How to Plan for Healthcare Costs Before Medicare Age

Retiring before Medicare age can sound exciting. You may be ready to leave work, slow down, travel, spend more time with family, or finally stop living around your job.

But there’s one big issue that can catch early retirees off guard: healthcare coverage before age 65.

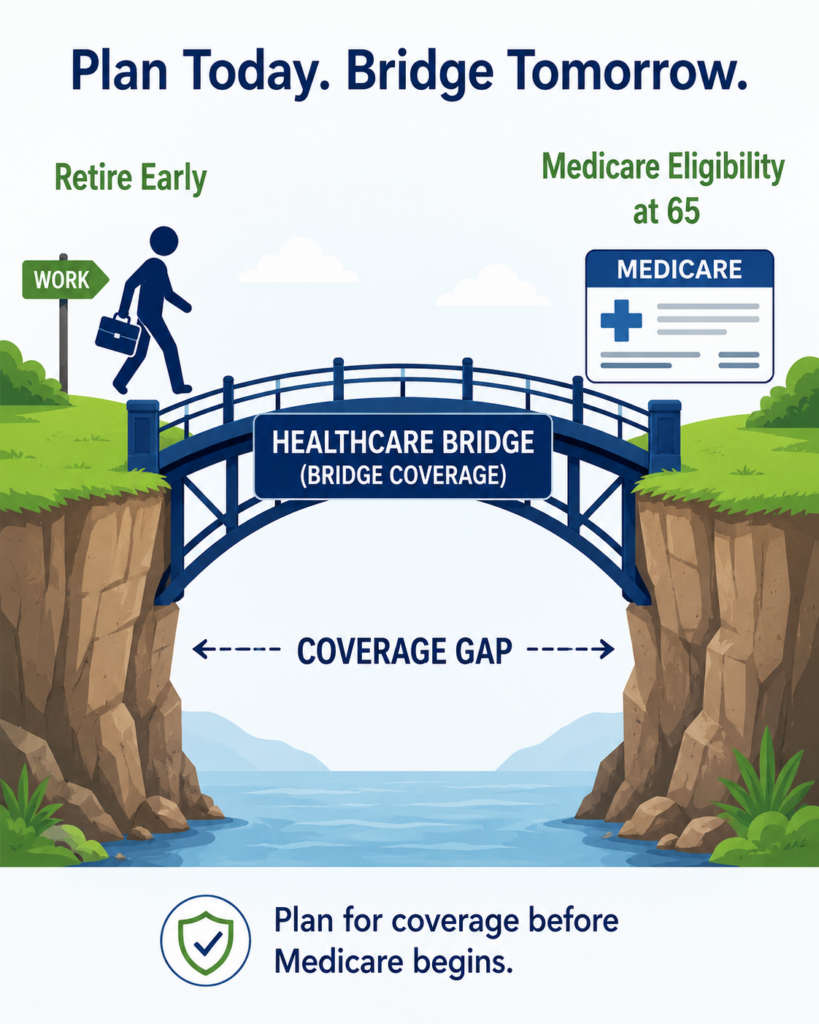

Medicare generally starts at age 65, which means if you retire at 60, 62, 63, or 64, you need a healthcare bridge. That bridge can be expensive if you don’t plan ahead. In this article, we’ll walk through five important steps to help you plan for healthcare costs before Medicare age so your retirement decision doesn’t get derailed by surprise premiums, deductibles, or coverage gaps.

Key Point / Summary

Planning for healthcare before Medicare age means figuring out where your coverage will come from, how much it may cost, how your income affects subsidies, and how to bridge the gap safely until Medicare begins.

Short on time? Here are the five key things we’ll cover:

- Know exactly when Medicare starts.

- Compare your pre-Medicare health insurance options.

- Estimate premiums, deductibles, and out-of-pocket costs.

- Coordinate healthcare planning with your retirement income strategy.

- Build a healthcare bridge before you retire.

