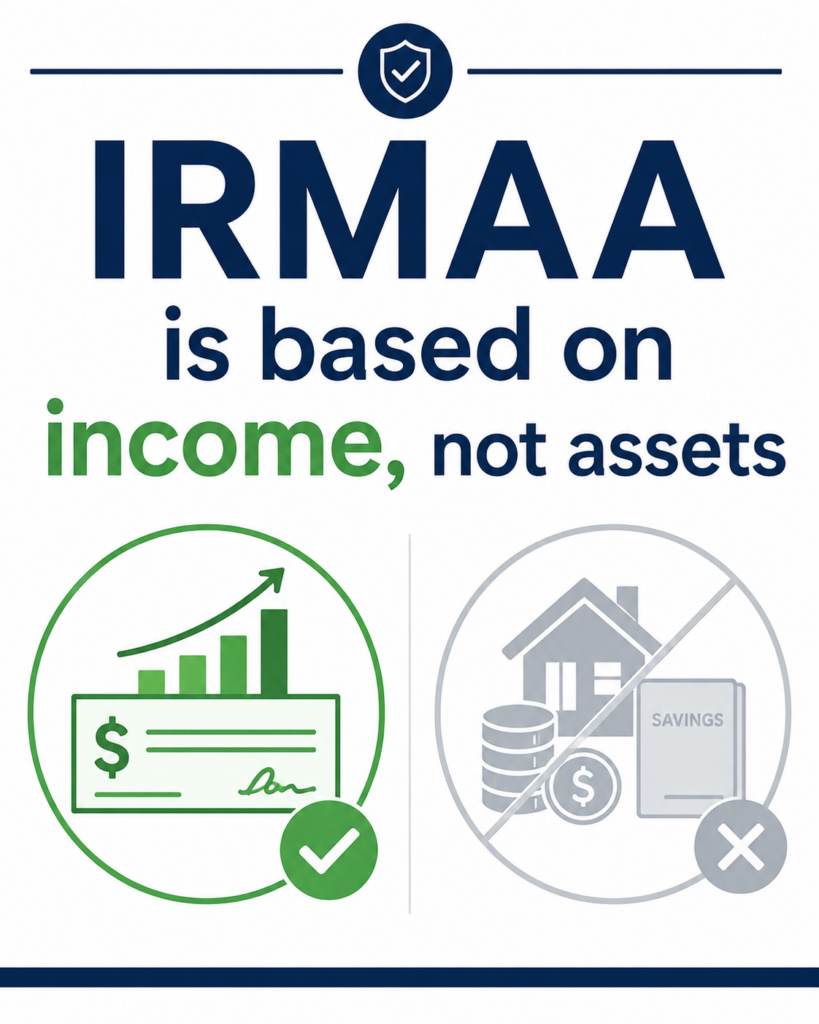

1. IRMAA Is Based on Income, Not Assets

The first thing to understand is that IRMAA is based on income, not your total net worth.

You could have a large investment portfolio and avoid IRMAA if your taxable income stays below the thresholds. Or you could have fewer assets but trigger IRMAA because you had a large taxable income year.

That distinction matters.

IRMAA is generally based on your modified adjusted gross income, often called MAGI. For Medicare IRMAA purposes, this usually means your adjusted gross income plus tax-exempt interest.

This is where retirees can get caught off guard.

They may think, “I’m not rich. I just took money from my IRA to buy a car, help my kids, do a Roth conversion, or pay off the house.”

But Medicare doesn’t look at why the income happened. It looks at the income number.

For example, a retiree might normally have income below the IRMAA threshold. But one year they sell a highly appreciated investment, take a large IRA withdrawal, or convert money to a Roth IRA. That one event could increase income enough to trigger higher Medicare premiums later.

This is why retirement income planning needs to be tax-aware.

