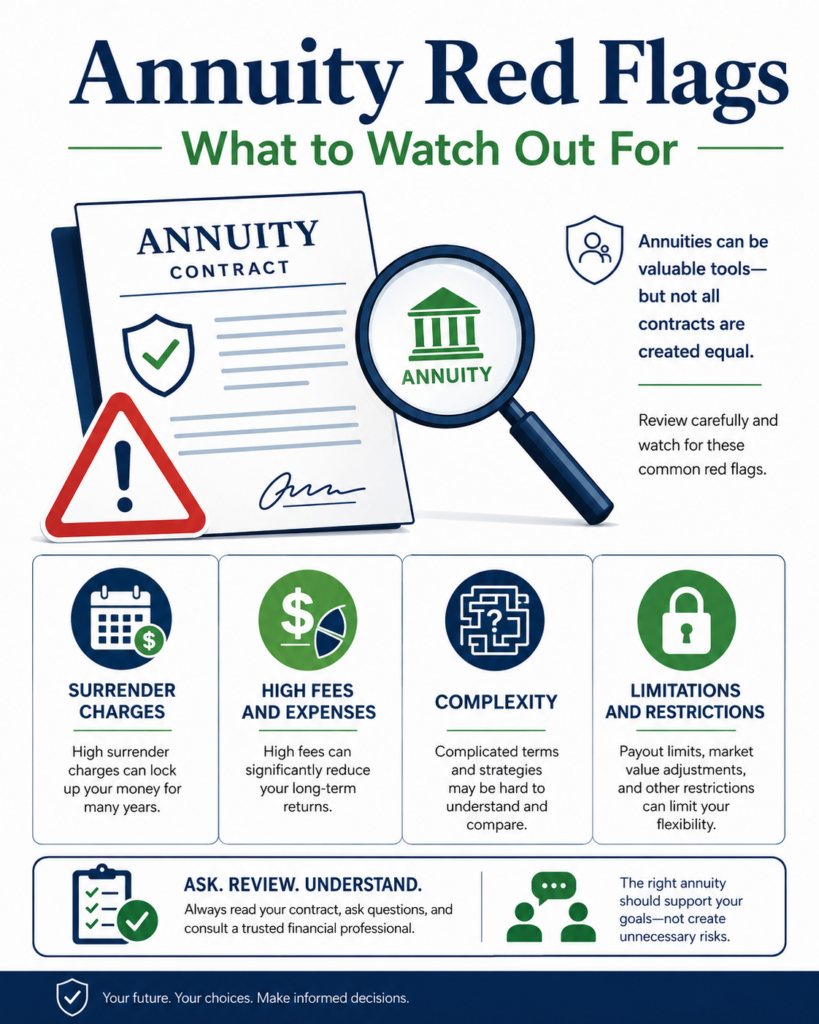

Annuity Red Flags: What to Watch Out For

Annuities can be useful retirement income tools, but they can also be confusing, oversold, and misunderstood.

That’s the problem.

Some annuities can help create predictable income, protect against outliving your money, or reduce pressure on your investment portfolio. But not every annuity is a good fit. And not every annuity recommendation is made with the full retirement plan in mind.

In this article, we’ll walk through five annuity red flags to watch out for before you sign anything. The goal isn’t to say annuities are bad. They’re not. The goal is to help you understand when an annuity may solve a real retirement problem—and when it may create unnecessary complexity, costs, or regret.

Short on time? Here is the Key Point / Summary

Annuities should be evaluated carefully because the wrong contract can limit liquidity, create surrender charges, hide fees, overpromise benefits, or fail to match your real retirement income needs.

Here are the five red flags we’ll cover:

- You don’t understand how the annuity works.

- The surrender period is too long for your needs.

- The fees, caps, spreads, or rider costs are unclear.

- The sales pitch focuses on guarantees without explaining trade-offs.

- The annuity is recommended before your full retirement plan is tested.

Annuities can be complex, and some annuity contracts may have surrender periods that last many years. Surrender charges can reduce the value and return of your investment if you withdraw too much money too soon.

