How to Choose the Best Pension Payout Option

Choosing a pension payout option can be one of the most important retirement decisions you’ll ever make. Once you make the election, it may be permanent. That means the choice you make today could affect your income, your spouse’s income, your taxes, your investment withdrawals, and your financial security for the rest of your life.

The challenge is that pension options can be confusing. You may see choices like single life, joint and survivor, period certain, lump sum, partial lump sum, or survivor percentages. One option may give you the highest monthly check. Another may provide less income now but more protection for your spouse later. Another may give you more flexibility, but also more responsibility.

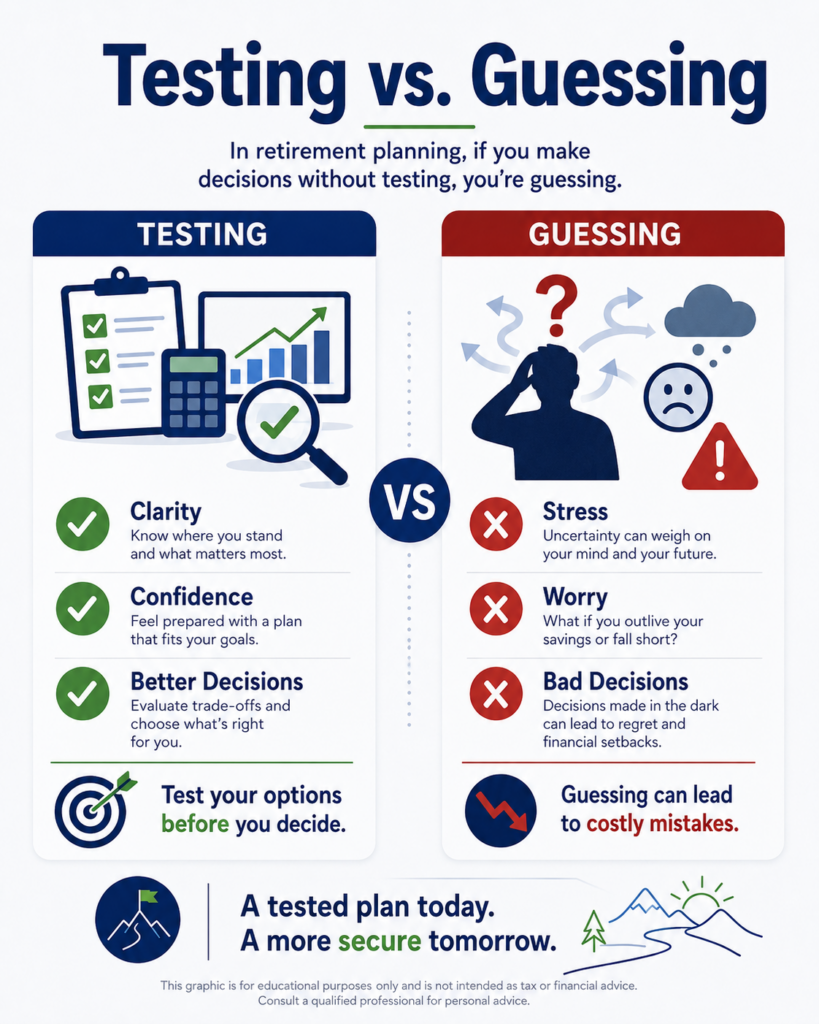

In this article, we’ll walk through five important steps to help you choose the best pension payout option. The goal isn’t to tell you which option is automatically best. The goal is to help you understand the trade-offs so you can make the decision based on your actual retirement plan instead of guessing.

Short on Time? Here is the Key Point / Summary

Choosing the best pension payout option means comparing income, survivor protection, flexibility, taxes, investment risk, and longevity risk before making a permanent decision.

Here are the five key things we’ll cover:

- Understand what each pension payout option actually means.

- Compare the monthly income difference.

- Protect the surviving spouse.

- Decide whether a lump sum gives you more flexibility or more risk.

- Test each option inside your full retirement plan.

The biggest mistake is choosing the largest monthly check without understanding what happens if you die first, your spouse dies first, inflation rises, taxes change, or your investment accounts have to cover an income gap.

A pension decision should not be made by looking at the pension paperwork alone. It should be coordinated with Social Security, savings, investment withdrawals, taxes, insurance, healthcare, and survivor planning.

If you’re within a few years of retirement and trying to choose a pension payout option, a Retirement Readiness Review can help you test the choices before making an election you may not be able to undo.