A good plan should look at:

- How much income you need

- Which accounts you withdraw from

- Whether Roth conversions make sense

- When Social Security begins

- How pensions affect taxable income

- Whether capital gains may be realized

- Whether required minimum distributions are coming

- Whether Medicare premiums may increase

The key is not to avoid income at all costs. Sometimes it makes sense to create income on purpose. For example, Roth conversions can be smart in certain situations. Selling investments may be necessary. IRA withdrawals may be part of the plan.

But those choices should be made with eyes open.

A decision that saves taxes later might temporarily increase IRMAA now. That may still be worth it, but you want to know before you do it.

A Retirement Readiness Review can help you test income decisions before retirement so you can see whether they may affect Medicare costs.

- IRMAA is based on income, not total wealth.

- Large one-time income events can trigger Medicare surcharges.

- IRA withdrawals, Roth conversions, capital gains, and pensions can matter.

- The goal is not always to avoid IRMAA, but to avoid being surprised by it.

- Medicare planning should be part of retirement income planning.

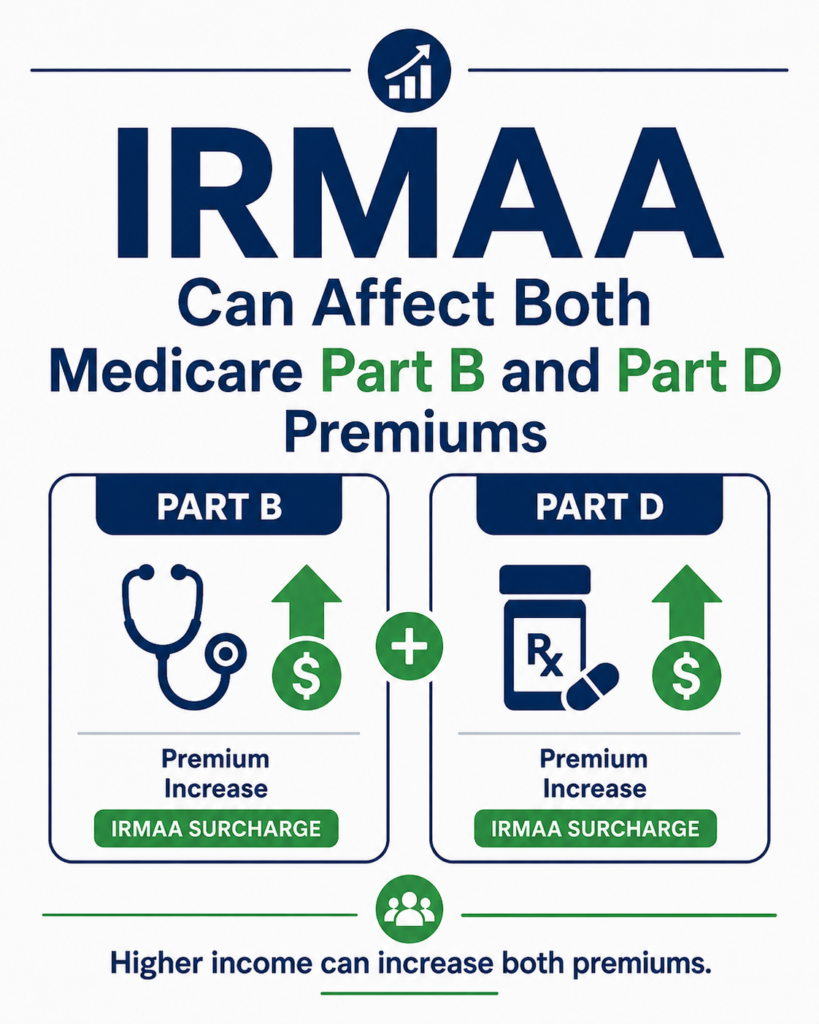

2. IRMAA Can Affect Both Medicare Part B and Part D

The second thing to understand is that IRMAA can apply to both Medicare Part B and Medicare Part D.

Medicare Part B covers medical insurance, including things like doctor services, outpatient care, preventive services, and certain medical equipment. Most people pay the standard Part B premium, but higher-income beneficiaries may pay more.

