Annuities vs. the 4% Rule: Which Income Strategy Wins?

One of the biggest retirement income questions is simple on the surface: How should you turn your savings into a paycheck?

For many retirees, the decision often comes down to two broad strategies. One strategy is using the 4% rule, where you withdraw from your investments each year. The other is using an annuity, where part of your savings may be turned into more predictable income.

The problem is that both strategies have strong opinions attached to them. Some people say the 4% rule gives you flexibility and growth. Others say annuities provide security and income you can’t outlive. The truth is, neither strategy automatically wins for everyone.

In this article, we’ll compare annuities and the 4% rule in plain English so you can understand the trade-offs before making a major retirement income decision.

Short on time? Here is the Key Point / Summary

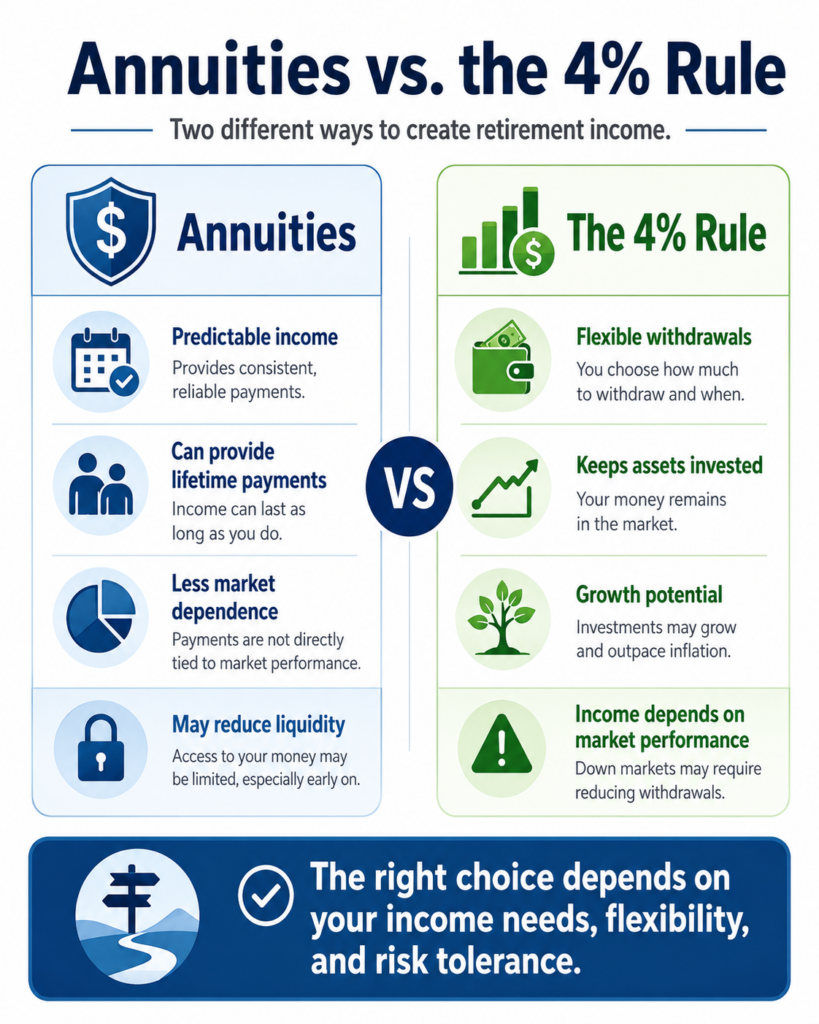

The 4% rule and annuities solve different retirement income problems.

The 4% rule is a withdrawal strategy that keeps your money invested and gives you flexibility, but it still exposes you to market risk and sequence-of-returns risk. Annuities can provide more predictable income, and in some cases lifetime income, but they may come with less liquidity, more complexity, fees, surrender charges, and trade-offs.

Here are the five key things we’ll cover:

- The 4% rule gives flexibility, but it isn’t a guarantee.

- Annuities can provide predictable income, but the details matter.

- Market risk and longevity risk are handled differently.

- Liquidity, taxes, inflation, and legacy goals can change the answer.

- The best strategy may be a blend of both.

The 4% rule is often used as a retirement spending guideline, but the “safe” withdrawal number can change depending on market assumptions, inflation, spending flexibility, and portfolio design.

Annuities can be useful but are often complex. Some annuities can have long surrender periods, fees, and liquidity restrictions that should be understood before committing money.