How Do You Choose the Best Pension Payout Option?

You choose the best pension payout option by answering one main question:

Which option gives your household the best balance of income today, protection tomorrow, and flexibility for the future?

That answer will be different for different people.

For example, a single retiree with no dependents may look at pension options differently than a married retiree whose spouse depends on the pension income. Someone with a large investment portfolio may make a different choice than someone whose pension is the foundation of their retirement income. Someone in excellent health may choose differently than someone with serious health concerns.

The right pension option depends on factors like:

- Your age

- Your spouse’s age

- Your health

- Your spouse’s health

- Your monthly income need

- Your Social Security benefits

- Your investment savings

- Your tax situation

- Your life expectancy

- Your desire to leave money to heirs

- Your comfort managing investments

- Your need for guaranteed income

- Your ability to handle income loss after one spouse dies

The best pension option is not always the one with the biggest monthly payment.

It’s the one that fits your full retirement plan.

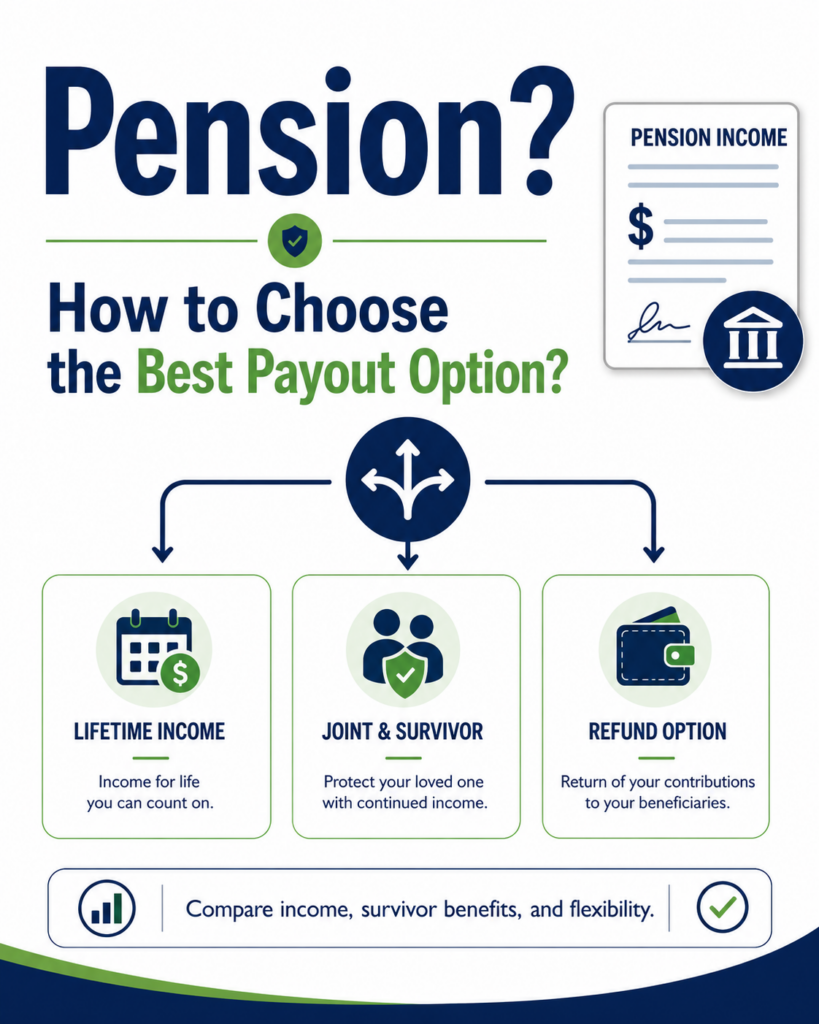

1. Understand What Each Pension Payout Option Actually Means

The first step is understanding the pension options in front of you.

This may sound simple, but it’s where many people get stuck. Pension paperwork can be loaded with terms that sound similar but have very different consequences.

Common pension payout options may include:

- Single life annuity

- Joint and survivor annuity

- 100% survivor option

- 75% survivor option

- 50% survivor option

- Life with period certain

- Lump sum

- Partial lump sum

- Level income option

- Pop-up option

Each option answers a different question.

A single life annuity usually pays income for your life only. It may provide the highest monthly amount, but payments may stop when you die. If you’re married and your spouse depends on that income, this can create a serious problem.

A joint and survivor annuity usually pays income for your life and then continues some level of income to your spouse after you die. The trade-off is that the monthly benefit is usually lower while you’re both alive.