Medicare Part D covers prescription drug coverage. Even if your Part D plan has its own premium, IRMAA can add another surcharge on top of that.

That means IRMAA can hit retirees in two places at once.

For 2026, most people pay the standard Part B premium of $202.90 per month, while Social Security will tell beneficiaries the exact amount they’ll pay for Part B.

The key issue is that IRMAA is not a one-time annual fee. It is generally a monthly surcharge. So even a modest monthly increase can add up over the year.

For married couples, the impact can be even larger because each spouse on Medicare may be subject to their own Medicare premiums and surcharges.

For example, if both spouses are on Medicare and both are subject to IRMAA, the household cost can be meaningfully higher than expected.

That can create frustration because retirees often budget for basic Medicare premiums but forget about income-related surcharges.

This is especially important for people who are close to an IRMAA threshold.

If your income is just below a bracket, a relatively small amount of extra taxable income could push you into a higher Medicare premium tier. That might happen because of:

- A year-end IRA withdrawal

- Selling investments with capital gains

- A Roth conversion

- Part-time consulting income

- A bonus paid near retirement

- Required minimum distributions

- Taxable interest from higher cash balances

- A business or property sale

The annoying part is that crossing a threshold can sometimes create a disproportionate result. A little more income can lead to higher monthly premiums.

That doesn’t mean you should let IRMAA control every retirement decision. But it does mean you should know where the thresholds are and how close you are to them.

This is where tax planning and Medicare planning meet.

Before taking a large withdrawal or conversion, it’s wise to ask:

- Will this increase my modified adjusted gross income?

- Could it push me into an IRMAA bracket?

- Is the long-term benefit still worth the temporary surcharge?

- Can the income be spread over multiple years?

- Should I use Roth, taxable, or cash assets instead?

- Will this affect one spouse or both spouses?

- Will this change next year’s strategy?

A Retirement Readiness Review can help you compare different income scenarios and see whether IRMAA may become an issue.

- IRMAA can apply to Medicare Part B and Part D.

- The surcharge is usually monthly, not just one annual bill.

- Couples may feel a larger household impact.

- Small income changes near a threshold can matter.

- Medicare premium planning should be included in tax planning.

3. Retirement Income Decisions Can Accidentally Trigger IRMAA

The third thing to understand is that IRMAA is often triggered by normal retirement income decisions.

Most retirees don’t set out to increase their Medicare premiums. It happens because one decision affects another.

That’s the frustrating part of retirement planning.

You might make a decision that seems reasonable in one area, only to discover it creates a problem somewhere else.

For example, you may decide to do a Roth conversion. That conversion may be smart long-term because it could reduce future required minimum distributions, create tax-free income later, and improve flexibility for a surviving spouse or heirs.

But the conversion may also increase income this year. That higher income may trigger IRMAA two years later.

Or you may sell appreciated investments to fund a major purchase. That may create capital gains. Those gains may increase your MAGI and affect Medicare premiums.

Or you may retire and take a large distribution from your 401(k) to pay off your mortgage. That might reduce debt, but it could also increase taxable income enough to create Medicare surcharges.

None of these decisions are automatically wrong.

The problem is making them without testing the ripple effects.

Retirement income decisions that may affect IRMAA include:

- Roth conversions

- Traditional IRA withdrawals

- 401(k) withdrawals

- Pension income

- Social Security taxation

- Capital gains

- Interest income

- Dividend income

- Business income

- Rental income

- Required minimum distributions

- Sale of a second home

- Sale of a business

- Part-time work

The key is timing.

Sometimes a good strategy becomes better when spread over multiple years. Instead of doing one large Roth conversion, it may make sense to convert smaller amounts over time. Instead of taking one large IRA withdrawal, it may make sense to use a mix of taxable, IRA, Roth, and cash assets.

Again, the goal isn’t always to avoid IRMAA. Sometimes paying IRMAA for a year or two may be worth it if the long-term tax savings are strong enough.

