What Should You Do With Your 401(k) After You Retire?

Retiring does not automatically mean you have to move your 401(k). But it does mean you need to make a thoughtful decision about what role that account will play in your retirement income plan.

For many people, the 401(k) is one of their largest retirement assets. It may be the account they spent decades building. But once the paycheck stops, that same account may need to provide income, manage taxes, handle market risk, prepare for required minimum distributions, and eventually pass to a surviving spouse or heirs.

In this article, we’ll walk through five important things to consider before deciding what to do with your 401(k) after retirement.

Short on time? Here is the Key Point / Summary

After you retire, you generally have several choices for your 401(k). You may be able to leave it in your old employer’s plan, roll it to an IRA, roll it to a new employer plan if you keep working, take withdrawals, convert some money to Roth, or use it as part of a larger retirement income strategy.

Here are the five key things we’ll cover:

- You may not need to move your 401(k) immediately.

- Rolling your 401(k) to an IRA may provide more control and flexibility.

- Your withdrawal strategy matters more after retirement.

- Taxes, RMDs, and Roth conversions should be considered before moving money.

- Your 401(k) decision should be tested inside your full retirement plan.

If a plan pays an eligible rollover distribution directly to you, you generally have 60 days to roll it over to another eligible retirement plan or IRA. Required minimum distributions generally apply to many retirement accounts starting with the year the account owner reaches age 73.

If you’re within a few years of retirement, a Retirement Readiness Review can help you decide whether to keep your 401(k), roll it over, use it for income, convert some to Roth, or coordinate it with Social Security, taxes, and investments.

What Should You Do With Your 401(k) After You Retire?

The best thing to do with your 401(k) after retirement depends on your income needs, tax situation, investment options, fees, retirement age, spouse, estate goals, and whether your employer plan has features worth keeping.

The mistake is assuming there is one automatic answer.

Some retirees should leave their 401(k) where it is, at least temporarily. Some should roll it to an IRA for more flexibility. Some should use part of it for income. Some should coordinate withdrawals with Roth conversions. Some should be careful not to roll money too quickly because they may lose certain plan benefits.

The right question is not, “Should I roll over my 401(k)?”

The better question is:

What job does this 401(k) need to do in my retirement plan?

1. You May Not Need to Move Your 401(k) Immediately

The first thing to understand is that retirement does not automatically require you to move your 401(k).

In many cases, you may be able to leave the money in your former employer’s plan. That can be a reasonable choice if the plan has strong investment options, low costs, good service, and useful withdrawal features.

This can be especially helpful if you are newly retired and still trying to get your income plan organized.

There is nothing wrong with slowing down and making a deliberate decision.

Leaving the money in the 401(k) may be attractive if:

- The plan has low-cost investment options.

- You like the investment lineup.

- You want to avoid making a rushed decision.

- The plan has good institutional pricing.

- You want to keep certain creditor protections.

- You are retiring before age 59½ and may need access under certain rules.

- You want to avoid accidental rollover mistakes.

That last point matters.

Rolling over a 401(k) can be simple when done correctly, but mistakes can be costly. If a plan pays an eligible rollover distribution directly to you, you generally have 60 days to roll it over to another eligible plan or IRA. If you miss that window, the distribution may become taxable, and depending on your age and situation, penalties may apply.

That’s why direct rollovers are often preferred. With a direct rollover, the money goes from the 401(k) plan directly to the receiving IRA or retirement plan, instead of passing through your hands.

But leaving money in the 401(k) also has possible downsides.

Your old employer plan may have limited investment options, limited withdrawal flexibility, higher fees, poor service, or less control than an IRA. Some plans make it difficult to set up customized monthly withdrawals. Others may not allow partial withdrawals in the way you want.

You should review:

- Investment choices

- Fees and expenses

- Withdrawal rules

- Roth 401(k) options

- Beneficiary rules

- Required minimum distribution procedures

- Online access and service quality

- Whether the plan allows flexible income withdrawals

A 401(k) can be a great retirement asset, but you need to know whether the plan still fits your life after work.

A Retirement Readiness Review can help compare keeping your 401(k) versus rolling it to an IRA.

- You may not need to move your 401(k) right away.

- Some employer plans have strong investment options and low costs.

- Direct rollovers can help avoid 60-day rollover mistakes.

- Old 401(k) plans may have limited withdrawal flexibility.

