What If the Market Crashes Right After You Retire?

A market crash is painful at any age. But a market crash right after you retire can be especially dangerous.

Why?

Because once you retire, you’re no longer just investing for growth. You’re also taking income. That means if your portfolio drops and you’re pulling money out at the same time, the damage can be much harder to recover from.

This is called sequence-of-returns risk, and it’s one of the biggest risks retirees face in the first few years of retirement. In this article, we’ll walk through why an early retirement market crash can be so dangerous, what mistakes to avoid, and how to prepare before it happens.

Short on time? Here is the Key Point / Summary

A market crash right after retirement can hurt more than a crash during your working years because you may be taking withdrawals from a falling portfolio. That can force you to sell investments at lower prices, reduce the portfolio’s ability to recover, and create stress at the exact moment you need confidence.

Here are the five key things we’ll cover:

- Understand why the first few retirement years are so important.

- Avoid selling investments in a panic.

- Build an income plan before the market drops.

- Keep enough safe money to cover short-term income needs.

- Test your retirement plan against a bad market scenario.

The biggest mistake is assuming that average returns will save you. In retirement, the order of returns matters. Two retirees can earn the same average return over time, but the one who suffers bad returns early while taking withdrawals may have a much worse outcome.

If you’re within a few years of retirement, a Retirement Readiness Review can help test your plan against a market crash before you give up your paycheck.

What Happens If the Market Crashes Right After You Retire?

If the market crashes right after you retire, your retirement plan may face pressure from two directions at once.

First, your portfolio value may fall.

Second, you may still need income.

That combination can be dangerous.

During your working years, a market crash is painful, but you may still have a paycheck. You may be able to keep contributing, avoid withdrawals, and wait for the market to recover.

In retirement, the situation is different.

You may need monthly income for:

- Groceries

- Utilities

- Healthcare

- Taxes

- Insurance

- Travel

- Mortgage or rent

- Home repairs

- Transportation

If that income has to come from investments while the market is down, you may be forced to sell shares at lower prices. That can permanently damage the portfolio’s ability to recover.

The better question is not, “Will the market crash?”

The better question is:

If the market crashes early in retirement, where will your income come from?

