Roth Conversions in Retirement: Smart Move or Tax Trap?

Roth conversions can be one of the most useful retirement tax planning strategies available. They can also be one of the easiest ways to accidentally create a large tax bill, higher Medicare premiums, and unnecessary stress.

That’s why Roth conversions are not automatically good or bad. They’re a tool. Used at the right time, they may help reduce future required minimum distributions, create more tax flexibility, help a surviving spouse, and leave more attractive assets to heirs. Used carelessly, they can push you into a higher tax bracket, trigger IRMAA, increase taxable income, and create a tax bill you weren’t prepared to pay.

In this article, we’ll walk through five important things to understand before doing Roth conversions in retirement so you can decide whether they may be a smart move or a tax trap.

Short on time? Here is a Key Point / Summary

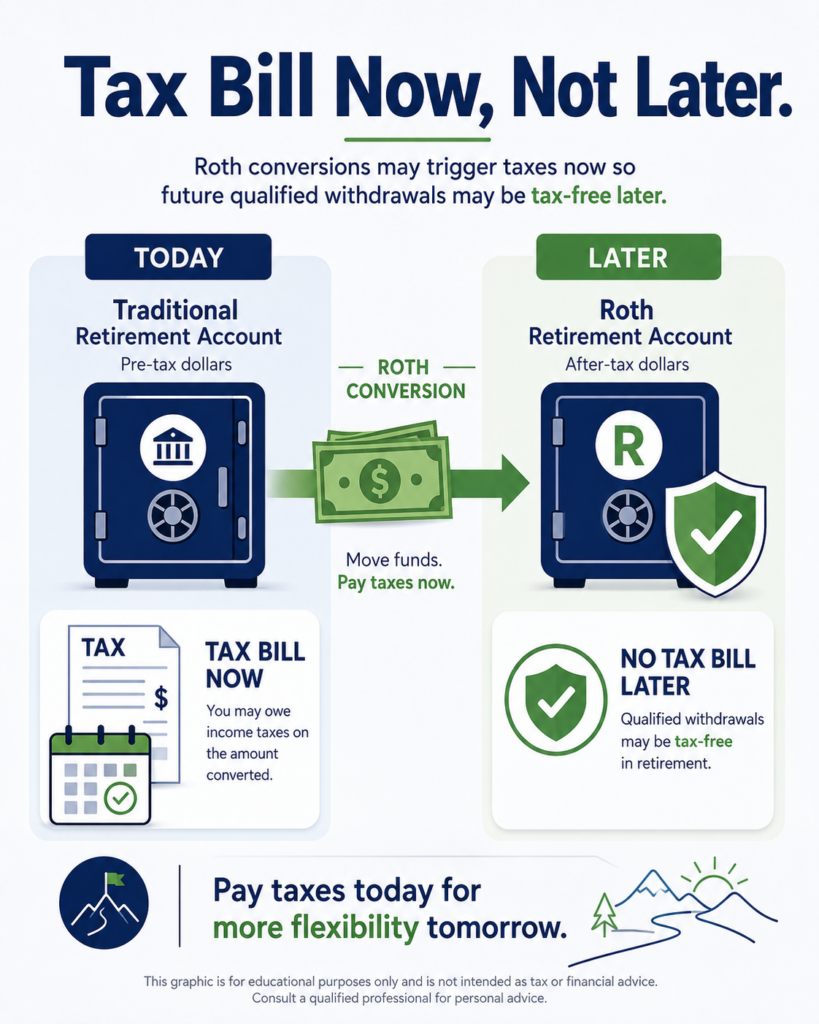

A Roth conversion means moving money from a traditional pre-tax retirement account into a Roth account. The converted amount is generally taxable in the year of conversion, but future qualified Roth withdrawals may be tax-free.

Here are the five key things we’ll cover:

- Roth conversions can create future tax flexibility.

- The tax bill happens now, not later.

- Roth conversions can affect Medicare IRMAA and Social Security taxation.