- Review fees, investments, service, and income options before deciding.

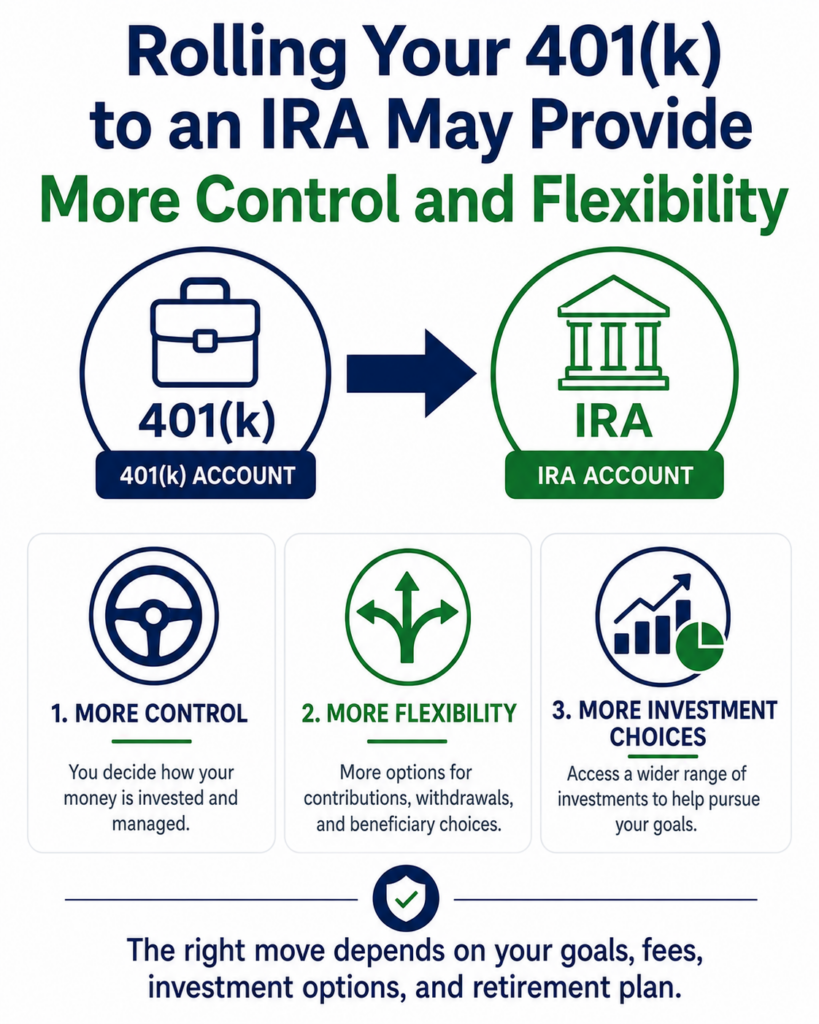

2. Rolling Your 401(k) to an IRA May Provide More Control and Flexibility

The second option is rolling your 401(k) into an IRA.

This is one of the most common retirement moves because an IRA may provide more flexibility than an employer plan.

An IRA may offer:

- More investment choices

- More control over withdrawals

- Easier account consolidation

- More flexible beneficiary planning

- Roth conversion options

- Easier coordination with an advisor

- More customized income planning

For retirees with multiple old 401(k)s, consolidating accounts into an IRA may also simplify life. Instead of tracking several plans, websites, logins, investment menus, and statements, you may have one coordinated account.

That can make retirement income planning easier.

But rolling to an IRA is not automatically better.

A rollover can have downsides if the IRA has higher fees, poor investment choices, unnecessary products, or reduced protections compared with your 401(k). Some 401(k) plans have institutional share classes or low-cost funds that may be hard to match elsewhere.

You should also be careful about sales pressure.

Some people are encouraged to roll over a 401(k) because someone wants to manage the account or sell a product. That does not mean the rollover is bad, but the recommendation should be based on your plan, not someone else’s compensation.

Before rolling over your 401(k), ask:

- Why am I moving this money?

- Will the IRA cost more or less than the 401(k)?

- Will I get better investment options?

- Will I get better withdrawal flexibility?

- Will the rollover affect my access to money before age 59½?

- Will I lose any special plan features?

- How will this affect Roth conversions?

- How will this affect required minimum distributions?