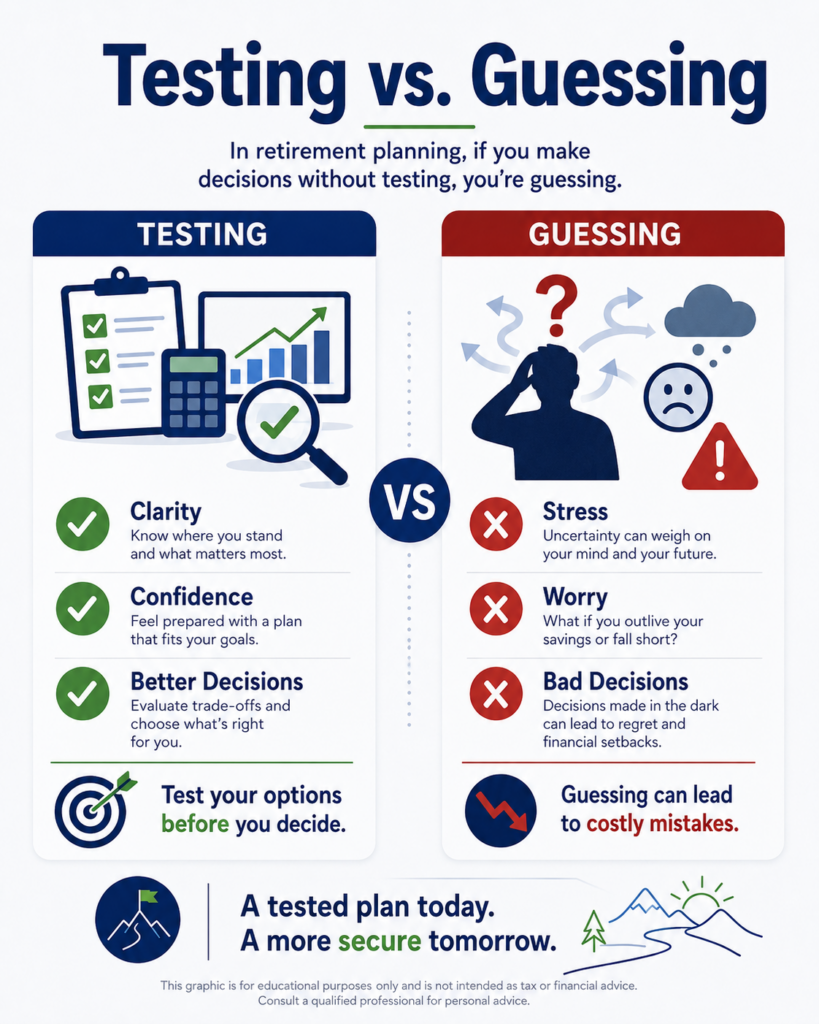

If you’re considering an annuity, the question is not, “Is this product good or bad?” The better question is, “What job is this annuity supposed to do in my retirement plan, and are the trade-offs worth it?”

A Retirement Readiness Review can help you compare annuities against other income strategies before you buy anything, move money, or commit to a contract you may not fully understand.

What Are the Biggest Annuity Red Flags?

The biggest annuity red flag is not the product itself. It’s a recommendation that isn’t clearly connected to your full retirement plan.

An annuity may be appropriate if it helps solve a specific problem, such as:

- Creating lifetime income.

- Covering essential expenses.

- Reducing sequence-of-returns risk.

- Protecting a spouse.

- Providing principal protection.

- Creating more predictable cash flow.

- Reducing emotional stress during market downturns.

But an annuity may be a poor fit if:

- You need liquidity.

- You don’t understand the terms.

- The surrender period is too long.

- Fees are unclear.

- The guarantees are oversold.

- You’re putting too much of your money into one product.

- The recommendation is based on a sales pitch instead of a tested plan.

Annuities are tools. Like any tool, they can be helpful when used for the right job and harmful when used for the wrong one.

1. You Don’t Understand How the Annuity Works

The first annuity red flag is simple: you don’t understand the product.

If you can’t explain the annuity in plain English, you probably shouldn’t buy it yet.

That doesn’t mean you need to become an annuity expert. But you should understand the basic mechanics before putting retirement savings into a contract.