Medicare is generally first available at age 65, and the Initial Enrollment Period lasts seven months: it starts three months before the month you turn 65 and ends three months after that month.

If you retire before age 65 and lose employer coverage, you can use the Health Insurance Marketplace to buy coverage, and losing job-based coverage can qualify you for a Special Enrollment Period outside the normal Open Enrollment window.

This is why healthcare planning should be part of your retirement income plan. If you’re within a few years of retirement, a Retirement Readiness Review can help you test whether retiring before Medicare age is realistic after healthcare costs are included.

How Do You Plan for Healthcare Costs Before Medicare Age?

You plan for healthcare costs before Medicare age by identifying your coverage options, estimating the full cost of coverage, and coordinating your income so you don’t accidentally make health insurance more expensive than it needs to be.

The mistake many people make is only looking at monthly premiums.

Premiums matter, but they are not the whole story.

You also need to consider:

- Deductibles

- Copays

- Coinsurance

- Prescription drug costs

- Provider networks

- Out-of-pocket maximums

- Marketplace subsidies

- COBRA costs

- Spouse’s employer coverage

- Health Savings Account funds

- Taxable income

- Roth conversions

- IRA withdrawals

- Timing of retirement

The real question is not just, “Can I retire before Medicare?”

The better question is:

Can I retire before Medicare and still afford healthcare without damaging the rest of my retirement plan?

1. Know Exactly When Medicare Starts

The first step is knowing when Medicare begins and how long your pre-Medicare gap will last.

Medicare generally begins at age 65. Your first chance to sign up is your Initial Enrollment Period, which lasts seven months. It starts three months before the month you turn 65 and ends three months after the month you turn 65.

This matters because the length of your healthcare gap depends on your retirement date.

For example:

- If you retire at 64 and 6 months, you may only need a short healthcare bridge.

- If you retire at 62, you may need roughly three years of coverage.

- If you retire at 60, you may need about five years of coverage.

- If your spouse is younger, they may need coverage even after you move to Medicare.

That last point is important.

Many couples focus on the older spouse’s Medicare date. But if one spouse is 65 and the other is 61, the younger spouse may still need private health insurance for several years.

That can create a major planning issue.

You also need to understand that Medicare does not automatically solve every healthcare cost. Medicare has premiums, deductibles, coinsurance, prescription drug costs, and possible supplemental coverage costs. For 2026, the standard Medicare Part B premium is $202.90 per month, and the Part B deductible is $283.

So, the goal is not just to survive until Medicare. The goal is to plan for both the pre-Medicare years and the Medicare years.

Before retiring early, you should ask:

- What month will I turn 65?

- When does Medicare coverage begin?

- When does my employer coverage end?

- Does my spouse need coverage longer than I do?

- Will I use COBRA, Marketplace coverage, or a spouse’s plan?

- Will I need dental, vision, or long-term care planning separately?

- How will healthcare costs change once Medicare begins?

This is where a retirement date can matter.

Retiring one month earlier or later may affect how long you need private health insurance, whether you qualify for certain employer benefits, or whether you have a coverage gap.

A Retirement Readiness Review can help you map your healthcare timeline before you leave work.

- Medicare generally begins at age 65.

- Your Initial Enrollment Period lasts seven months.

- Retiring before 65 means you need a healthcare bridge.

- Younger spouses may need coverage longer.

- Medicare still has premiums and out-of-pocket costs.

2. Compare Your Pre-Medicare Health Insurance Options

The second step is comparing your coverage options.

If you retire before Medicare age, you may have several possible ways to get health insurance. The right choice depends on your age, income, employer benefits, spouse, health needs, and budget.

Common options include:

- COBRA

- Spouse’s employer plan

- Affordable Care Act Marketplace coverage

- Retiree health benefits from a former employer

- Private health insurance

- Part-time work with benefits

- Health-sharing arrangements, though these are not the same as insurance

- Self-insuring for minor costs while carrying major medical coverage

COBRA is one common option for people who leave an employer plan. COBRA provides temporary continuation coverage that usually lasts up to 18 months, with some life events allowing coverage to extend to 36 months.