1. Understand Why the First Few Retirement Years Are So Important

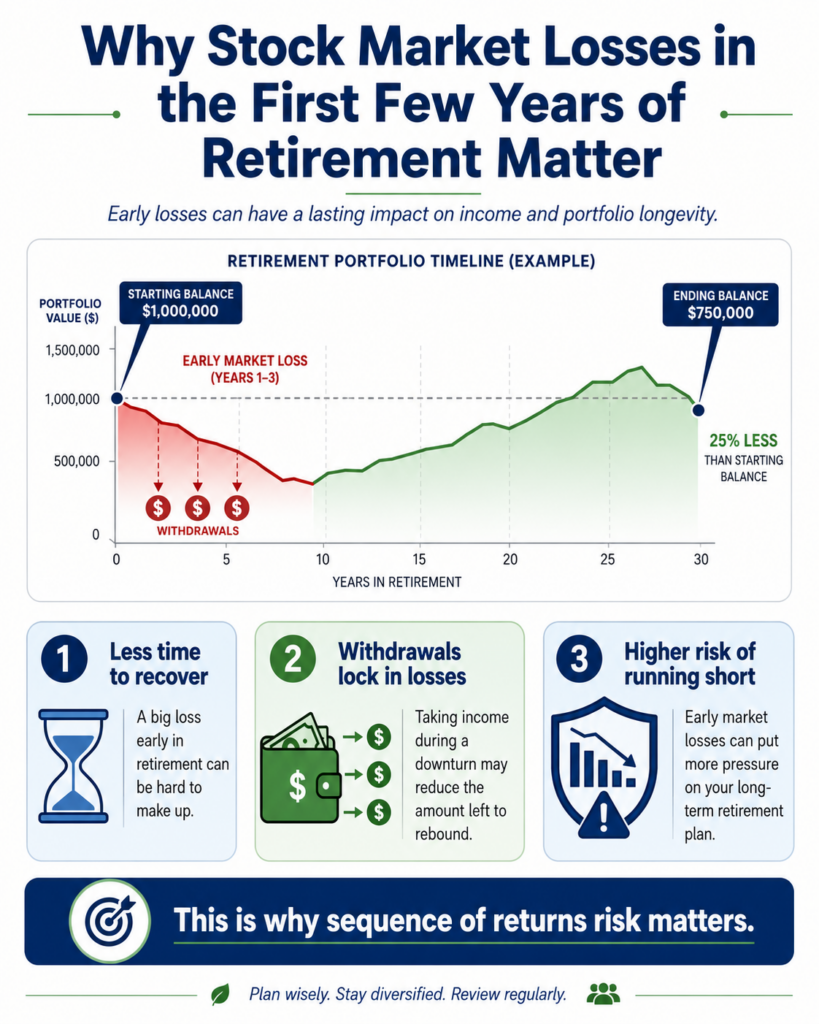

The first few years of retirement matter because they can set the tone for the rest of the plan.

This is where sequence-of-returns risk shows up.

Sequence-of-returns risk means the order of investment returns matters, especially when you’re taking withdrawals.

Here’s the simple version.

If you’re still working and not taking withdrawals, a market decline may be uncomfortable, but you may have time to recover. You may even be able to buy more shares while prices are lower.

But if you’re retired and taking money out, a decline can hurt more.

You may have to withdraw from a portfolio that has already dropped. That means you’re selling more shares to get the same amount of income. Once those shares are sold, they can’t participate in the recovery.

That can create long-term damage.

For example, imagine two retirees both start with $1,000,000 and both withdraw $50,000 per year.

One retiree gets strong market returns early and bad returns later.

The other retiree gets bad market returns early and strong returns later.

Even if the average return over time is similar, the outcomes can be very different. The retiree who gets bad returns early may run into trouble because withdrawals are happening while the portfolio is down.

That’s why the years right before and right after retirement are sometimes called the retirement red zone.

This is not the time to rely on hope.

It’s the time to build a plan.

A good plan should answer:

- What if the market falls 20% right after I retire?

- What if it falls 30%?

- What if it takes five years to recover?

- Where will income come from during the downturn?

- What expenses could be reduced?

- How much cash or conservative money do we need?

- Should we delay major spending?

- Should we delay retirement?

- Should we use guaranteed income for essential expenses?

The point is not to predict the next crash.

The point is to avoid being surprised by it.

A Retirement Readiness Review can help test how your plan handles bad returns early in retirement.

- The first few retirement years are extremely important.

- Bad returns early can be more damaging than bad returns later.

- Withdrawals during a market decline can reduce recovery potential.

- Average returns can be misleading in retirement.

- Your plan should test bad market timing before retirement begins.

2. Avoid Selling Investments in a Panic

The second thing to understand is that panic can make a bad market worse.

A market crash is scary. Nobody likes seeing account values fall. But emotional decisions during a downturn can turn temporary losses into permanent damage.

One of the most common mistakes is selling after the market has already dropped.

That may feel safe in the moment, but it can create a serious problem.

If you sell after the decline, you may lock in losses. Then, if the market recovers, you may miss the recovery because you moved to cash too late.

This is how retirees can get whipsawed.

They stay invested while the market falls, sell near the bottom because they can’t take the stress, and then hesitate to reinvest because they’re afraid the market will fall again.

That is a dangerous pattern.

It’s also understandable.

The problem is not that retirees are irrational. The problem is that they never had a plan for what to do during a downturn.

A good retirement plan should include a written market crash plan.

That plan should answer:

- What accounts do we use first?

- What investments do we avoid selling during a downturn?

- How much income is already covered by Social Security, pensions, or annuities?

- How much cash do we have available?

- What expenses can be paused?

- When do we rebalance?

- Who do we call before making major changes?

