Will Your Spouse Be Okay If Something Happens to You?

Most couples spend years planning for retirement while both spouses are alive. They think about Social Security, pensions, investment withdrawals, travel, taxes, healthcare, and whether they’ve saved enough.

But there’s one question that may matter more than almost anything else:

Will your spouse be okay if something happens to you?

It’s not a fun question. Nobody enjoys thinking about death, illness, disability, or one spouse being left alone. But if you’re married and nearing retirement, this question needs to be answered before life forces it on you.

In this article, we’ll walk through five important areas couples should review to make sure the surviving spouse is protected, prepared, and financially secure.

Short on time? Here is the Key Point / Summary

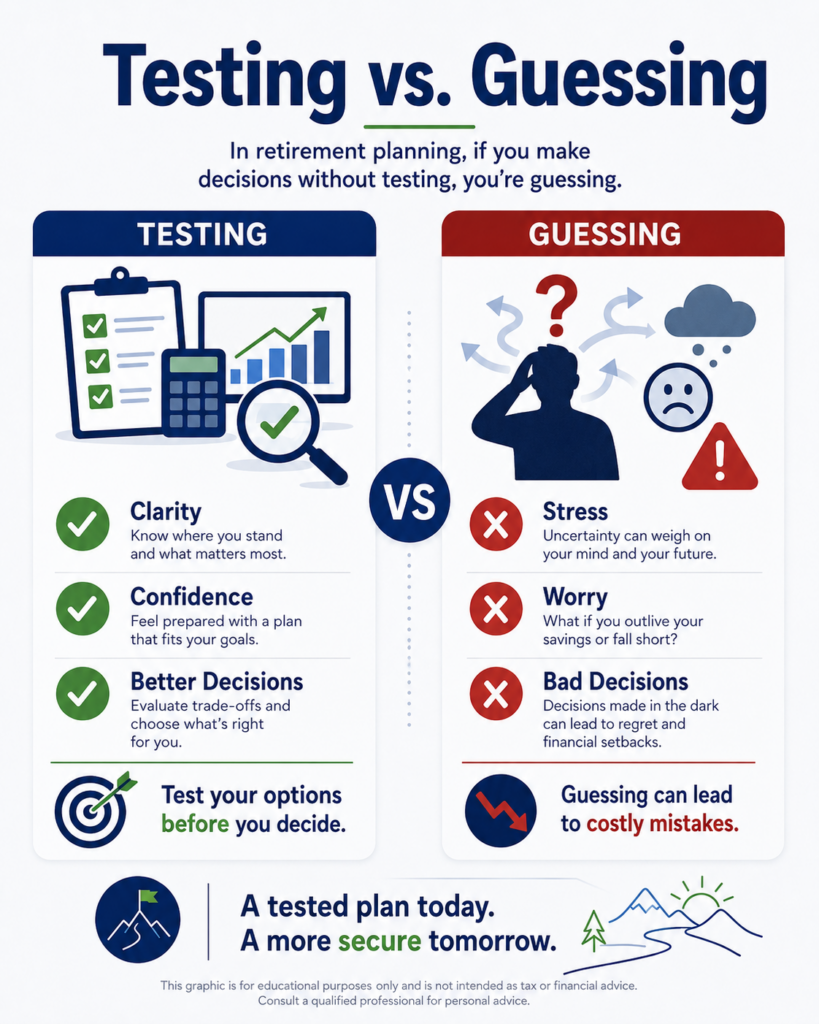

Making sure your spouse will be okay means testing what happens if one spouse dies, becomes disabled, or can no longer manage the financial plan.

Here are the five key things we’ll cover:

- Know what income continues and what income stops.

- Review Social Security and pension survivor benefits.

- Make sure your spouse understands the financial plan.

- Check beneficiaries, estate documents, and account access.

- Test the surviving spouse scenario before something happens.

The biggest mistake is assuming everything will be fine because the retirement plan works while both spouses are alive. A plan that works for two people may not work the same way for one person.