But surprise IRMAA is different from planned IRMAA.

Planned IRMAA means you knew the cost and accepted it.

Surprise IRMAA means you didn’t realize the decision would affect Medicare premiums.

Those are very different experiences.

This is also important for people approaching age 63. Because of the two-year lookback, income at age 63 may affect Medicare premiums at age 65.

Many people don’t realize Medicare planning begins before Medicare starts.

That’s why the final few working years before retirement matter. A big bonus, stock sale, business income year, or Roth conversion before Medicare can affect the first year of Medicare premiums.

A Retirement Readiness Review can help identify these timing issues before they create surprises.

- IRMAA can be triggered by normal retirement income decisions.

- Roth conversions and IRA withdrawals can increase MAGI.

- Capital gains and interest income may also matter.

- The two-year lookback means planning should begin before Medicare starts.

- Planned IRMAA may be acceptable; surprise IRMAA is the problem.

4. Some Life-Changing Events May Allow You to Request a Lower IRMAA

The fourth thing to understand is that IRMAA is not always set in stone.

If your income has gone down because of a qualifying life-changing event, you may be able to ask Social Security to lower your IRMAA.

This is especially important for new retirees.

Why?

Because Medicare may base your premium on income from two years ago, when you were still working. If you retire and your income drops, the older tax return may no longer reflect your current situation.

You can request a lower IRMAA if you’ve had a life-changing event that reduced household income. Examples include marriage, divorce, death of a spouse, loss of income, and an employer settlement payment.

The form commonly used for this is SSA-44, Medicare Income-Related Monthly Adjustment Amount Life-Changing Event.

Life-changing events may include:

- Marriage

- Divorce or annulment

- Death of a spouse

- Work stoppage

- Work reduction

- Loss of income-producing property

- Loss of pension income

- Employer settlement payment

This can be very useful for retirees who stop working and suddenly have much lower income.

For example, suppose Medicare uses your tax return from two years ago when you were still earning a high salary. But now you’re retired and your income is much lower. You may be able to request that Social Security use more recent income information instead.

That could reduce or eliminate the surcharge if you qualify.

But you usually need to take action. Social Security may not automatically know your current situation has changed.

This is why retirees should pay attention to Medicare letters.

If you receive an IRMAA notice and your income has dropped because of a qualifying event, don’t ignore it. Review the notice, gather documentation, and consider filing a request for reconsideration or using Form SSA-44 if appropriate.

Documentation may include:

- Employer retirement letter

- Final pay stub

- Divorce decree

- Death certificate

- Proof of pension loss

- Tax return

- Estimate of current-year income

The key is that the income reduction must generally be tied to a qualifying life-changing event.

Simply having investment losses or not liking the surcharge may not be enough.

This is another area where planning helps. If you know you’re retiring, you can anticipate that your Medicare premium may be based on higher income from your working years. Then you can be ready to respond.

A Retirement Readiness Review can help identify whether a life-changing event may apply and how Medicare premiums may change after retirement.

- IRMAA may be lowered after certain life-changing events.

- Retirement or reduced work may qualify if income drops.

- Social Security Form SSA-44 is commonly used for this request.

- You may need documentation.

- Don’t ignore IRMAA notices if your income has changed.

5. Medicare Planning Should Be Coordinated With Tax and Retirement Income Planning

The fifth and most important point is that IRMAA should not be handled by itself.

IRMAA is connected to your retirement income plan, tax plan, investment withdrawals, Social Security, Roth conversion strategy, and even survivor planning.

That’s why isolated decisions can create problems.

For example, a CPA may focus on reducing this year’s taxes. An investment advisor may focus on portfolio returns. A Medicare agent may focus on plan selection. But IRMAA sits at the intersection of all three.

You need a coordinated plan.

That plan should answer:

- How much income do you need each year?

- Which accounts should provide that income?

- How close are you to IRMAA thresholds?

- Should Roth conversions be done before Medicare starts?