- What would cause us to change the plan?

This matters because you don’t want to make emotional decisions when fear is high.

You want the decision rules established before the market drops.

Another mistake is assuming you can handle risk because you handled it during your working years.

Risk feels different in retirement.

A 25% decline on a $1,000,000 portfolio means a temporary paper loss of $250,000. If you’re still working, that may hurt, but you may tell yourself you have time.

If you’re retired and taking income, that same decline can feel like your future is disappearing.

That’s why risk tolerance should be tested in dollars, not just percentages.

Ask yourself:

If my $1,000,000 portfolio dropped to $750,000 right after I retired, and I still needed $5,000 per month, what would I do?

That question gets real–fast.

A Retirement Readiness Review can help build a clear downturn plan so panic doesn’t become the strategy.

- Panic selling can turn temporary losses into permanent losses.

- Risk feels different once the paycheck stops.

- A written downturn plan can reduce emotional decisions.

- Know which accounts to use during a market decline.

- Test risk in dollars, not just percentages.

3. Build an Income Plan Before the Market Drops

The third step is building an income plan before the market drops.

This is one of the most important pieces of retirement planning.

You should not retire with only a pile of investments and a vague idea that you’ll “take what you need.”

That may work when markets are good.

It may not work when markets are bad.

A retirement income plan should clearly explain where your paycheck will come from.

Common income sources may include:

- Social Security

- Pensions

- Annuities

- Investment withdrawals

- Cash reserves

- Interest and dividends

- Rental income

- Part-time work

- Roth withdrawals

- Taxable account withdrawals

Each source has a different job.

Social Security may provide lifetime income.

A pension may provide predictable monthly income.

An annuity may help cover part of essential expenses.

Cash reserves may help you avoid selling investments during a downturn.

Investments may provide growth, inflation protection, lifestyle income, and legacy potential.

Roth accounts may provide tax flexibility.

The key is to coordinate these pieces before retirement.

One helpful way to think about this is separating your spending into two categories:

Essential expenses

These are the bills that must be paid:

- Housing

- Groceries

- Utilities

- Insurance

- Healthcare

- Taxes

- Transportation

- Basic living costs

Lifestyle expenses

These are important, but more flexible:

- Travel

- Hobbies

- Dining out

- Gifts

- Home improvements

- Entertainment

- Large optional purchases

Ideally, your essential expenses should be covered by more stable income sources, or at least backed by a plan that does not force you to sell stocks during a crash.

That does not mean every retiree needs an annuity or pension. But it does mean your essential income needs should be protected intentionally.

For example, if Social Security covers $4,500 per month and your essential expenses are $6,500 per month, you have a $2,000 monthly gap.

How will that gap be filled if the market crashes?

Will it come from cash?

A conservative bond ladder?

A Treasury ladder?

An annuity?

A pension?

A reduced spending plan?

A balanced portfolio withdrawal strategy?

There may be several acceptable answers.

But “we’ll figure it out later” is not one of them.

A Retirement Readiness Review can help organize your income sources and determine whether your essential expenses are protected.

- Retirement income should be planned before the market drops.

- Essential expenses and lifestyle expenses should be separated.

- Stable income sources can reduce pressure on investments.

- Cash reserves or conservative assets can help during downturns.

- Your retirement paycheck should not depend entirely on good markets.

4. Keep Enough Safe Money to Cover Short-Term Income Needs

The fourth step is keeping enough safe money to cover short-term income needs.

This is sometimes called a cash reserve, income bucket, or retirement paycheck reserve.

The idea is simple.

If the market crashes, you don’t want to be forced to sell long-term investments at depressed prices to pay short-term bills.

A cash reserve may help prevent that.

For example, you might keep one to three years of planned withdrawals in cash, high-quality short-term bonds, CDs, Treasury bills, or other conservative assets.

The right amount depends on your situation.

You may need a larger reserve if:

- Most of your income comes from investments.

- You have high essential expenses.

- You are very uncomfortable with market risk.