- The best conversion window may be before RMDs begin.

- Roth conversions should be tested, not guessed.

Converting a traditional IRA to a Roth IRA generally results in taxation of any untaxed amounts in the traditional IRA. People may be able to convert amounts from a traditional IRA into a Roth IRA regardless of adjusted gross income.

Required minimum distributions matter too. Owners of traditional IRA, SEP IRA, and SIMPLE IRA accounts generally must begin RMDs once they reach age 73, even if retired.

If you’re within a few years of retirement, a Retirement Readiness Review can help you test whether Roth conversions improve your plan or simply create unnecessary taxes.

Are Roth Conversions in Retirement a Smart Move or a Tax Trap?

Roth conversions can be smart when they help you pay taxes at a lower rate today to reduce future taxes, create flexibility, and improve long-term retirement income planning.

They can become a tax trap when you convert too much, convert at the wrong time, ignore Medicare premiums, forget about Social Security taxation, or pay the tax from the wrong source.

The real question is not, “Should retirees do Roth conversions?”

The better question is:

How much should you convert, in which years, and what problem is the conversion supposed to solve?

That question changes everything.

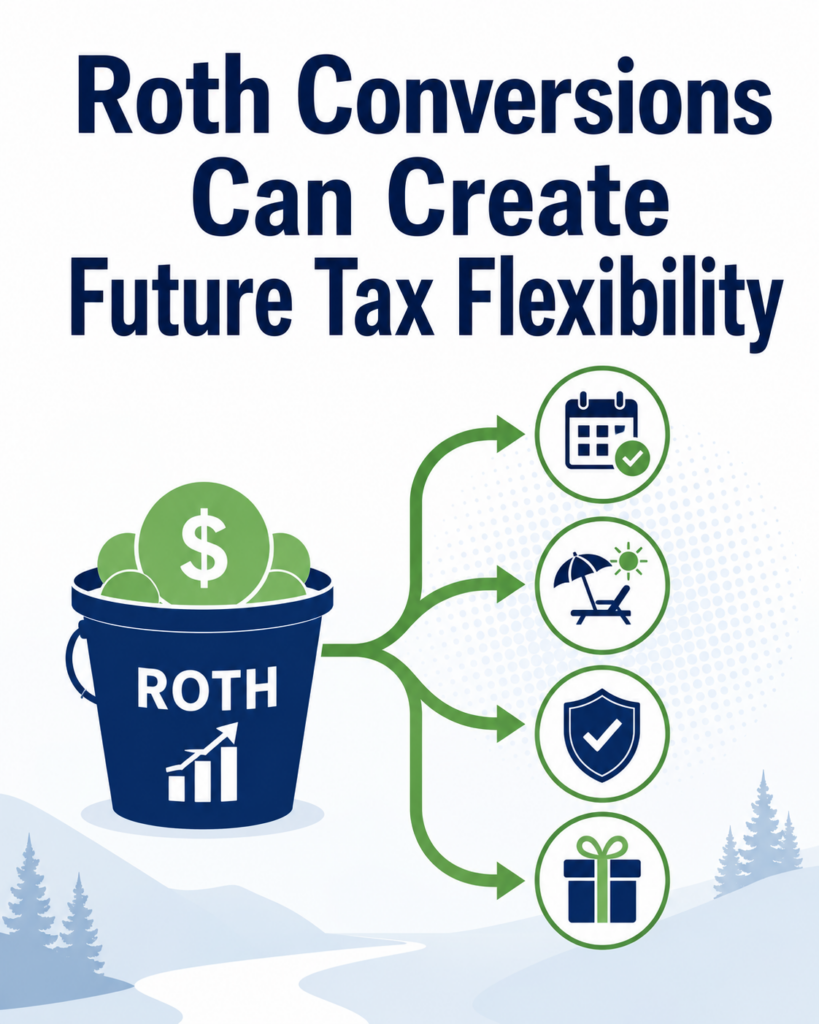

1. Roth Conversions Can Create Future Tax Flexibility

The first reason Roth conversions may be smart is future tax flexibility.