If you’re within a few years of retirement, a Retirement Readiness Review can help test what happens to income, taxes, investments, Social Security, pensions, and expenses if one spouse dies first.

Will Your Spouse Be Okay If Something Happens to You?

Your spouse may be okay if your plan has been tested for survivor income, taxes, account access, healthcare costs, and household expenses.

But if the plan only works while both spouses are alive, there may be hidden problems.

When one spouse dies, several things can change quickly:

- One Social Security check may go away.

- Pension income may reduce or stop.

- Taxes may become less favorable.

- Investment withdrawals may need to increase.

- Medicare premiums may change.

- Household expenses may not drop as much as expected.

- The surviving spouse may have to manage finances alone.

That’s why the better question is not just, “Do we have enough to retire?”

The better question is:

Will the surviving spouse still be financially secure if one of us is gone?

1. Know What Income Continues and What Income Stops

The first step is knowing exactly what income continues and what income stops if one spouse dies.

This is the foundation of survivor planning.

Many couples look at their current retirement income and assume that most of it will continue. But that may not be true.

Your retirement income may include:

- Social Security

- Pension income

- Investment withdrawals

- Annuity income

- Rental income

- Part-time work

- Business income

- Interest and dividends

- Required minimum distributions

Some of that income may continue. Some may change. Some may stop completely.

For example, if both spouses are receiving Social Security, the surviving spouse generally does not keep both checks. The survivor may continue receiving the higher benefit, but the smaller benefit may disappear.

That can be a major income drop.

If one spouse has a pension, the surviving spouse’s income depends on the pension payout option. A single-life pension may stop when the pension holder dies. A joint-and-survivor pension may continue some or all of the income to the surviving spouse.

If one spouse works part-time in retirement, that income may stop.

If an annuity is involved, the survivor benefit depends on the contract. Some annuities continue income to a spouse. Others may not. Some may have refund features, death benefits, or period-certain payments. Others may provide income only for one life.

Investment income may continue, but the withdrawal rate may need to change if other income drops.

This is where couples need to get specific.

You should create a simple survivor income list:

- Income source

- Current monthly amount

- What happens if husband dies first

- What happens if wife dies first

- Whether income continues, reduces, or stops

- Whether the survivor can access it easily

This is not complicated, but it is powerful.

For example:

- Social Security: one check may go away.

- Pension: depends on survivor election.

- IRA withdrawals: may continue but taxes may change.

- Annuity income: depends on contract terms.

- Rental income: may continue if the property is owned and managed properly.

- Part-time work: likely stops if the worker dies or becomes disabled.

Once you know what income remains, you can compare it to the survivor’s expenses.

That’s where the truth shows up.

A Retirement Readiness Review can help organize all income sources and test whether the surviving spouse has enough income after the first death.

- Don’t assume all retirement income continues.

- One Social Security check may go away.

- Pension income depends on the payout option.

- Annuity income depends on the contract.

- Survivor income should be listed and tested before retirement.

2. Review Social Security and Pension Survivor Benefits

The second step is reviewing Social Security and pension survivor benefits.

These two decisions can have a huge impact on the surviving spouse.

Start with Social Security.

For many couples, Social Security is one of the largest sources of guaranteed retirement income. But when one spouse dies, the household does not usually continue receiving both benefits.

That means Social Security claiming decisions should be made as a couple.

If the higher-earning spouse delays Social Security, that may increase the monthly benefit. It may also increase the potential survivor benefit for the spouse who lives longer.

This can be especially important when one spouse has a much lower Social Security benefit.

For example, suppose one spouse’s benefit is $3,200 per month and the other spouse’s benefit is $1,600 per month. While both are alive, the household receives $4,800 per month. But if one spouse dies, the survivor may be left with only the larger benefit.

That means household Social Security income could drop from $4,800 to $3,200.

That is a $1,600 monthly income loss.

The surviving spouse may still have many of the same household expenses.