You should be able to answer:

- Is this a fixed annuity, fixed indexed annuity, variable annuity, immediate annuity, or deferred income annuity?

- Is the goal income, growth, protection, tax deferral, or legacy?

- When can I access the money?

- What happens if I need a large withdrawal?

- What fees or charges apply?

- What income is guaranteed?

- What is not guaranteed?

- What happens if I die early?

- What happens if my spouse outlives me?

- What happens if inflation rises?

- What happens if I change my mind?

If the explanation sounds impressive but leaves you confused, slow down.

A good annuity recommendation should be understandable. If the product is so complicated that you have to simply “trust the salesperson,” that’s a problem.

This is especially important with indexed or variable annuities.

Variable annuities can contain investment subaccounts, insurance features, rider charges, mortality and expense charges, administrative fees, surrender charges, and optional benefits. Fixed indexed annuities may also have moving parts, such as caps, spreads, participation rates, crediting methods, surrender periods, income riders, and withdrawal rules.

None of that automatically makes them bad. But it does mean you need to understand what you’re buying.

A simple rule helps: If the product has to be sold with a long explanation but the risks are brushed over quickly, pause.

You should also be careful with phrases like:

- “You get market upside with no downside.”

- “You can’t lose.”

- “It’s just like a bank CD.”

- “You’ll get guaranteed income and full access.”

- “There are no fees.”

- “This is only available for a limited time.”

- “Everyone in retirement should own this.”

Those phrases may leave out important details.

For example, “no market downside” may apply to the contract value under certain terms, but it doesn’t mean there are no surrender charges, opportunity costs, inflation risks, liquidity limits, or rider costs.

A Retirement Readiness Review can help translate the annuity proposal into plain English and compare it against your actual retirement goals.

- Don’t buy an annuity you can’t explain.

- Ask what is guaranteed and what is not.

- Understand the type of annuity being recommended.

- Be cautious when benefits are emphasized but trade-offs are minimized.

- A good recommendation should be clear, not confusing.

2. The Surrender Period Is Too Long for Your Needs

The second annuity red flag is a long surrender period that doesn’t match your need for access to money.

A surrender period is the length of time when you may pay a penalty if you withdraw too much money from the annuity or cancel the contract. Some surrender periods can last six to ten years or even longer.

This matters because retirement is unpredictable.

You may need money for:

- Healthcare expenses.

- Long-term care.

- Home repairs.

- Helping family.

- A new vehicle.

- Moving or downsizing.

- Emergency expenses.

- Travel.

- Tax payments.

- Market downturn protection.

If too much of your money is locked into an annuity, you may not have enough flexibility.

Many annuities allow a certain amount of penalty-free withdrawals each year, such as 10% of the contract value. But that doesn’t mean you have full access without consequences. Withdrawals may still affect income guarantees, riders, taxes, or future benefits.

That’s why the surrender period must be considered before you buy.

A long surrender period may be acceptable if the annuity is being used for a specific long-term purpose, like future lifetime income. But it may be a problem if you’re putting money into the annuity that you may need in the next few years.

A useful question is:

Would I still be comfortable if I couldn’t freely access this money for the next 7 to 10 years?

If the answer is no, be careful.

Another red flag is when someone recommends putting a large percentage of your savings into one annuity.

Even if the annuity is appropriate, concentration can create problems. You may want some money in predictable income, some in investments, some in cash, some in Roth accounts, and some in flexible taxable accounts.

Different dollars should have different jobs.

An annuity may be a good place for some dollars, but not necessarily all dollars.

A Retirement Readiness Review can help determine how much liquidity you need before deciding whether an annuity fits.

- Surrender periods can limit access to your money.

- Surrender charges may reduce your return if you withdraw early.

- Penalty-free withdrawals may still have restrictions.

- Don’t put emergency money into a long surrender contract.

- The annuity amount should match your liquidity needs.

3. The Fees, Caps, Spreads, or Rider Costs Are Unclear

The third annuity red flag is unclear costs.

Some annuity costs are obvious. Others are harder to see.