Many retirees enter retirement with most of their savings in traditional IRAs or 401(k)s. That can be a good thing while working because pre-tax contributions may have reduced taxable income during high-earning years.

But in retirement, those accounts create taxable income when money comes out.

Traditional IRA and 401(k) withdrawals are generally taxed as ordinary income. That means if most of your retirement income has to come from tax-deferred accounts, you may have less control over your future tax bill.

A Roth conversion can help change that.

When you convert money from a traditional IRA to a Roth IRA, you pay tax on the converted amount now. In exchange, the money moves into a Roth account, where future qualified withdrawals may be tax-free.

That can be valuable later in retirement.

Roth money may give you flexibility to:

- Fund large expenses without increasing taxable income the same way.

- Manage future tax brackets.

- Reduce pressure from future RMDs.

- Help control taxable income after Social Security begins.

- Create tax flexibility for a surviving spouse.

- Leave potentially more tax-favorable assets to heirs.

For example, suppose you need $40,000 for a car, home repair, or major trip later in retirement. If all your money is in a traditional IRA, that withdrawal may increase taxable income. If you have Roth money available, you may have more flexibility.

That doesn’t mean you should always use Roth money first. But having Roth money gives you options.

Options are valuable in retirement.

Retirement is unpredictable. Tax laws can change. Your spouse may pass away. Medical expenses may rise. Required minimum distributions may become larger than expected. You may need to help family. You may want to make a large purchase.

Roth conversions may help create a more flexible tax structure before those events happen.

But flexibility has a cost.

You don’t get Roth benefits for free. The conversion creates taxable income in the year you do it. So the question is whether paying tax today is worth the future flexibility.

A Retirement Readiness Review can help test whether Roth conversions improve your long-term plan or simply move taxes forward unnecessarily.

- Roth conversions can create future tax-free income if rules are met.

- Roth accounts may provide flexibility for large expenses.

- Roth money may help manage future tax brackets.

- Roth conversions may help reduce future RMD pressure.

- The benefit must be weighed against today’s tax bill.

2. The Tax Bill Happens Now, Not Later

The second thing to understand is simple: Roth conversions can create a tax bill now.

This is where Roth conversions can become a tax trap.

If you convert $50,000 from a traditional IRA to a Roth IRA, that $50,000 is generally added to your taxable income for the year, assuming it was pre-tax money. That can push you into a higher tax bracket, increase the amount of tax you owe, and possibly affect other parts of your financial life.

A Roth conversion generally results in taxation of any untaxed amounts in the traditional IRA.

That means you need to plan for the tax bill before converting.

A common mistake is converting a large amount because Roth accounts sound attractive, then realizing later that the tax bill is much larger than expected.

Another mistake is using IRA money to pay the conversion tax.

If you convert $100,000 and withhold taxes from the IRA, less money gets into the Roth account. You may also create additional taxable income if more money is withdrawn to cover taxes. In many cases, conversions are more attractive when you can pay the tax from non-retirement assets, but this depends on your situation.

You also need to think about your current tax bracket versus your future tax bracket.

A Roth conversion may make sense if you believe you’re paying tax at a lower rate today than you’re likely to pay later. But if you convert too much and push yourself into a higher bracket, the benefit may shrink or disappear.

For example, converting enough to “fill up” a lower tax bracket may be reasonable in some cases. But converting so much that you jump into a much higher bracket may turn a smart strategy into a tax mistake.

This is why the amount matters.

Roth conversion planning is rarely all-or-nothing. It’s often about finding the right annual conversion amount.

You may convert:

- A small amount each year.

- Enough to fill a target tax bracket.

- More in unusually low-income years.

- Less or nothing in high-income years.

- More before required minimum distributions begin.

- Less once Social Security, pensions, or RMDs increase income.

The key is to avoid guessing.