- You have no pension.

- You retire before Social Security starts.

- You have large upcoming expenses.

- You want more emotional comfort.

You may need a smaller reserve if:

- Social Security and pensions cover most expenses.

- You have guaranteed income.

- Your spending is flexible.

- You have a large portfolio relative to your needs.

- You can reduce withdrawals during downturns.

- You are comfortable with volatility.

The point is not to keep too much money in cash forever.

Cash has its own risk: inflation.

If too much of your money sits in cash for too long, it may lose purchasing power over time. That can be a problem in a 20- or 30-year retirement.

So, the goal is balance.

You need enough safe money to avoid forced selling, but enough growth-oriented money to fight inflation and support long-term income.

This is where a bucket strategy may help.

A simple version might look like this:

Bucket 1: Short-term money

Cash and conservative assets for near-term withdrawals.

Bucket 2: Mid-term money

Moderate investments or bonds designed to refill short-term reserves.

Bucket 3: Long-term growth money

Stocks or growth assets designed for inflation protection and long-term income.

This kind of structure may help retirees stay calm during market downturns because they can see where the next few years of income will come from.

But buckets should not be random.

They need to be connected to the withdrawal plan, tax plan, and investment strategy.

A Retirement Readiness Review can help determine how much safe money you may need before retiring.

- Safe money can help avoid selling stocks during a crash.

- Cash reserves may provide emotional and financial stability.

- Too much cash can create inflation risk.

- The right reserve depends on income sources and spending needs.

- A bucket strategy may help organize short-, mid-, and long-term money.

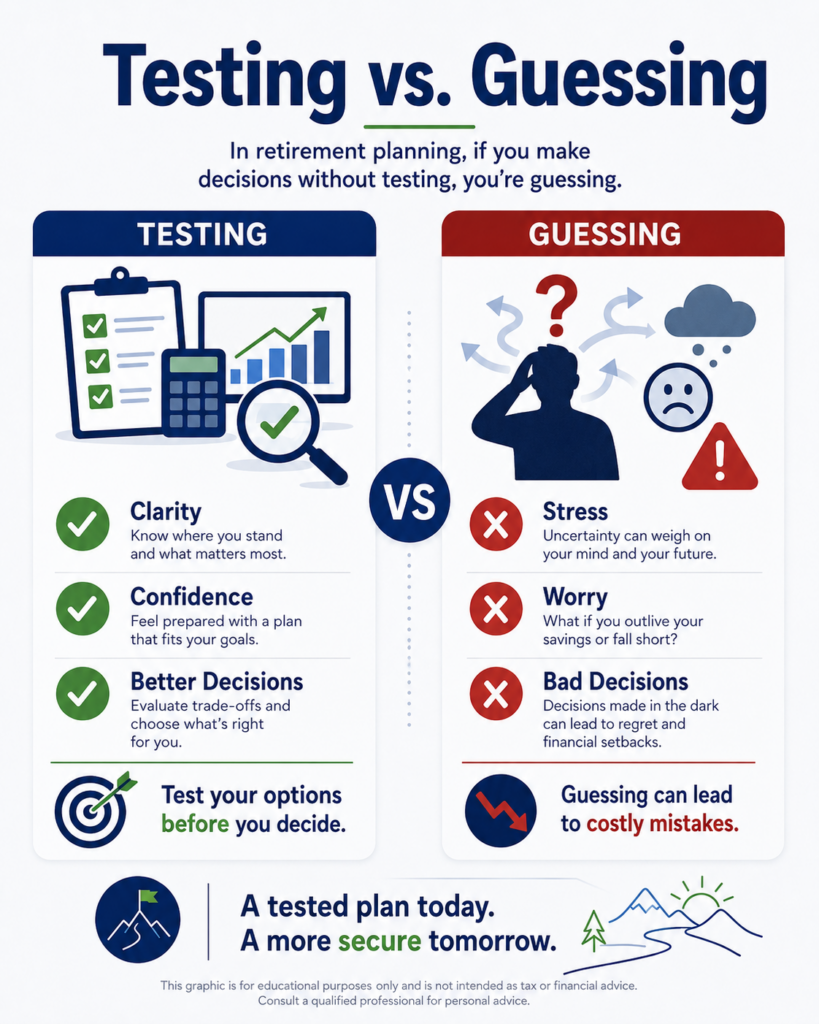

5. Test Your Retirement Plan Against a Bad Market Scenario

The fifth and most important step is testing your retirement plan against a bad market scenario.

