RMDs Explained: How They May Affect Your Retirement Plan

Required minimum distributions, often called RMDs, can feel like one of those retirement rules people don’t think about until they’re forced to deal with it.

For years, you may have saved into traditional IRAs, 401(k)s, 403(b)s, SEP IRAs, or SIMPLE IRAs. You got tax benefits while saving, your money grew tax-deferred, and eventually retirement arrived. But at a certain age, the IRS generally says you can’t leave all that pre-tax money untouched forever. You must begin taking money out.

That’s where RMDs come in. In this article, we’ll walk through what RMDs are, when they start, how they can affect taxes, Social Security, Medicare premiums, Roth conversions, and your overall retirement income plan.

Short on Time? Here’s the Key Point / Summary

RMDs are required withdrawals from certain retirement accounts. They can affect your retirement plan because they may increase taxable income, change your withdrawal strategy, affect Medicare premiums, make more of your Social Security taxable, and reduce tax flexibility later in retirement.

Here are the five key things we’ll cover:

- RMDs force taxable withdrawals from certain retirement accounts.

- RMDs can increase your tax bill in retirement.

- RMDs may affect Social Security taxation and Medicare premiums.

- RMD planning should start before RMDs begin.

- Roth conversions, charitable giving, and withdrawal planning may help manage RMDs.

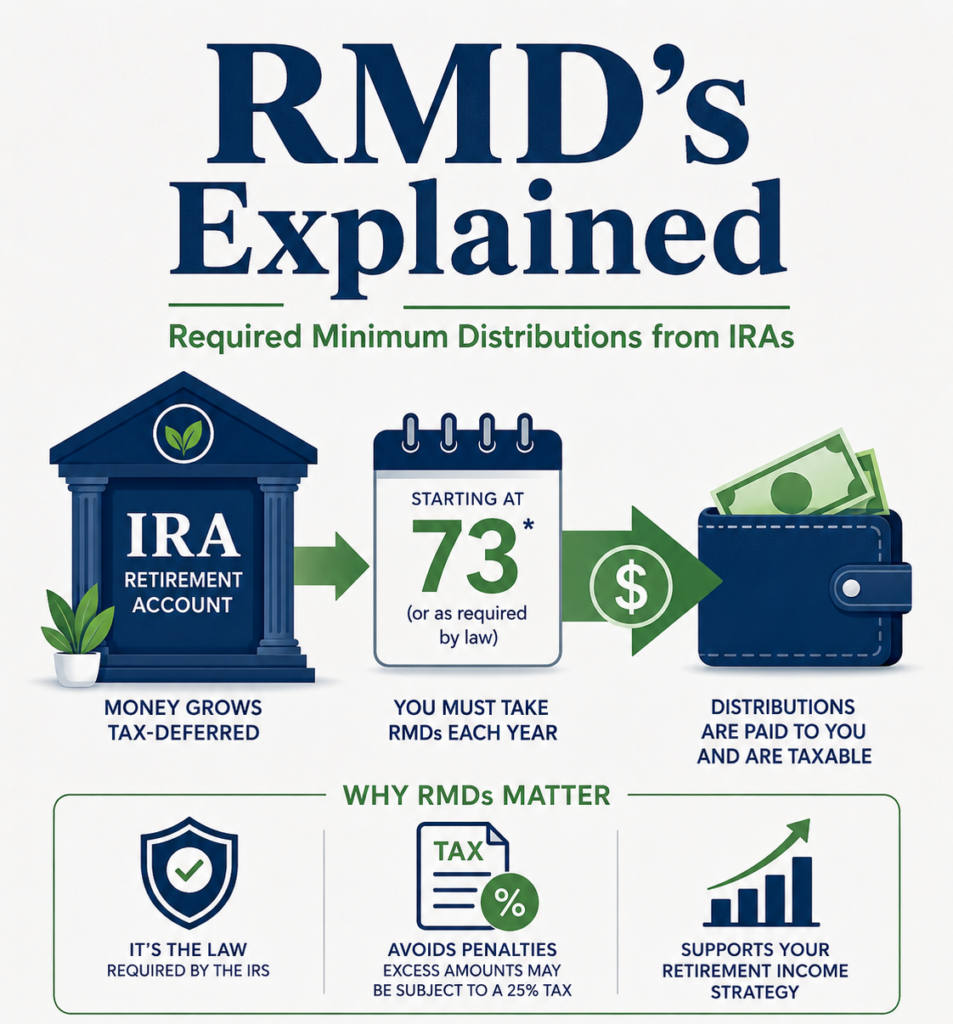

Required minimum distributions are minimum amounts that IRA and retirement plan account owners generally must withdraw each year starting with the year they reach age 73. Traditional IRAs, SEP IRAs, and SIMPLE IRAs generally require RMDs once the account holder reaches age 73, even if retired.