- Is this being recommended for my benefit or because someone wants the account?

That last question is blunt, but important.

A rollover should improve your retirement plan.

It should not be done just because it is common.

A Retirement Readiness Review can help compare the pros and cons of rolling your 401(k) to an IRA before you make the move.

- IRAs may provide more investment flexibility.

- IRAs may make withdrawals and tax planning easier.

- Consolidation can simplify retirement income planning.

- A rollover may not be best if your 401(k) has better costs or features.

- The rollover should solve a real planning problem.

3. Your Withdrawal Strategy Matters More After Retirement

The third thing to understand is that once you retire, your 401(k) is no longer just a savings account. It may become part of your paycheck.

That is a major mindset shift.

During your working years, the goal was accumulation. You contributed money, invested it, and tried to grow the account.

In retirement, the goal becomes distribution. You need to decide how much to withdraw, when to withdraw, which account to use, and how to reduce the risk of running out of money.

This is where many retirees struggle.

They know they have money saved, but they do not know how to turn it into reliable monthly income.

A good 401(k) withdrawal plan should answer:

- How much income do I need each month?

- How much will Social Security provide?

- Do I have a pension or annuity?

- How much must come from investments?

- Should withdrawals come from the 401(k), IRA, Roth, taxable account, or cash?

- What happens if the market drops?

- How much cash should I keep?

- How will taxes be withheld?

- How often should withdrawals be reviewed?

The danger is pulling money randomly.

For example, you may take withdrawals from your 401(k) simply because it is the biggest account. But that may increase taxable income. It may affect Social Security taxation. It may affect Medicare premiums. It may also create unnecessary pressure on investments during a down market.

That does not mean 401(k) withdrawals are bad.

It means they should be coordinated.

For example, some retirees may use taxable savings first to manage taxes. Others may take traditional retirement account withdrawals earlier to reduce future required minimum distributions. Some may preserve Roth accounts for later flexibility. Others may use Roth money strategically for large expenses.

The right answer depends on the plan.

You should also think about sequence-of-returns risk.

If your 401(k) remains invested in the market and you begin taking withdrawals during a major downturn, your portfolio may have a harder time recovering. That is why cash reserves, conservative income buckets, spending flexibility, or guaranteed income sources may matter.

A Retirement Readiness Review can help design a withdrawal strategy so your 401(k) becomes part of a coordinated retirement paycheck.

- Your 401(k) may need to provide income after retirement.

- Withdrawals should not be random.

- Taxes and market risk should be considered.

- A cash reserve may reduce pressure during downturns.

- Your withdrawal plan should coordinate all accounts.

4. Taxes, RMDs, and Roth Conversions Should Be Considered Before Moving Money

The fourth thing to understand is that your 401(k) decision can affect taxes.

This is one of the biggest reasons to plan before moving money.

Traditional 401(k) withdrawals are generally taxable as ordinary income. That means the money you take out can affect your tax bracket, Social Security taxation, Medicare premiums, and future required minimum distributions.

RMDs are especially important.

Required minimum distributions are minimum amounts that retirement account owners generally must withdraw each year starting with the year they reach age 73.

That means if you have a large traditional 401(k) or IRA, you may eventually be required to take withdrawals even if you do not need the money.

This can create tax pressure later in retirement.

For example, suppose you retire at 62 and leave a large 401(k) untouched until age 73. If the account grows, your future RMDs may be larger. Those RMDs may increase taxable income, make more of your Social Security taxable, or push you into Medicare IRMAA surcharge territory.

That does not mean you should drain your 401(k) early.

It means you should test the future tax impact.

This is also where Roth conversions may come in.

A Roth conversion means moving money from a traditional pre-tax account into a Roth account and paying taxes on the converted amount now. Future qualified Roth withdrawals may be tax-free.

For some retirees, the years after retirement but before Social Security and RMDs begin may be lower-income years. Those years may create an opportunity to convert some 401(k) or IRA money to Roth.

But Roth conversions can also become a tax trap.

They may increase taxable income, trigger Medicare IRMAA, reduce health insurance subsidies before Medicare, or create a tax bill that is larger than expected.

That is why conversions should be tested carefully.

You should ask:

- What tax bracket am I in now?

- What tax bracket might I be in later?

- When do RMDs begin?

- Should I take withdrawals before RMDs?

- Should I convert some money to Roth?