This is where guessing ends and planning begins.

A plan that only works if markets behave nicely is not a strong plan.

Before you retire, you should test what happens if markets are bad early.

For example:

- What if the market drops 20% in year one?

- What if it drops 30% in the first two years?

- What if returns are poor for five years?

- What if inflation stays high during the downturn?

- What if healthcare costs rise at the same time?

- What if one spouse dies during the downturn?

- What if you need a major home repair?

- What if you retire before Social Security starts?

This type of stress testing can show weak spots.

Maybe your plan still works fine.

Great.

Maybe the plan works only if you reduce spending temporarily.

That is useful to know.

Maybe the plan fails if withdrawals continue at the same level during a downturn.

That means you need a better strategy.

Stress testing can help you decide whether to:

- Retire now or work longer.

- Delay Social Security.

- Reduce spending early in retirement.

- Build a larger cash reserve.

- Change investment allocation.

- Add guaranteed income.

- Use a Treasury or bond ladder.

- Keep more flexible expenses.

- Pay off debt before retirement.

- Create a written withdrawal plan.

This is the difference between hoping and knowing.

It’s not that the projections will be perfect. They won’t be.

But testing gives you a clearer picture of how your plan responds under pressure.

This is especially important for conservative retirees.

If you know a market crash would cause you to panic, you need to build a plan that reduces the need to panic.

That might mean a more conservative allocation. It might mean more guaranteed income. It might mean a larger cash reserve. It might mean working one more year. It might mean spending less early. It might mean delaying a big purchase.

The right answer depends on your numbers.

A Retirement Readiness Review can help test your retirement plan under market crash scenarios before you give up your paycheck.

- Stress test your plan before retirement.

- A plan should not depend on perfect market timing.

- Market crashes, inflation, healthcare costs, and survivor risk should be tested.

- Weak spots can often be fixed before retirement.

- Confidence comes from testing, not guessing.

Conclusion

A market crash right after retirement can be one of the most dangerous financial events a retiree faces.

Not because crashes are unusual. They’re part of investing.

The danger comes from combining a market decline with portfolio withdrawals. That’s where sequence-of-returns risk can damage a retirement plan.

The solution is not to live in fear or move everything to cash.

The solution is to prepare.

Understand why the first few retirement years matter. Avoid panic selling. Build an income plan before the market drops. Keep enough safe money for short-term needs. Test your retirement plan against bad market scenarios.

The goal is not to predict the next crash.

The goal is to know what you’ll do when it comes.

If you’re within a few years of retirement, a Retirement Readiness Review can help you test how your plan holds up if the market crashes right after you retire. We’ll look at income, investments, Social Security timing, taxes, cash reserves, survivor planning, and withdrawal strategy so you can make decisions with more confidence.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before the market puts your retirement plan under pressure.

FAQs

Why is a market crash worse right after retirement?

A market crash is more dangerous right after retirement because you may be withdrawing money from a falling portfolio. Selling investments during a decline can reduce the portfolio’s ability to recover and may increase the risk of running out of money.

What is sequence-of-returns risk?

Sequence-of-returns risk is the risk that poor investment returns occur early in retirement while you are taking withdrawals. Even if long-term average returns are reasonable, bad returns early can create lasting damage.

How can I protect my retirement from a market crash?

You can prepare by building a written income plan, keeping enough safe money for short-term withdrawals, avoiding panic selling, separating essential and lifestyle expenses, and stress-testing your plan against bad market scenarios.