Roth accounts are different. You’re generally not required to take withdrawals from Roth IRAs or designated Roth accounts in a 401(k) or 403(b) while the account owner is alive, although beneficiaries may still be subject to RMD rules.

If you’re within a few years of retirement, a Retirement Readiness Review can help you test how future RMDs may affect taxes, income, Social Security, Medicare premiums, and your long-term retirement plan.

What Are RMDs and Why Do They Matter?

RMD stands for required minimum distribution.

It’s the minimum amount you must withdraw each year from certain retirement accounts once you reach the applicable starting age.

RMDs matter because they can force income into your tax return even if you don’t need the money.

That’s the part many retirees don’t like.

You may have enough income from Social Security, pensions, annuities, or taxable accounts. But once RMDs begin, the IRS may still require you to pull money from traditional retirement accounts. Those withdrawals are generally taxable as ordinary income.

That can affect more than just your tax bill.

RMDs can also affect:

- Social Security taxation

- Medicare IRMAA surcharges

- Investment withdrawal strategy

- Roth conversion planning

- Charitable giving strategy

- Spouse survivor planning

- Estate planning

- Cash flow

- Tax brackets

The key is to avoid waiting until age 73 to think about RMDs.

By then, many of your best planning years may already be behind you.

1. RMDs Force Taxable Withdrawals From Certain Retirement Accounts

The first thing to understand is that RMDs apply to many pre-tax retirement accounts.

These may include:

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- Traditional 401(k)s

- Traditional 403(b)s

- 457(b) plans

- Profit-sharing plans

- Other employer retirement plans

The basic idea is simple.

If you received tax benefits when money went into the account, the IRS eventually wants taxes paid when money comes out.

That’s why RMDs exist.

During your working years, you may have contributed pre-tax money to a 401(k) or IRA. That may have reduced your taxable income at the time. The money then grew tax-deferred. But tax-deferred does not mean tax-free. It means taxes were delayed.

RMDs are one way the IRS eventually forces some of that delayed taxable income to come out.

RMDs are minimum amounts that account owners generally must withdraw annually starting with the year they reach age 73.

This is important because RMDs are not optional.

If you don’t take the required amount, there can be penalties. The penalty for missing an RMD can generally be 25% of the amount not taken, and it may be reduced to 10% if corrected within a certain timeframe.

That’s a painful mistake.

The amount you must withdraw is usually based on your account balance at the end of the prior year and an IRS life expectancy factor. As you get older, the percentage you’re required to withdraw generally increases.

This means RMDs can become larger later in retirement.

For example, if your IRA balance grows significantly during your 60s and early 70s, your future RMDs may be larger than expected. That can create tax problems later, especially if you also have Social Security, pensions, investment income, or annuity income.

This is why RMDs should not be treated as a surprise.

They should be projected before they begin.

A Retirement Readiness Review can help estimate future RMDs and show how they may affect your retirement income plan.

- RMDs apply to many traditional pre-tax retirement accounts.

- RMDs generally begin at age 73 for many retirees.

- RMDs are usually taxable as ordinary income.

- Missing an RMD can create penalties.

- RMD amounts may grow as you age.

2. RMDs Can Increase Your Tax Bill in Retirement

The second thing to understand is that RMDs can increase your tax bill.

This is one of the biggest reasons retirees need to plan ahead.

Many people assume they’ll automatically be in a much lower tax bracket in retirement. Sometimes that’s true. But it’s not always true.

Retirement income can come from several sources:

- Social Security

- Pensions

- Traditional IRA withdrawals

- 401(k) withdrawals

- RMDs

- Annuity income

- Interest

- Dividends

- Capital gains

- Rental income

- Part-time work

Once RMDs begin, they may add taxable income on top of everything else.

That can push you into a higher tax bracket or reduce your ability to control taxable income.

For example, suppose you have Social Security, a pension, and investment income. You may already have enough cash flow to live comfortably. But once RMDs begin, you may be forced to withdraw additional taxable money from your IRA.

Even if you reinvest that money in a taxable account, the withdrawal itself still generally counts as taxable income.

This is why RMDs can be frustrating.

You may not need the money, but you may still have to pay tax on it.

RMDs can also create a compounding tax problem.

If your IRA keeps growing, future RMDs may become larger. Larger RMDs can create more taxable income. More taxable income can affect Social Security taxation and Medicare premiums. Higher taxes and premiums can increase the amount you need to withdraw.