If you’re within a few years of retirement, a Retirement Readiness Review can help you compare annuities, the 4% rule, investment withdrawals, Social Security timing, taxes, and survivor income before you commit to one strategy.

Annuities vs. the 4% Rule: Which Income Strategy Wins?

The winning income strategy depends on what you need your money to do.

If you value flexibility, investment control, growth potential, and legacy planning, the 4% rule or another investment withdrawal strategy may be attractive.

If you value predictable income, lifetime cash flow, and reducing the fear of running out of money, an annuity may be worth considering.

But this decision is rarely either-or.

Most retirees want several things at once:

- Reliable income to pay the bills.

- Flexibility for travel, emergencies, and family needs.

- Growth potential to fight inflation.

- Protection from bad markets.

- Confidence they won’t outlive their money.

- A plan for the surviving spouse.

- Some money left for heirs or charity.

That’s why the better question is not, “Which strategy wins?”

The better question is:

Which strategy, or combination of strategies, gives you the best retirement income plan based on your real numbers?

1. The 4% Rule Gives Flexibility, But It Isn’t a Guarantee

The first thing to understand is how the 4% rule works.

The basic idea is simple. You withdraw about 4% of your portfolio in the first year of retirement. Then, in future years, you adjust that dollar amount for inflation.

For example, if you retire with $1,000,000, the 4% rule suggests a first-year withdrawal of about $40,000. If inflation is 3%, the next year’s withdrawal might increase to $41,200.

That sounds simple, and that’s part of its appeal.

The 4% rule gives retirees a starting point. It helps answer the question, “How much can I withdraw from my portfolio without running out too soon?”

But there are several problems with treating the 4% rule like a guarantee.

First, the 4% rule depends heavily on market performance.

If markets perform well early in retirement, the strategy may work beautifully. Your portfolio may continue growing, your withdrawals may feel comfortable, and you may still have assets left later in life.

But if markets perform poorly early in retirement, the plan can come under pressure.

That’s called sequence-of-returns risk.

This risk matters because bad returns early in retirement can be more damaging than bad returns later. If you’re withdrawing money while the portfolio is down, you may be selling investments at lower values. That can make it harder for the portfolio to recover.

Second, the 4% rule assumes discipline.

If the market is doing well, it can be tempting to spend more. If the market is down, it can be tempting to panic and sell. The strategy only works if you have a process and stick with it.

Third, the 4% rule may not match real-life spending.

Most retirees don’t spend in a perfectly straight line. Spending may be higher in the early “go-go” years of retirement, lower later, and then possibly higher again because of healthcare or long-term care costs.

Fourth, the 4% rule doesn’t automatically solve taxes.

A $40,000 withdrawal from a traditional IRA is not the same as $40,000 from a Roth IRA or taxable brokerage account. The after-tax income matters more than the gross withdrawal.

That doesn’t mean the 4% rule is bad.

It can be a useful starting point. But it should be tested, adjusted, and coordinated with the rest of your plan.

A Retirement Readiness Review can help test whether a portfolio withdrawal strategy can support your income needs under different market conditions.

- The 4% rule is a guideline, not a guarantee.

- It keeps your money flexible and invested.

- It exposes you to market and sequence-of-returns risk.

- It may need to be adjusted for taxes and real-life spending.

- It should be tested before retirement, not assumed.

2. Annuities Can Provide Predictable Income, But the Details Matter

The second thing to understand is how annuities work.

An annuity is a contract with an insurance company. Depending on the type of annuity, it may provide income for a set period, for your lifetime, or for the lifetimes of you and your spouse.

The biggest appeal is predictability.

Instead of wondering how much you can withdraw from your portfolio each year, an annuity may provide a stated income stream based on the contract terms.

That can be comforting for retirees who worry about running out of money.

Annuities may be especially useful when there is a gap between essential expenses and guaranteed income sources.

For example, suppose your basic retirement expenses are $7,000 per month. Social Security provides $4,500 per month. That leaves a $2,500 monthly gap for essential expenses.

You could fund that gap with investment withdrawals. Or you could use an annuity for part of that gap so more of your basic bills are covered by predictable income.

That can reduce the emotional pressure of market downturns.

If your basic expenses are covered, you may feel less tempted to panic when the market drops. Your investments can then be used more for inflation protection, lifestyle spending, emergencies, and legacy goals.

But annuities come with trade-offs.

The first trade-off is liquidity.

Some annuities have surrender charges, withdrawal limits, or restrictions on access to your money.

The second trade-off is complexity.