A 100% joint and survivor option may continue the same monthly amount to your spouse after your death. A 75% option may continue 75% of the amount. A 50% option may continue half. The more survivor protection you choose, the lower the starting monthly benefit may be.

A life with period certain option may pay for your life, but guarantees payments for a set period, such as 10 or 20 years. If you die before that period ends, payments may continue to a beneficiary until the period is complete.

A lump sum gives you a one-time payment instead of monthly pension income. This may provide more flexibility, but it also shifts investment risk, withdrawal risk, and longevity risk onto you.

A partial lump sum may combine both approaches by giving you some monthly income and some money up front.

A level income option may temporarily increase pension income before Social Security starts and then reduce pension income later. This can smooth income, but it must be understood carefully.

A pop-up option may increase the pension benefit if the spouse dies first, depending on the pension rules. Not all plans offer this.

The most important thing is to avoid choosing based only on the first number you see.

The highest monthly pension is not always the best pension.

The lowest monthly pension is not always the safest pension.

The lump sum is not always better or worse.

Each option has a job. Your job is to figure out which one fits your household.

Before making a pension election, you should ask:

- What happens if I die first?

- What happens if my spouse dies first?

- Does the income continue?

- How much does the income continue?

- Is there any inflation adjustment?

- Can I change this later?

- Does this affect my spouse’s financial security?

- How does this interact with Social Security?

- How does this affect investment withdrawals?

- What happens if we both live a long time?

A Retirement Readiness Review can help you compare the pension options side by side so you understand what each one really means.

- Pension options can have very different survivor outcomes.

- The highest monthly payment may provide the least protection.

- Joint and survivor options may reduce income now but protect a spouse later.

- Lump sums provide flexibility but shift more responsibility to you.

- You should understand every option before making a permanent election.

2. Compare the Monthly Income Difference

The second step is comparing the monthly income difference between the options.

This is where the decision often gets emotional.

The single life option may show the largest monthly payment. That can be tempting. After all, who doesn’t want more monthly income in retirement?

But you need to ask what you’re giving up to get that higher payment.

For example, suppose your pension options look like this:

- Single life option: $4,000 per month

- 100% joint and survivor: $3,500 per month

- 75% joint and survivor: $3,650 per month

- 50% joint and survivor: $3,800 per month

At first glance, the $4,000 option looks best. It gives you the most income now.

But if the single life option stops when you die, your spouse may lose that income completely. If your spouse depends on it, the “best” monthly option could become the worst survivor option.

Now look at it another way.

Choosing the 100% joint and survivor option may cost $500 per month compared with the single life option. That’s $6,000 per year of lower income while both spouses are alive.

The question is whether that cost is worth the survivor protection.

Sometimes it is.

Sometimes it isn’t.

If your spouse has their own strong pension, Social Security, investments, and income sources, you may not need as much survivor protection from your pension. But if your spouse would struggle without your pension, the joint and survivor option may be very important.

You also need to compare the income difference over time.

Ask:

- How much income do we give up each month for survivor protection?

- How much would the survivor receive if one spouse dies?

- How long would the survivor need that income?

- Could investments replace the lost pension income?

- Would life insurance fill the gap?

- How does Social Security change after the first death?

- What expenses remain for the survivor?

The pension decision should not be based only on the “cost” of the survivor option. It should be based on the consequence of not choosing it.

For example, giving up $500 per month may feel painful. But losing $4,000 per month after the pension holder dies could be devastating.

That doesn’t mean the most protective option is always best. Some couples may reasonably choose a lower survivor percentage if they have enough assets to cover the gap. Others may choose full survivor protection because the pension is a major part of household income.

The right answer depends on your numbers.

You should also consider inflation.

Some pensions have cost-of-living adjustments. Many do not. If your pension does not increase over time, the purchasing power of the monthly payment may decline. That means you may need investments or other income sources to help cover rising expenses.

A Retirement Readiness Review can help compare the income difference between pension options and test whether your plan still works under each one.

- The largest pension check may come with less survivor protection.

- Joint and survivor options may reduce income today to protect income later.

- The cost of survivor protection should be compared with the risk of income loss.

- Inflation can reduce the value of fixed pension income over time.

- The best choice depends on the full household income plan.

3. Protect the Surviving Spouse

The third step is protecting the surviving spouse.

This may be the most important part of the pension decision for married couples.