One decision touches another.

This is especially important for couples.

While both spouses are alive, they may file jointly and have wider tax brackets. But when one spouse dies, the survivor may eventually file as single. If the survivor still has large IRA balances and RMDs, the tax burden may become more painful.

That’s one reason RMD planning is also survivor planning.

The goal is not necessarily to avoid all taxes. That’s usually impossible.

The goal is to avoid being forced into higher taxes later because you ignored the problem earlier.

A Retirement Readiness Review can help compare different withdrawal strategies before RMDs begin, including whether earlier IRA withdrawals or Roth conversions may help manage future taxes.

- RMDs can increase taxable income.

- Higher taxable income can push retirees into higher tax brackets.

- RMDs may become larger later in retirement.

- Surviving spouses may face higher tax pressure.

- RMD planning should be part of tax planning.

3. RMDs May Affect Social Security Taxation and Medicare Premiums

The third thing to understand is that RMDs can affect more than your income tax bracket.

They may also affect Social Security taxation and Medicare premiums.

Social Security benefits may be taxable depending on your combined income. If RMDs increase your taxable income, they may also cause more of your Social Security benefit to be taxable.

This surprises many retirees.

They think of Social Security, IRA withdrawals, and Medicare as separate issues. But in retirement, they’re connected.

RMDs can also affect Medicare premiums through IRMAA.

IRMAA stands for Income-Related Monthly Adjustment Amount. It is an extra Medicare surcharge that higher-income retirees may pay on top of Medicare Part B and Part D premiums.

Because RMDs increase income, they may push some retirees into a higher Medicare premium bracket.

This can be especially frustrating because IRMAA generally uses a two-year income lookback. So a large RMD year may affect Medicare costs later.

For example, if your RMDs increase your modified adjusted gross income, you may pay higher Medicare premiums in a future year. This is not always a reason to avoid income, but it is a reason to plan carefully.

This is where RMD planning connects to:

- Social Security timing

- Roth conversions

- Medicare IRMAA

- Tax brackets

- Charitable giving

- Investment withdrawals

- Pension income

- Survivor planning

For example, if you retire at 62 and don’t start RMDs until 73, the years before RMDs begin may provide a planning window. You may be able to take controlled IRA withdrawals, do Roth conversions, or manage capital gains before RMDs force more income later.

But if you wait until RMDs begin, your flexibility may be lower.

The important point is that RMDs don’t just affect one line on your tax return.

They can affect your full retirement income picture.

That’s why you want to test RMDs before they happen.

A Retirement Readiness Review can help you see whether future RMDs may affect Social Security taxation, Medicare premiums, and your after-tax retirement income.

- RMDs can make more of Social Security taxable.

- RMDs may affect Medicare IRMAA premiums.

- Medicare premium increases can show up later because of income lookbacks.

- RMDs should be coordinated with Social Security and Medicare planning.

- The best retirement plan looks at after-tax, after-premium income.

4. RMD Planning Should Start Before RMDs Begin

The fourth thing to understand is that RMD planning should start before age 73.

Waiting until RMDs begin is one of the biggest mistakes retirees make.

The years after retirement but before RMDs can be some of the most valuable planning years you have.

Why?

Because your taxable income may be lower.

You may no longer have wages. You may not have started Social Security yet. You may not have pension income yet. Required minimum distributions may not have started yet.

That creates a window where you may have more control over taxable income.

During these years, you may consider:

- Controlled traditional IRA withdrawals

- Roth conversions

- Capital gain harvesting

- Charitable giving strategies

- Delaying Social Security

- Using taxable accounts strategically

- Building Roth flexibility

- Managing future RMD exposure

Not all of these strategies will be right for everyone. But they should be tested.

For example, some retirees avoid IRA withdrawals before RMDs because they don’t want to pay taxes. That sounds reasonable, but it can backfire.

If the IRA grows untouched for years, future RMDs may become larger. Those larger RMDs may create higher taxable income later when you have less flexibility.

Sometimes paying some tax earlier may reduce larger tax problems later.

Other times, it may not.

That’s why this is not about rules of thumb. It’s about testing.

A good RMD plan should answer:

- What are my projected RMDs?

- What will my tax bracket look like before and after RMDs?

- Should I withdraw from my IRA before RMDs begin?

- Should I do Roth conversions?

- How would conversions affect IRMAA?

- Should I delay Social Security?

- What happens if one spouse dies?

- How much income will the surviving spouse have?

- What happens to Medicare premiums?

- What happens to heirs?

That last question matters because RMDs also connect to estate planning.

If you leave a large traditional IRA to heirs, they may have to withdraw the money under inherited IRA rules. Depending on their tax situation, that can create a burden.