COBRA can be convenient because it may let you keep your current doctors and coverage for a period of time. But it can also be expensive because you may pay the full premium plus administrative costs.

Another option is a spouse’s employer plan. If your spouse is still working and has access to group health insurance, this may be one of the strongest options. It may offer better coverage, broader provider networks, or lower costs than individual coverage.

Marketplace coverage can also be important. If you retire before age 65 and lose job-based coverage, you can use the Marketplace to buy a plan, and that loss of coverage may create a Special Enrollment Period.

Marketplace plans may also include premium tax credits depending on household income. Marketplace savings are based on expected household income for the year you want coverage, not last year’s income.

That creates a planning opportunity, but also a planning risk.

If your income is lower after retirement, you may qualify for more help with premiums. But if you take large IRA withdrawals, do Roth conversions, realize capital gains, or earn part-time income, your household income may rise and reduce subsidies.

That means your healthcare option is connected to your income plan.

You should compare plans based on more than just premium.

Look at:

- Monthly premium

- Deductible

- Out-of-pocket maximum

- Prescription coverage

- Doctor network

- Hospital network

- Specialist access

- HSA eligibility

- Coverage for your spouse

- Coverage in other states if you travel

- Prior authorization rules

- Total worst-case cost

A low premium plan may look attractive, but if the deductible and out-of-pocket maximum are high, it may be expensive if you actually need care.

A more expensive premium may make sense if it lowers your risk or gives you access to doctors you trust.

A Retirement Readiness Review can help compare these costs so healthcare is included in your retirement income plan.

- COBRA may bridge coverage but can be expensive.

- A spouse’s employer plan may be a strong option.

- Marketplace plans may be available after losing employer coverage.

- Marketplace subsidies depend on expected household income.

- Compare total healthcare exposure, not just monthly premiums.

3. Estimate Premiums, Deductibles, and Out-of-Pocket Costs

The third step is estimating the full cost of healthcare.

Many early retirees only budget for the monthly premium. That’s a mistake.

Healthcare costs include more than premiums.

You also need to plan for:

- Deductibles

- Copays

- Coinsurance

- Prescriptions

- Specialist visits

- Lab work

- Imaging

- Therapy

- Dental

- Vision

- Hearing

- Out-of-network costs

- Emergency care

- Out-of-pocket maximums

The premium is what you pay to keep the insurance. The deductible and out-of-pocket costs are what you may pay when you actually use it.

For example, a Marketplace plan might have a manageable monthly premium but a high deductible. That may be fine if you’re healthy and rarely use care. But if you have prescriptions, ongoing treatment, or a planned surgery, the total cost could be much higher.

This is why you should build three healthcare cost estimates:

Best-case cost

This is your annual premium plus routine care.

Expected cost

This includes premiums, prescriptions, regular doctor visits, and known medical needs.

Worst-case cost

This includes premiums plus the full out-of-pocket maximum.

The worst-case number matters because retirement planning is not just about average years. It’s about surviving expensive years without panic.

For example, if your plan has a $10,000 out-of-pocket maximum and your spouse has a similar plan, your household exposure could be significant. You may not hit that number every year, but you should know whether your plan can handle it.

You should also think carefully about prescriptions.

Prescription costs can vary dramatically between plans. One plan may cover a medication well, while another may have poor coverage or require prior authorization.

Before choosing coverage, check:

- Are your medications covered?

- What tier are they on?

- Are there quantity limits?

- Is prior authorization required?

- Are your pharmacies in network?

- Are mail-order options available?

Provider networks also matter.

A cheap plan may not be cheap if your preferred doctors or hospitals are out of network.

This is especially important if you travel or split time between states. Some plans have narrower local networks and may not be ideal for people who spend months away from home.