There are different types of annuities, including immediate annuities, deferred income annuities, fixed annuities, fixed indexed annuities, variable annuities, and registered index-linked annuities. Each one works differently.

The third trade-off is inflation.

Some annuity payments may not increase with inflation unless specific features are included. Those features may reduce the starting income amount.

The fourth trade-off is legacy.

Depending on the annuity type and payout option, there may be less money left for heirs. Some contracts include death benefits, refund features, or survivor options, but those usually affect the income amount or cost.

Annuities can be useful, but they should not be bought just because the word “guaranteed” sounds good.

You need to know what is guaranteed, what is not guaranteed, what it costs, and what you’re giving up.

A Retirement Readiness Review can help compare an annuity strategy against investment withdrawals before you buy a product.

- Annuities may provide predictable income.

- Some annuities can provide income for life.

- They may reduce pressure on your portfolio.

- They can involve liquidity limits, fees, and complexity.

- The contract details matter as much as the concept.

3. Market Risk and Longevity Risk Are Handled Differently

The 4% rule and annuities handle risk differently.

The 4% rule leaves more risk on your shoulders.

If markets perform well, you may benefit. Your portfolio can grow. You may have more flexibility. You may leave more money to heirs.

But if markets perform poorly, especially early in retirement, your plan may be pressured.

That means the 4% rule carries market risk.

It also carries longevity risk.

Longevity risk is the risk of living longer than expected and needing income for more years than planned. Living a long life is a blessing, but financially it means your money has to last longer.

With a 4% rule strategy, the portfolio has to do the heavy lifting. It must provide income, handle inflation, survive bad markets, and last for life.

Annuities can transfer some longevity risk to an insurance company.

If you purchase a lifetime income annuity, the income may continue for as long as you live, depending on contract terms. That can reduce the fear of outliving that portion of your income.

But transferring risk usually comes with a cost.

When you buy certain annuities, you may give up liquidity, control, upside potential, or legacy value in exchange for income guarantees.

There is no free lunch.

The 4% rule may be better if you value flexibility, market upside, and legacy potential.

Annuities may be better if you value predictable income and protection against living a very long time.

But many retirees need both.

You may need some money protected from longevity risk and some money invested for growth.

That’s why it helps to divide your retirement spending into categories.

Essential expenses may include:

- Housing

- Groceries

- Utilities

- Insurance

- Healthcare

- Transportation

- Taxes

Lifestyle expenses may include:

- Travel

- Hobbies

- Dining out

- Gifts

- Home improvements

- Entertainment

If predictable income covers essential expenses, your investment withdrawals may be used more flexibly for lifestyle expenses.

That can make market downturns easier to handle.

A Retirement Readiness Review can help test whether your essential expenses should be covered by Social Security, pensions, annuities, investments, or a combination.

- The 4% rule carries market and longevity risk.

- Annuities may transfer some longevity risk.

- Investment withdrawals may provide more upside and flexibility.

- Annuities may provide more predictable income.

- The best strategy depends on which risks worry you most.

4. Liquidity, Taxes, Inflation, and Legacy Goals Can Change the Answer

The income strategy that looks best at first may not be best after you consider liquidity, taxes, inflation, and legacy goals.

Start with liquidity.

The 4% rule generally keeps more of your money accessible in investment accounts. That can be helpful if you need money for home repairs, healthcare, travel, family support, or emergencies.

Annuities may reduce liquidity, depending on the type of contract. Some allow ]partial withdrawals. Others may lock up principal in exchange for income. Some have surrender charges for a number of years.

Next, consider taxes.

Investment withdrawals are taxed differently depending on the account.

Traditional IRA and 401(k) withdrawals are generally taxable as ordinary income. Roth IRA withdrawals may be tax-free if qualified. Taxable brokerage accounts may create capital gains, dividends, or interest.

Annuity taxation depends on whether the annuity is qualified or non-qualified and how the income is structured.

This matters because retirement is about after-tax income, not just gross income.

A strategy that produces $5,000 per month before taxes may not be as attractive if the after-tax result is much lower.

Next, consider inflation.

The 4% rule is designed to adjust withdrawals for inflation, but whether that works depends on portfolio performance. If inflation rises and markets struggle, inflation-adjusted withdrawals may become harder to sustain.

Annuities may provide predictable income, but some annuity payments may be fixed. If income does not rise over time, inflation can reduce purchasing power.

Finally, consider legacy goals.

With the 4% rule, any money remaining in the portfolio can generally be left to heirs, charities, or other beneficiaries.