That’s why asking “What are the fees?” is not enough. You also need to ask how the insurance company makes money, how your return is credited, and what features reduce your income or growth potential.

Depending on the annuity type, costs and trade-offs may include:

- Surrender charges.

- Mortality and expense charges.

- Administrative fees.

- Investment subaccount expenses.

- Income rider fees.

- Death benefit rider fees.

- Long-term care rider costs.

- Caps on growth.

- Participation rates.

- Spreads.

- Market value adjustments.

- Lower starting income for added guarantees.

- Lower crediting rates for added features.

With fixed indexed annuities, you may hear “no fee” or “zero fee.” That may be technically true for the base contract, but the trade-offs may show up in caps, spreads, participation rates, or restrictions on how interest is credited.

For example, if an indexed annuity has a cap, you may only receive gains up to a certain limit. If it has a spread, the insurance company may subtract a percentage before crediting interest. If it has a participation rate, you may receive only a portion of the index gain.

Again, that does not make the annuity bad.

It means the cost may not always look like a line-item fee.

You need to understand the economics.

A good advisor should be willing to explain:

- What fees are charged directly?

- What costs are built into the product?

- How does the insurance company make money?

- What limits my upside?

- What happens if I add riders?

- What happens if I remove riders?

- What are the surrender charges?

- What is the worst-case outcome?

- What are the alternatives?

Be especially careful if someone says, “There are no fees,” and then quickly moves on.

A better explanation would be: “Here are the direct fees, here are the indirect trade-offs, here’s how the product is priced, and here’s what you’re giving up in exchange for the benefits.”

That’s the kind of transparency you want.

A Retirement Readiness Review can help compare the real cost of the annuity against other strategies, such as investment withdrawals, bond ladders, CDs, Treasury ladders, or delaying Social Security.

- Some annuity costs are obvious; others are built into the design.

- Variable annuities may include several layers of fees.

- Indexed annuities may use caps, spreads, and participation rates.

- Riders can add benefits but may also add costs.

- “No fee” does not always mean “no trade-off.”

4. The Sales Pitch Focuses on Guarantees Without Explaining Trade-Offs

The fourth annuity red flag is a sales pitch that focuses heavily on guarantees but barely discusses trade-offs.

Guarantees can be valuable.

For many retirees, guaranteed lifetime income can provide peace of mind. It may help cover essential expenses, reduce fear of running out of money, and make it easier to stay calm during market downturns.

But guarantees are not magic.

They are contractual promises backed by the claims-paying ability of the issuing insurance company. They also come with terms, conditions, limits, and trade-offs.

A guarantee may involve giving up:

- Liquidity.

- Upside potential.

- Legacy value.

- Flexibility.

- Inflation protection.

- Control over investments.

- Access to principal.

- Higher income in the early years.

- Simplicity.

A red flag is when only the good parts are emphasized.

For example:

- “Guaranteed income for life” sounds good.

- But what happens if you need a lump sum?

- What happens if inflation rises?

- What happens if you die early?

- What happens to your spouse?

- What happens to your heirs?

- What happens if the rider fee increases?

- What happens if you withdraw more than allowed?

Those questions matter.

Another red flag is when hypothetical illustrations are presented like guaranteed outcomes.

Annuity illustrations can be helpful, but you need to separate guaranteed values from non-guaranteed projections. If the illustration assumes strong crediting, market performance, or future rates, ask what happens under less favorable assumptions.

You should also be cautious with bonus features.

Some annuities offer premium bonuses or income bonuses. These can sound attractive, but bonuses may come with longer surrender periods, lower caps, higher charges, or other trade-offs.

The point is not that bonuses are always bad. The point is that you need to ask what you’re giving up to receive the bonus.

A good annuity conversation should include both sides:

- What problem does this solve?

- What risks does it reduce?

- What risks remain?

- What does it cost?

- What flexibility do I lose?

- What happens if I change my mind?

- What alternatives should I compare?

If the salesperson cannot clearly explain the downside, that’s a major warning sign.

A Retirement Readiness Review can help identify whether the guarantee is actually valuable in your plan or simply sounds attractive in a sales presentation.