The goal is not to find the cheapest plan. The goal is to find the most appropriate plan for your health, budget, and retirement lifestyle.

Healthcare planning before Medicare is really risk management.

You want to know:

- What will I pay in a normal year?

- What could I pay in a bad year?

- Can my retirement income plan handle both?

- Should I keep more cash available?

- Should I delay retirement until Medicare?

- Should one spouse keep working for benefits?

A Retirement Readiness Review can help stress-test your plan with realistic healthcare cost assumptions.

- Premiums are only one part of healthcare costs.

- Deductibles and out-of-pocket maximums matter.

- Prescription coverage should be reviewed carefully.

- Provider networks can affect real-world costs.

- Plan for normal years and expensive years.

4. Coordinate Healthcare Planning With Your Retirement Income Strategy

The fourth step is coordinating healthcare costs with your retirement income strategy.

This is where many early retirees get surprised.

Your income may affect the cost of your health insurance before Medicare, especially if you’re using Marketplace coverage. Marketplace savings are based on your expected household income for the coverage year.

That means your withdrawal choices can affect your healthcare costs.

For example, if you retire at 62 and use the Marketplace until 65, your household income may determine whether you qualify for premium tax credits. If you take a large IRA withdrawal, do a big Roth conversion, sell investments with large capital gains, or earn part-time income, your income may rise.

That may reduce subsidies and increase your net health insurance cost.

This does not mean you should avoid income. You need income to live.

It means income should be planned carefully.

Possible income sources before Medicare include:

- Cash savings

- Taxable brokerage accounts

- Traditional IRA withdrawals

- Roth IRA withdrawals

- 401(k) withdrawals

- Part-time work

- Pension income

- Rental income

- Spouse’s income

- Social Security if claimed early

Each source can affect taxes differently. Some may also affect Marketplace subsidies differently.

For example, Roth IRA qualified withdrawals may not increase taxable income the same way traditional IRA withdrawals do. Cash savings may provide spending money without creating the same taxable income. Taxable brokerage accounts may create capital gains if investments are sold.

This is why the years before Medicare can be valuable planning years, but also delicate years.

You may want to do Roth conversions before required minimum distributions begin. But if you’re relying on Marketplace subsidies, a large Roth conversion may increase income and reduce healthcare assistance.

You may want to sell appreciated investments. But capital gains may increase income.

You may want to work part-time. But wages may affect both taxes and subsidies.

The right strategy depends on the numbers.

A good pre-Medicare income plan should answer:

- How much income do we need each year?

- Which accounts should fund that income?

- How much income can we show before subsidies are affected?

- Should Roth conversions wait?

- Should cash be used to manage income?

- Should capital gains be spread out?

- Should Social Security be delayed?

- Should one spouse work longer for benefits?

- What happens when Medicare begins?

The goal is not to let health insurance control your entire retirement plan. The goal is to understand the trade-offs.

Sometimes it may be worth creating more income and paying higher premiums. Other times, careful withdrawal planning may save thousands in healthcare costs.

A Retirement Readiness Review can help test different withdrawal strategies before you retire early.

- Marketplace subsidies may depend on expected household income.

- IRA withdrawals, Roth conversions, gains, and wages can affect income.

- Cash and Roth accounts may provide flexibility in some situations.

- Healthcare and tax planning should be coordinated.

- Pre-Medicare income planning can make early retirement more realistic.

5. Build a Healthcare Bridge Before You Retire

The fifth step is building a healthcare bridge before you retire.

A healthcare bridge is your plan for getting from your retirement date to Medicare age without coverage gaps, surprise costs, or unnecessary stress.

This bridge should include:

- Your coverage source

- Monthly premiums

- Expected out-of-pocket costs

- Worst-case annual costs

- Prescription costs

- Provider network review

- Spouse coverage

- Income strategy

- Cash reserve

- Medicare enrollment timeline

You should build this bridge before you give notice at work.