Roth assets may be more attractive for heirs in some situations, though inherited Roth accounts may still have distribution rules.

The key is that RMD planning is not just about one year.

It’s about your lifetime tax picture and your family’s financial outcome.

A Retirement Readiness Review can help identify your best planning window before RMDs begin.

- RMD planning should begin before age 73.

- The years between retirement and RMDs can be valuable tax planning years.

- Roth conversions may be useful in lower-income years.

- Earlier IRA withdrawals may reduce future RMD pressure.

- Planning should include taxes, Medicare, Social Security, and heirs.

5. Roth Conversions, Charitable Giving, and Withdrawal Planning May Help Manage RMDs

The fifth thing to understand is that RMDs can often be managed with better planning.

You may not be able to eliminate RMDs completely, but you may be able to reduce their impact.

Three common planning tools are:

- Roth conversions

- Qualified charitable distributions

- Strategic withdrawal planning

A Roth conversion moves money from a traditional IRA into a Roth IRA. The converted amount is generally taxable in the year of conversion, but future qualified Roth withdrawals may be tax-free.

This can help reduce future RMDs because money moved into a Roth IRA is no longer sitting in the traditional IRA. Roth IRAs do not require withdrawals during the original owner’s lifetime.

But Roth conversions are not automatically good.

They can increase taxable income, trigger IRMAA, affect Social Security taxation, and create a tax bill now. They should be tested carefully.

A qualified charitable distribution, often called a QCD, may help charitably inclined retirees. A QCD allows eligible IRA owners to transfer money directly from an IRA to a qualified charity. When done correctly, the distribution may satisfy part or all of an RMD without being included in taxable income.

This can be valuable for retirees who already give to charity and don’t need all of their RMD income.

Strategic withdrawal planning is also important.

Instead of waiting for RMDs, some retirees may take controlled withdrawals earlier. Others may use a mix of taxable accounts, IRA accounts, Roth accounts, and cash to manage taxable income year by year.

The best strategy depends on your goals.

You may want to:

- Reduce future RMDs

- Manage tax brackets

- Avoid surprise Medicare premiums

- Protect a surviving spouse

- Improve estate planning

- Create Roth flexibility

- Support charities

- Reduce taxable income later

The key is that RMD planning should be proactive.

Once RMDs begin, you can still plan. But you may have fewer options than you had earlier.

This is why retirees should not wait until the year they turn 73 to start thinking about RMDs.

A Retirement Readiness Review can help compare Roth conversions, charitable giving, and withdrawal strategies so you can decide what makes sense for your plan.

- Roth conversions may reduce future RMDs but create taxes now.

- Roth IRAs do not require RMDs during the original owner’s lifetime.

- QCDs may help charitably inclined retirees manage taxable income.

- Strategic withdrawals may reduce future RMD pressure.

- RMD planning should be coordinated with the full retirement plan.

Conclusion

RMDs can have a bigger impact on your retirement plan than many people expect.

They force taxable withdrawals from certain retirement accounts. They can increase your tax bill. They may affect Social Security taxation and Medicare premiums. They can reduce flexibility later in retirement. And they may create a bigger tax burden for a surviving spouse or heirs.

But RMDs don’t have to be a surprise.

The best time to plan for RMDs is before they begin. The years after retirement but before RMDs may create valuable planning opportunities. Roth conversions, controlled IRA withdrawals, charitable giving, and tax-aware withdrawal planning may help reduce future problems.

The goal is not to avoid taxes completely. The goal is to manage taxes intelligently over your lifetime.

If you’re within a few years of retirement and want to understand how RMDs may affect your plan, a Retirement Readiness Review can help. We’ll look at your IRA balances, Social Security timing, tax brackets, Medicare premiums, Roth conversion opportunities, survivor planning, and withdrawal strategy.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before RMDs start making decisions for you.

FAQs

What age do RMDs start?

Required minimum distributions generally begin for IRA and retirement plan account owners starting with the year they reach age 73. Traditional IRA, SEP IRA, and SIMPLE IRA owners generally must begin RMDs once they reach age 73, even if retired.

Do Roth IRAs have RMDs?

Roth IRAs generally do not require withdrawals during the original owner’s lifetime. Withdrawals are generally not required from Roth IRAs or designated Roth accounts in a 401(k) or 403(b) plan while the account owner is alive, although beneficiaries may be subject to RMD rules.

What happens if I miss an RMD?

If you miss an RMD or don’t withdraw enough, there can be a penalty. The penalty is generally 25% of the amount not taken, but it may be reduced to 10% if corrected within a certain timeframe.