A Retirement Readiness Review can help compare conversion amounts so you can see the tax impact before making the move.

- Roth conversions create taxable income in the year of conversion.

- Converting too much can push you into a higher tax bracket.

- You should know how the tax bill will be paid.

- Paying tax from non-retirement assets may improve the outcome in some cases.

- The conversion amount matters as much as the decision to convert.

3. Roth Conversions Can Affect Medicare IRMAA and Social Security Taxation

The third thing to understand is that Roth conversions can affect more than your income tax bracket.

This is where many retirees get surprised.

A Roth conversion can increase your modified adjusted gross income. That may affect Medicare IRMAA, Social Security taxation, Marketplace health insurance subsidies before Medicare, and other income-based calculations.

IRMAA stands for Income-Related Monthly Adjustment Amount. It is an extra Medicare surcharge that can apply to higher-income beneficiaries. Medicare IRMAA uses modified adjusted gross income, generally adjusted gross income plus tax-exempt interest.

That matters because Roth conversions increase adjusted gross income in the year of conversion.

So, a Roth conversion done at age 63 may affect Medicare premiums at age 65 because IRMAA often uses a two-year lookback. A conversion done after Medicare begins may also affect future Medicare premiums.

This doesn’t mean Roth conversions are bad.

Sometimes it may be worth paying IRMAA temporarily if the conversion creates larger long-term benefits. But you want that to be a planned decision, not a surprise.

Roth conversions can also affect Social Security taxation.

Social Security benefits may become taxable depending on your combined income. A Roth conversion increases taxable income, which may cause more of your Social Security benefit to be taxable in that year.

Again, this does not automatically mean the conversion is wrong. It just means the full impact should be reviewed.

A retiree might say, “I’m in the 12% tax bracket, so I’ll convert more.”

But the real cost may be higher if the conversion also:

- Makes more Social Security taxable.

- Triggers IRMAA.

- Reduces health insurance subsidies before Medicare.

- Increases state income taxes.

- Pushes capital gains into a higher tax range.

- Affects the surviving spouse’s future tax picture.

That’s why Roth conversion planning must be coordinated.

You should ask:

- Will this conversion increase Medicare premiums?

- Will it make more Social Security taxable?

- Will it affect health insurance subsidies?

- Will it push me into a higher tax bracket?

- Will it affect both spouses?

- Will the long-term benefit justify the short-term cost?

Roth conversions can still be a great strategy. But they need to be measured against all costs, not just federal income tax.

A Retirement Readiness Review can help test Roth conversions alongside IRMAA, Social Security taxation, and retirement income needs.

- Roth conversions increase taxable income.

- Higher income may affect Medicare IRMAA.

- Social Security taxation may also be affected.

- Pre-Medicare health insurance subsidies may be affected.

- The full cost should be tested before converting.

4. The Best Conversion Window May Be Before RMDs Begin

The fourth thing to understand is timing.

For many retirees, the best Roth conversion window may be after retirement but before required minimum distributions begin.

Why?

Because these years may be lower-income years.

You may have stopped working, but Social Security may not have started yet. Pension income may not have started yet. Required minimum distributions may not have started yet. That can create a temporary planning window.

Owners of traditional IRA, SEP IRA, and SIMPLE IRA accounts generally must begin taking RMDs at age 73.

Once RMDs begin, you may have less control over your taxable income because the IRS requires certain minimum withdrawals from tax-deferred accounts.

That’s why the years before RMDs can be important.

For example, suppose you retire at 62 and delay Social Security until 70. You may have several years where taxable income is lower than it was during your working years and lower than it may be after Social Security and RMDs begin.

Those years may be a good time to test Roth conversions.

But again, “may” is the key word.

The right strategy depends on:

- Your retirement date

- Your Social Security claiming age

- Your pension start date

- Your IRA balance

- Your tax bracket

- Your Medicare age

- Your spouse’s income

- Your investment withdrawals

- Your cash reserves

- Your estate goals

This is also where survivor planning matters.