That may sound obvious, but many people don’t do it. They focus on whether their investment portfolio can support retirement and then treat healthcare as a side issue.

Healthcare is not a side issue.

For early retirees, healthcare may be one of the largest expenses between retirement and Medicare.

Before retiring, you should know:

- What happens to employer coverage after your last day?

- Does coverage end immediately or at month-end?

- Can you use COBRA?

- What will COBRA cost?

- Is Marketplace coverage available?

- Will you qualify for subsidies?

- Can your spouse add you to their employer plan?

- Are your doctors covered?

- Are your prescriptions covered?

- How much cash should you set aside?

- When do you need to enroll in Medicare?

You also want to avoid coverage gaps.

A short gap may not sound like a big deal until something happens during that gap. One accident, diagnosis, or hospitalization can create major financial stress.

You should also think about timing your retirement date.

For example, if your employer coverage lasts through the end of the month, retiring at the beginning of a month may give you more coverage time than retiring at the end of a month. If bonuses, severance, unused vacation, or stock compensation are involved, those may also affect taxable income and Marketplace subsidies.

This is why retirement timing should be intentional.

You should also prepare for the transition to Medicare.

As you approach age 65, you’ll need to understand Medicare Part A, Part B, Part D, Medicare Advantage, Medicare Supplement plans, and whether IRMAA may apply.

Medicare planning should begin before your 65th birthday because your Initial Enrollment Period starts three months before the month you turn 65.

If you’re on Marketplace coverage, you should update your Marketplace application when Medicare starts so Marketplace coverage ends the day before Medicare begins.

That detail matters because you don’t want overlapping coverage mistakes or subsidy repayment problems.

A Retirement Readiness Review can help organize your healthcare bridge so you know what to do before and after your retirement date.

- Build your healthcare bridge before leaving work.

- Know when employer coverage ends.

- Avoid coverage gaps.

- Time retirement carefully if benefits and income are affected.

- Prepare for the Medicare transition before age 65.

Conclusion

Planning for healthcare costs before Medicare age is one of the most important parts of early retirement planning.

If you retire before 65, you need a clear bridge from your employer coverage to Medicare. That bridge might involve COBRA, a spouse’s plan, Marketplace coverage, retiree benefits, private insurance, or part-time work with benefits.

But the plan should not stop with choosing coverage.

You also need to estimate premiums, deductibles, out-of-pocket maximums, prescriptions, provider networks, and worst-case healthcare costs. Then you need to coordinate those costs with your retirement income strategy, because withdrawals, Roth conversions, capital gains, wages, and pensions may affect taxes and Marketplace subsidies.

The biggest mistake is assuming healthcare will “work itself out.”

It might. But that’s not a plan.

If you’re thinking about retiring before Medicare age, healthcare needs to be tested before you leave work. You want to know what coverage will cost, where the money will come from, how long the bridge lasts, and whether your retirement plan still works after realistic healthcare costs are included.

A Retirement Readiness Review can help you answer those questions before you make the leap. We’ll look at your income needs, retirement date, healthcare options, tax strategy, Social Security timing, and investment withdrawals so you can see whether early retirement is truly realistic.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before giving up your paycheck and employer health insurance.

FAQs

Can I retire before 65 and still get health insurance?

Yes. If you retire before 65 and lose job-based coverage, you may be able to use COBRA, join a spouse’s employer plan, buy Marketplace coverage, use retiree health benefits, or buy private insurance. Marketplace coverage may be available through a Special Enrollment Period after losing job-based coverage.

How long can COBRA last after I retire?

COBRA usually provides temporary continuation coverage for up to 18 months, although certain life events may extend coverage to 36 months.

Does retirement income affect health insurance before Medicare?

It can. If you use Marketplace coverage, premium savings are generally based on expected household income for the coverage year. IRA withdrawals, capital gains, Roth conversions, pensions, wages, and other taxable income may affect whether you qualify for subsidies.