Retirement income often changes dramatically after one spouse dies. One Social Security check may go away. Pension income may reduce or stop. Taxes may change. Investment withdrawals may need to increase. But many household expenses may remain.

The mortgage or rent may not change. Property taxes may not change. Home insurance may not change. Utilities may drop a little, but not by half. Healthcare costs, transportation, groceries, home maintenance, and basic living expenses may still be significant.

That means the surviving spouse may need more protection than couples realize.

This is why a pension election should be tested for both spouses.

You should test:

- What happens if you die first?

- What happens if your spouse dies first?

- What income continues?

- What income stops?

- What happens to Social Security?

- What happens to taxes?

- How much will the survivor need each month?

- Will the survivor need to withdraw more from investments?

- Will the survivor have enough cash?

- Would the survivor need to downsize?

- Would life insurance help?

This is not about being negative. It’s about being responsible.

One spouse will likely outlive the other. That means survivor planning is not a remote possibility. It’s a normal part of retirement planning.

Pension survivor options can help solve this problem, but they come with trade-offs.

A 100% joint and survivor option may provide maximum income continuity for the surviving spouse, but it usually lowers the monthly benefit while both spouses are alive.

A 50% joint and survivor option may provide more income now but less survivor income later.

A single life option may provide the highest income while the pension holder is alive but may leave the spouse with no pension income.

This is why pension decisions should be coordinated with Social Security claiming decisions.

If the higher-earning spouse delays Social Security, that may increase the potential survivor benefit. If the pension also has a strong survivor option, the surviving spouse may be much better protected.

But if the pension stops and the smaller Social Security check goes away, the surviving spouse could face a major income drop.

You should also consider which spouse is more financially experienced.

If one spouse handles all the money, the other spouse should still understand the income plan. The pension option should not leave the less financially involved spouse with a complicated situation they’re not prepared to manage.

One of the best gifts you can give your spouse is a retirement income plan they can understand and rely on.

A Retirement Readiness Review can help test the survivor scenario so you can see whether the pension election protects both spouses.

- Pension decisions can greatly affect the surviving spouse.

- A single life option may create survivor income risk.

- Joint and survivor options may provide important protection.

- Survivor planning should include Social Security, taxes, and expenses.

- The plan should be understandable for both spouses.

4. Decide Whether a Lump Sum Gives You More Flexibility or More Risk

The fourth step is deciding whether a lump sum is better than monthly pension income.

Some pension plans offer a lump sum option. This can be attractive because it gives you control of the money. You may be able to invest it, roll it into an IRA if eligible, use it for income, leave it to heirs, or keep more flexibility.

But a lump sum also shifts responsibility to you.

With monthly pension income, the employer or pension plan is responsible for paying the promised benefit according to the plan terms. With a lump sum, you become responsible for investing, withdrawing, managing taxes, and making the money last.

That’s a big trade-off.

A lump sum may be attractive if:

- You want more control.

- You have other guaranteed income sources.

- You want to leave money to heirs.

- You’re comfortable managing investments.

- You have a shorter life expectancy.

- You want more flexibility for large expenses.

- You have strong financial discipline.

- You want to coordinate withdrawals with taxes.

A monthly pension may be attractive if:

- You want predictable income.

- You worry about outliving your money.

- You don’t want to manage investments.

- Your spouse needs stable income.

- You have a long life expectancy.

- You want more income certainty.

- You already have enough investment flexibility elsewhere.

The lump sum decision should not be based only on the size of the lump sum.

You need to compare it with the value of the monthly pension.

For example, if the pension offers $4,000 per month for life, how much would you need to invest to reasonably produce that income for the rest of your life? What return would you need? What happens if markets perform poorly? What happens if you live to 95? What happens if inflation rises? What happens if your spouse outlives you by 20 years?

The lump sum can feel powerful because you see a large number. But large numbers can shrink quickly if withdrawals, market declines, taxes, and spending are not managed carefully.

On the other hand, a monthly pension can feel safe, but it may lack flexibility. If you need a large amount for healthcare, home repairs, or helping family, the monthly pension may not provide easy access to extra funds.

That’s why the decision is not simple.

A lump sum gives you flexibility and control.

A monthly pension gives you predictable income.

The best choice depends on which problem you’re trying to solve.

You should also consider pension plan security. Some private pensions may be protected by the Pension Benefit Guaranty Corporation up to certain limits, but guarantees have rules and limits. Public pensions operate under different systems. This doesn’t mean you should distrust your pension, but it does mean plan strength and protections may be part of the decision.