- Guarantees can be useful, but they have conditions.

- A guarantee may reduce flexibility or liquidity.

- Bonus features may have hidden trade-offs.

- Separate guaranteed values from hypothetical projections.

- A fair recommendation explains both benefits and drawbacks.

5. The Annuity Is Recommended Before Your Full Retirement Plan Is Tested

The fifth and most important red flag is when an annuity is recommended before your full retirement plan is tested.

This is where I’d be most careful.

An annuity should not be the starting point. Your retirement plan should be the starting point.

Before buying an annuity, you should know:

- How much income you need.

- How much Social Security will provide.

- Whether you have a pension.

- What your essential expenses are.

- What your lifestyle expenses are.

- How much income your portfolio needs to generate.

- How much market risk you can tolerate.

- How much liquidity you need.

- What your tax situation looks like.

- What happens if one spouse dies.

- What happens if healthcare costs rise.

- What happens if you need long-term care.

- What you want to leave to heirs.

Only after that should you decide whether an annuity fits.

A red flag is when the conversation starts with the product instead of the plan.

For example:

- “I have the perfect annuity for you.”

- “This product solves retirement income.”

- “This is what all retirees should do.”

- “You need to move this money now.”

- “This offer won’t last.”

- “We don’t need to look at your full plan.”

That’s backwards.

A good process should start with your numbers.

First, create a baseline. What happens if you keep doing what you’re doing? Then test options. What happens if you delay Social Security? What happens if you use investment withdrawals? What happens if you use a Treasury ladder? What happens if you add an annuity? What happens if markets are bad? What happens if one spouse dies?

That’s how you determine whether an annuity is solving a real problem.

Sometimes the answer will be yes.

An annuity may improve the plan by creating lifetime income, covering essential expenses, or reducing sequence-of-returns risk.

Sometimes the answer will be no.

The annuity may reduce liquidity, create unnecessary complexity, or solve a problem you don’t actually have.

And sometimes the answer is a blend.

You may use an annuity for part of the income need while keeping the rest of the money invested for growth, flexibility, inflation protection, and legacy goals.

That’s why testing matters.

The goal is not to be pro-annuity or anti-annuity.

The goal is to be pro-plan.

A Retirement Readiness Review can help you test annuities against other strategies before you commit.

- The retirement plan should come before the product.

- Annuities should solve a specific problem.

- Compare annuities against other income strategies.

- Test survivor, tax, liquidity, and market scenarios.

- The best decision is based on your numbers, not a sales pitch.

Conclusion

Annuities can be helpful retirement tools, but they need to be handled carefully.

The red flags are not always obvious. Sometimes the danger is not the annuity itself, but the way it’s explained, sold, or used.

Be careful if you don’t understand the product, if the surrender period is too long, if fees and trade-offs are unclear, if guarantees are emphasized without limitations, or if the annuity is recommended before your full retirement plan is tested.

A good annuity should have a clear job.

It should help solve a specific retirement problem, such as income stability, longevity protection, or covering essential expenses. It should also fit your liquidity needs, tax plan, spouse protection, and long-term goals.

If you’re considering an annuity, don’t make the decision based on fear, pressure, or a polished illustration.

Test it.

A Retirement Readiness Review can help compare annuities, investment withdrawals, Social Security timing, taxes, survivor income, and market risk so you can see whether an annuity improves your plan or creates unnecessary trade-offs.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before making a decision that could affect your retirement for years.

FAQs

Are annuities bad for retirees?

No. Annuities are not automatically bad. Some can provide useful income guarantees, principal protection, or lifetime income. The issue is whether the annuity fits your retirement plan, whether you understand the trade-offs, and whether the product solves a real problem.

What is the biggest annuity red flag?

The biggest red flag is being sold an annuity before your full retirement plan has been tested. A product should not come before the plan. You should understand income needs, taxes, liquidity, spouse protection, and alternatives before buying.

What should I ask before buying an annuity?

Ask how the annuity works, what fees apply, how long the surrender period lasts, what is guaranteed, what is not guaranteed, how withdrawals work, what happens if you die, what happens if your spouse outlives you, and how the annuity compares to other income strategies.