With annuities, the legacy outcome depends on the contract. Some annuities may leave little or no remaining value after death. Others may include refund features, death benefits, period-certain payments, or survivor benefits.

Those features matter, but they usually come with trade-offs.

This is why blanket advice fails.

Saying “never buy annuities” ignores situations where predictable income may solve a real problem.

Saying “the 4% rule is all you need” ignores the emotional and financial risk of bad markets, long life, and uncertain income.

Good planning compares the trade-offs.

A Retirement Readiness Review can help compare the after-tax, after-inflation, and survivor impact of each strategy.

- Liquidity may favor investment withdrawals.

- Predictable income may favor annuities.

- Taxes can change the real income result.

- Inflation affects both strategies differently.

- Legacy goals may favor one strategy over another.

5. The Best Strategy May Be a Blend of Both

The biggest mistake is assuming you have to choose one strategy for all your money.

You may not.

For many retirees, the best answer may be a blend.

That means using different parts of your money for different jobs.

For example:

- Social Security covers part of essential expenses.

- A pension covers another part.

- An annuity may fill a predictable income gap.

- Investments provide growth and flexible withdrawals.

- Cash reserves help during market downturns.

- Roth accounts provide tax flexibility.

- Taxable accounts provide liquidity.

- Legacy assets are preserved intentionally.

This kind of structure may reduce stress because every dollar has a job.

Some dollars provide guaranteed or predictable income.

Some dollars stay invested for long-term growth.

Some dollars stay liquid for emergencies.

Some dollars are used for tax planning.

Some dollars may be set aside for heirs.

This can be especially powerful for conservative retirees.

Many people nearing retirement don’t want to chase big returns. They want confidence. They want to know their bills are covered. They want to avoid being forced to sell investments during a bad market.

A blended strategy can help.

But it still needs to be tested.

A bad blend can create problems too. You don’t want to put too much money into an annuity and lose flexibility. You don’t want to keep too much exposed to the market if you can’t emotionally tolerate downturns. You don’t want to ignore taxes. You don’t want to leave the surviving spouse exposed.

The right blend depends on your actual retirement plan.

You should test:

- Investment-only withdrawals.

- Annuity-based income.

- A blended strategy.

- Social Security claiming options.

- Pension survivor options.

- Roth conversion strategies.

- Market downturn scenarios.

- Survivor income scenarios.

- Long-term care or healthcare shocks.

- Different spending levels.

That’s how you decide what wins.

Not based on theory.

Not based on a sales pitch.

Not based on a rule of thumb.

Based on your numbers.

A Retirement Readiness Review can help compare the 4% rule, annuities, and blended income strategies so you can make a decision with more confidence.

- You don’t have to use one strategy for everything.

- Annuities can cover part of the income need.

- Investments can provide flexibility and growth.

- Cash reserves can reduce forced selling.

- The best strategy should be tested against real retirement risks.

Conclusion

So, annuities versus the 4% rule: which income strategy wins?

The honest answer is that it depends.

The 4% rule may win if you value flexibility, growth potential, control, liquidity, and legacy planning. Annuities may win if you value predictable income, lifetime cash flow, and less fear of running out of money.

But for many retirees, the real winner may be a thoughtful blend of both.

The 4% rule is not a guarantee. Annuities are not magic. Both are tools. The question is whether the tool fits the job.

Your retirement income strategy should help you pay your bills, manage taxes, handle bad markets, protect your spouse, fight inflation, preserve flexibility, and give you confidence that your money can support the life you want.

If you’re within a few years of retirement and trying to decide between annuities and the 4% rule, a Retirement Readiness Review can help. We’ll look at your actual numbers, define your income needs, test different strategies, and help you understand the trade-offs before you commit to a plan.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before turning your savings into retirement income.

FAQs

Is the 4% rule better than an annuity?

Not always. The 4% rule may provide more flexibility, growth potential, and legacy value. An annuity may provide more predictable income and help reduce longevity risk. The better strategy depends on your income needs, assets, taxes, risk tolerance, and goals.

Are annuities safer than the 4% rule?

Annuities may provide more predictable income if the guarantees are backed by the issuing insurance company and the contract terms are understood. But they may also reduce liquidity and flexibility. The 4% rule keeps money invested and flexible, but it exposes you to market risk and withdrawal risk.

Can I use both an annuity and the 4% rule?

Yes. Many retirees may benefit from a blended strategy. An annuity can help cover essential expenses, while investment withdrawals can provide growth, flexibility, inflation protection, and legacy potential.