A Retirement Readiness Review can help compare the lump sum against monthly pension options so you can understand the trade-offs.

- Lump sums provide control and flexibility.

- Monthly pensions provide predictable income.

- Lump sums shift investment and longevity risk to you.

- Monthly pensions may provide less liquidity.

- The best choice depends on your income needs, risk tolerance, and goals.

5. Test Each Option Inside Your Full Retirement Plan

The fifth and most important step is testing each pension option inside your full retirement plan.

This is where many people make mistakes.

They look at the pension choices in isolation. They compare the monthly amounts and choose the one that feels best.

But your pension is only one piece of your retirement income plan.

It should be coordinated with:

- Social Security

- Investment withdrawals

- IRA and 401(k) accounts

- Roth accounts

- Taxable brokerage accounts

- Cash reserves

- Healthcare costs

- Medicare premiums

- Taxes

- Inflation

- Survivor needs

- Legacy goals

- Insurance

- Long-term care risk

A pension option that looks best by itself may not be best when combined with everything else.

For example, if you have a strong pension and strong Social Security, you may be able to invest more aggressively or withdraw less from your portfolio.

If you choose a smaller pension with survivor protection, you may need more investment withdrawals early in retirement.

If you choose a lump sum, your portfolio may become larger, but your guaranteed income may be smaller.

If you choose a single life pension, your income may look good while you’re alive, but your spouse may need more investment withdrawals after your death.

Each option changes the rest of the plan.

That’s why testing matters.

You should compare pension options under different scenarios:

- Both spouses live a long life.

- The pension holder dies early.

- The spouse dies first.

- Markets perform poorly early in retirement.

- Inflation is higher than expected.

- Healthcare costs rise.

- One spouse needs long-term care.

- Taxes increase.

- Social Security is claimed early.

- Social Security is delayed.

- The lump sum earns less than expected.

- The survivor lives 20 years after the first death.

This is how you move from guessing to planning.

You’re not trying to predict the future perfectly. You’re trying to see which pension option holds up best under the situations that matter most.

The best pension payout option should help you answer:

- Can we pay our bills?

- Can the surviving spouse stay financially secure?

- Do we have enough flexibility?

- Are we taking too much investment risk?

- Are we giving up too much income?

- Are taxes manageable?

- Can we sleep at night?

That last question matters.

Retirement income decisions are not just mathematical. They’re emotional too. Some retirees feel better with guaranteed income. Others feel better with flexibility. Some want maximum survivor protection. Others want more control and legacy value.

A good plan should respect both the numbers and your comfort level.

A Retirement Readiness Review can help test each pension payout option before you make a decision that may be permanent.

- Pension options should be tested inside the full retirement plan.

- Social Security, investments, taxes, and survivor planning all matter.

- Different options create different risks.

- The best option should work in multiple scenarios.

- The goal is confidence, not just the highest monthly check.

Conclusion

Choosing the best pension payout option is not just about picking the largest monthly payment.

It’s about choosing the option that best supports your retirement income, protects your spouse, manages risk, and fits your long-term goals.

A single life pension may offer the highest check, but it may leave a spouse exposed. A joint and survivor option may reduce income today but provide valuable protection later. A lump sum may offer flexibility and legacy potential, but it also puts investment and withdrawal risk on your shoulders.

There is no one-size-fits-all answer.

The best pension option depends on your income needs, health, spouse, investments, taxes, Social Security, risk tolerance, and desire for flexibility.

If you’re preparing to retire and need to choose a pension payout option, this is not a decision to rush. Once the election is made, you may not be able to change it.

A Retirement Readiness Review can help you compare your pension options, test survivor scenarios, evaluate lump sum versus monthly income, and see how each choice affects your overall retirement plan.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before making a decision that could affect the rest of your life.

FAQs

Is the highest monthly pension payout always the best option?

No. The highest monthly payout is often a single life option, which may stop when the pension holder dies. That may be fine for some people, but it can create a serious income problem for a surviving spouse. The best option depends on your full retirement plan.

Should I choose a lump sum or monthly pension?

It depends. A lump sum may provide more flexibility, control, and legacy potential, but it also shifts investment and longevity risk to you. A monthly pension may provide more predictable income, but less liquidity. The decision should be tested before you choose.

What is a joint and survivor pension option?

A joint and survivor pension option provides income while the pension holder is alive and then continues some level of income to the surviving spouse after the pension holder dies. The monthly amount is usually lower than a single life option, but it can provide valuable spouse protection.