When one spouse dies, the surviving spouse may eventually file as single. That can create a higher tax burden because the surviving spouse may have less favorable tax brackets but still have significant income.

Roth conversions during married years may help reduce future tax pressure on the surviving spouse.

This can be especially important when most retirement savings are in traditional IRAs or 401(k)s.

If the couple does nothing, future RMDs may be large. If one spouse dies, the survivor may have a large IRA, one Social Security check, possible pension survivor income, and single tax brackets.

That can create a tax problem.

Roth conversions may help reduce that risk if done carefully.

But converting too aggressively can create a different problem. You may pay too much tax too soon, reduce flexibility, or trigger Medicare surcharges.

That’s why timing and sizing matter.

A Retirement Readiness Review can help identify whether your pre-RMD years are a good Roth conversion window.

- The years after retirement and before RMDs may create planning opportunities.

- RMDs generally begin at age 73 for many tax-deferred retirement accounts.

- Roth conversions before RMDs may reduce future taxable income.

- Survivor tax planning can make conversions more attractive.

- Timing matters because income changes throughout retirement.

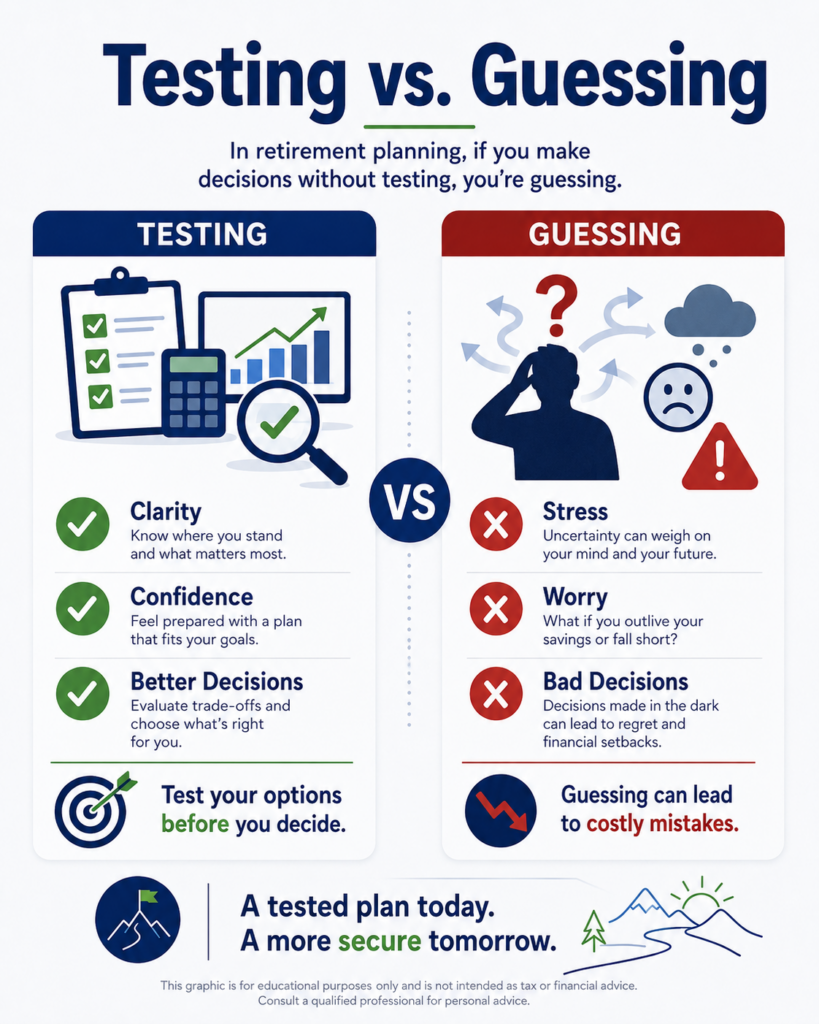

5. Roth Conversions Should Be Tested, Not Guessed

The fifth and most important point is this: Roth conversions should be tested before they’re done.