- Should conversions continue after Medicare starts?

- Should capital gains be harvested gradually?

- Should cash reserves be used in high-income years?

- How will required minimum distributions affect future IRMAA?

- How will a surviving spouse be affected?

- What happens if one spouse dies and filing status changes?

- How will Medicare premiums fit into the retirement budget?

This last point matters more than many couples realize.

When one spouse dies, the surviving spouse may eventually file as single. That can make IRMAA thresholds easier to cross. The same income that was manageable as a married couple may create more tax and Medicare premium pressure for the survivor.

That’s why Roth conversions, IRA withdrawal timing, and survivor tax planning can be connected to IRMAA planning.

Required minimum distributions can also matter. If you build a large traditional IRA and delay withdrawals for years, future RMDs may push income higher later in retirement. That could affect taxes, Social Security taxation, and Medicare premiums.

This doesn’t mean everyone should aggressively convert to Roth or drain IRAs early. That would be too simplistic.

It means the strategy should be tested.

Sometimes it may be worth triggering IRMAA now to reduce bigger tax problems later. Sometimes it may be better to avoid a threshold. Sometimes the difference is small enough that the planning decision should be based on other priorities.

The only way to know is to run the numbers.

The real goal is not just lower Medicare premiums. The goal is better lifetime retirement income after taxes, premiums, and risks.

A strong retirement plan should help you decide:

- When to take income

- Where to take income from

- When to realize gains

- Whether Roth conversions make sense

- How to manage RMDs

- How to protect the surviving spouse

- How to avoid surprise Medicare costs

That’s the kind of planning that gives retirees more confidence.

A Retirement Readiness Review can help you test different income strategies so IRMAA becomes part of the plan instead of an unpleasant surprise.

- IRMAA is connected to taxes, withdrawals, and Social Security.

- Roth conversions can help or hurt depending on timing.

- RMDs may increase future Medicare premiums.

- Survivor planning matters because filing status can change.

- The best plan looks at after-tax, after-premium retirement income.

Conclusion

IRMAA is one of those retirement issues that can surprise people because it doesn’t always feel obvious.

You may think you’re just taking an IRA withdrawal, doing a Roth conversion, selling an investment, or earning a little part-time income. But that income can affect your Medicare premiums later.

That’s why IRMAA planning matters.

IRMAA is based on income, not assets. It can affect both Medicare Part B and Part D. It often uses a two-year lookback. It can be triggered by normal retirement decisions. And in some cases, if your income drops because of a qualifying life-changing event, you may be able to request a lower surcharge.

The goal is not to live in fear of IRMAA. The goal is to understand it.

Sometimes paying IRMAA may be worth it if the bigger retirement strategy makes sense. Other times, careful planning may help you avoid unnecessary surcharges. Either way, the decision should be intentional.

If you’re within a few years of retirement and want to know how Medicare premiums may fit into your retirement income plan, a Retirement Readiness Review can help. We’ll look at income sources, withdrawals, Social Security, Roth conversions, taxes, Medicare thresholds, and survivor planning so you can understand the trade-offs before surprises happen.

You don’t have to move your money. You don’t have to buy a product. You just need a clear plan for how your retirement income decisions affect the rest of your financial life.

FAQs

What is IRMAA?

IRMAA stands for Income-Related Monthly Adjustment Amount. It is an extra Medicare surcharge that higher-income beneficiaries may pay on top of Medicare Part B and Part D premiums.

What income counts for IRMAA?

IRMAA is generally based on modified adjusted gross income, which usually includes adjusted gross income plus tax-exempt interest. IRA withdrawals, pensions, wages, capital gains, interest, dividends, and Roth conversions may all affect the calculation.

Can I appeal or reduce IRMAA after retirement?

Possibly. If your income dropped because of a qualifying life-changing event, such as work stoppage, work reduction, divorce, marriage, death of a spouse, or loss of pension income, you may be able to ask Social Security to lower your IRMAA.