- Will conversions affect Medicare premiums?

- How will this affect a surviving spouse?

- How will heirs be taxed?

- Can I pay conversion taxes from non-retirement assets?

Taxes should not be an afterthought.

A Retirement Readiness Review can help compare withdrawal and Roth conversion strategies before RMDs begin.

- Traditional 401(k) withdrawals are generally taxable.

- RMDs can force future taxable withdrawals.

- Roth conversions may create future tax flexibility.

- Conversions can also trigger tax and Medicare surprises.

- Tax planning should happen before the rollover or withdrawal decision.

5. Your 401(k) Decision Should Be Tested Inside Your Full Retirement Plan

The fifth and most important point is this: your 401(k) decision should not be made in isolation.

Your 401(k) is only one piece of the retirement puzzle.

It should be coordinated with:

- Social Security

- Pensions

- IRAs

- Roth accounts

- Taxable brokerage accounts

- Cash reserves

- Annuities

- Healthcare costs

- Medicare premiums

- Taxes

- Estate planning

- Spouse protection

- Market risk

- Inflation

- Required minimum distributions

This is why generic advice often fails.

One person may be better off leaving the 401(k) in the plan. Another may benefit from rolling it to an IRA. Another may need partial withdrawals. Another may need Roth conversions. Another may need to preserve the account for later and use taxable money first.

The best choice depends on what the full plan says.

A strong retirement plan should test:

- Leave the 401(k) where it is.

- Roll the 401(k) to an IRA.

- Use the 401(k) for monthly income.

- Use taxable accounts first.

- Do Roth conversions.

- Delay Social Security.

- Claim Social Security earlier.

- Build a cash reserve.

- Create guaranteed income.

- Plan for one spouse dying first.

- Plan for market downturns.

- Plan for RMDs and taxes.

That is how you move from guessing to decision-making.

For example, rolling your 401(k) to an IRA may make sense if it improves investment choice, simplifies income planning, and creates better Roth conversion flexibility.

Leaving your 401(k) alone may make sense if the plan has excellent low-cost options and you do not need complicated withdrawals yet.

Taking withdrawals may make sense if you are trying to fill a low tax bracket or reduce future RMDs.

Preserving the account may make sense if you have other income sources and want the 401(k) to grow.

None of these choices is automatically right.

The decision should be based on your actual numbers.

A Retirement Readiness Review can help compare each option so you understand the trade-offs before moving your retirement savings.

- Your 401(k) decision should fit your full retirement plan.

- Rollovers, withdrawals, and Roth conversions should be tested.

- Social Security, taxes, Medicare, and RMDs all matter.

- Spouse protection and estate planning should be included.

- The best answer depends on your numbers, not a rule of thumb.

Conclusion

So, what should you do with your 401(k) after you retire?

The honest answer is: it depends.

You may leave it in your old employer’s plan. You may roll it to an IRA. You may use it for retirement income. You may convert some of it to Roth over time. You may coordinate withdrawals with Social Security, taxes, Medicare, and required minimum distributions.

The mistake is making the decision too quickly.

Your 401(k) may be one of the most important assets in your retirement plan. It can affect your income, taxes, investment risk, spouse protection, estate planning, and long-term flexibility.

The right decision should be based on your full retirement picture.

If you’re within a few years of retirement or recently retired, a Retirement Readiness Review can help. We’ll look at your 401(k), IRAs, Social Security, taxes, income needs, Roth conversion opportunities, RMDs, and withdrawal strategy so you can decide what to do with confidence.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before making a decision that could affect the rest of your retirement.

FAQs

Should I roll my 401(k) into an IRA after I retire?

Maybe. Rolling your 401(k) into an IRA may provide more investment options, more withdrawal flexibility, and easier tax planning. But it is not always best. Some 401(k) plans have low costs, strong investment options, and useful protections. The decision should be compared before moving money.

Can I leave my money in my 401(k) after retirement?

In many cases, yes. Some employer plans allow retired employees to leave money in the plan. Whether that is best depends on the plan’s fees, investments, withdrawal rules, service quality, and how the account fits your retirement income strategy.

Do I have to take money out of my 401(k) after retirement?

Not immediately in every case. But required minimum distributions generally begin for many retirement accounts starting with the year you reach age 73. Traditional 401(k) withdrawals are generally taxable, so RMD planning should be included in your retirement plan.