Too many people approach Roth conversions with rules of thumb.

They hear:

- “Always convert before RMDs.”

- “Never pay taxes before you have to.”

- “Convert everything before tax rates go up.”

- “Don’t convert because it triggers IRMAA.”

- “Roth money is always better.”

Those statements are too simplistic.

Roth conversions are highly personal. The right answer depends on your income, assets, taxes, retirement age, spouse, Medicare situation, Social Security timing, estate goals, and cash flow.

The best way to evaluate Roth conversions is to compare scenarios.

For example:

Scenario 1: No Roth conversions

You leave the traditional IRA alone, take withdrawals as needed, and begin RMDs later.

Scenario 2: Moderate Roth conversions

You convert enough each year to fill a target tax bracket without creating unnecessary spikes.

Scenario 3: Aggressive Roth conversions

You convert larger amounts earlier, accepting higher taxes now for potentially lower future taxes.

Then you compare the results.

You want to look at:

- Lifetime taxes

- After-tax retirement income

- Future RMDs

- Medicare premiums

- Social Security taxation

- Portfolio longevity

- Surviving spouse impact

- Legacy value

- Cash flow

- Flexibility

The answer may surprise you.

Sometimes moderate conversions can improve the plan. Sometimes aggressive conversions are too costly. Sometimes no conversion is perfectly reasonable. Sometimes conversions make sense for one spouse’s protection more than for immediate tax savings.

The key is clarity.

You should know what problem the conversion is solving.

Possible goals include:

- Reducing future RMDs.

- Creating tax-free income later.

- Protecting the surviving spouse.

- Managing future tax brackets.

- Leaving better assets to heirs.

- Reducing estate complexity.

- Creating flexibility for large expenses.

- Taking advantage of low-income years.

If you can’t identify the purpose, you probably shouldn’t convert yet.

Roth conversions are not about chasing a trendy strategy. They are about improving your retirement plan.

A Retirement Readiness Review can help test different conversion strategies before you create a tax bill.

- Avoid one-size-fits-all Roth conversion advice.

- Compare no conversion, moderate conversion, and aggressive conversion scenarios.

- Measure after-tax results, not just account balances.

- Consider Medicare, Social Security, RMDs, and survivor planning.

- Convert only when the strategy solves a real problem.

Conclusion

Roth conversions in retirement can be a smart move or a tax trap.

They may be smart when they help reduce future RMDs, create tax flexibility, protect a surviving spouse, and improve long-term after-tax retirement income. They may become a tax trap when they’re done too aggressively, without understanding the tax bill, Medicare IRMAA, Social Security taxation, or cash flow consequences.

The strategy is not automatically good or bad.

The real question is whether Roth conversions improve your specific retirement plan.

That means looking at your retirement income, current tax bracket, future tax bracket, RMDs, Social Security timing, Medicare premiums, spouse protection, and estate goals.

If you’re within a few years of retirement and wondering whether Roth conversions make sense, a Retirement Readiness Review can help. We’ll test different strategies, compare the trade-offs, and help you understand whether converting is likely to help or hurt.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before creating a tax bill you can’t undo.

FAQs

Are Roth conversions taxable?

Yes. A Roth conversion generally creates taxable income in the year of conversion to the extent the converted money has not already been taxed. A conversion to a Roth IRA generally results in taxation of any untaxed amounts in the traditional IRA.

Can Roth conversions increase Medicare premiums?

Yes, they can. Roth conversions increase adjusted gross income, which may affect Medicare IRMAA. Medicare IRMAA generally uses modified adjusted gross income, which includes adjusted gross income plus tax-exempt interest.

When is the best time to do Roth conversions?

For many retirees, the best window may be after retirement but before Social Security and required minimum distributions begin. However, the best timing depends on your income, tax bracket, Medicare status, spouse, cash flow, and long-term goals.