The mortgage may stay the same. Property taxes may stay the same. Home insurance may stay the same. Utilities may drop a little, but probably not by half. Vehicle expenses, groceries, healthcare, and home maintenance may still be significant.

That’s why Social Security survivor planning matters.

Next, review pensions.

If you or your spouse has a pension, the payout choice may be one of the most important retirement decisions you make.

Common pension options may include:

- Single-life payout

- 100% joint-and-survivor payout

- 75% joint-and-survivor payout

- 50% joint-and-survivor payout

- Period-certain option

- Lump sum option

A single-life pension may provide the highest monthly income while the pension holder is alive, but it may stop at death.

A joint-and-survivor option usually pays less while both spouses are alive, but it can protect the surviving spouse later.

That trade-off must be tested.

The question is not simply, “Which option pays the most today?”

The better question is:

Which option protects the household best over both lifetimes?

A Retirement Readiness Review can help compare Social Security claiming strategies and pension payout options before permanent decisions are made.

- Social Security should be planned as a household decision.

- The surviving spouse may receive the higher benefit, not both benefits.

- Pension survivor options can protect or expose the surviving spouse.

- The highest pension check may not be the safest option.

- Social Security and pension decisions should be tested together.

3. Make Sure Your Spouse Understands the Financial Plan

The third step is making sure your spouse understands the financial plan.

This may be the most overlooked part of survivor planning.

In many marriages, one spouse handles most of the financial decisions. That may work while both spouses are healthy and alive. But it can create a serious problem if the financially involved spouse dies first, becomes disabled, or experiences cognitive decline.

The other spouse may be left asking:

- Where are the accounts?

- How do I access the money?

- Who do I call?

- Which bills are due?

- What income should I expect?

- What should I do with investments?

- Should I sell the house?

- How much can I spend?

- What should I not touch?

- Who can I trust?

That is a terrible position to leave someone in.

Your spouse does not need to become a financial expert. But they do need to understand the basics.

At a minimum, both spouses should know:

- Where the income comes from.

- Which accounts exist.

- How much cash is available.

- How bills are paid.

- Where passwords and documents are stored.

- Who the trusted advisor, CPA, and attorney are.

- What insurance policies exist.

- What debts exist.

- What happens to Social Security.

- What happens to pension income.

- What investment accounts are used for income.

- What not to do immediately after a death.

That last point matters.

After losing a spouse, people are vulnerable. They may be grieving, overwhelmed, confused, or pressured by family members, salespeople, or well-meaning friends.

The surviving spouse needs a simple plan that says:

- Don’t make major decisions immediately unless necessary.

- Don’t sell investments in a panic.

- Don’t move money because someone pressures you.

- Don’t cancel insurance without reviewing it.

- Don’t make large gifts before understanding the plan.

- Call these trusted professionals first.

- Use this account for short-term cash needs.

One of the best gifts you can give your spouse is a plan they can understand.

Not a pile of statements.

Not a complicated spreadsheet.

Not a password-protected mess nobody can follow.

A simple survivor roadmap.

That roadmap should explain:

- Monthly income

- Monthly expenses

- Account locations

- Important contacts

- Insurance policies

- Beneficiary information

- Tax considerations

- Investment withdrawal instructions

- Emergency cash access

- Estate documents

A Retirement Readiness Review can help simplify the retirement income plan so both spouses understand what to do if something happens.

- Both spouses should understand the basic plan.

- One spouse should not be left financially helpless.

- Important accounts, contacts, and documents should be organized.

- The survivor should know what not to do in a panic.

- A simple roadmap can reduce stress during a painful time.

4. Check Beneficiaries, Estate Documents, and Account Access

The fourth step is checking beneficiaries, estate documents, and account access.

This is not exciting work, but it is essential.

Even a good retirement plan can create problems if the paperwork is wrong.

You should review beneficiary designations on:

- IRAs

- 401(k)s

- 403(b)s

- Roth IRAs

- Life insurance

- Annuities

- Bank accounts

- Brokerage accounts

- Health savings accounts

- Employer benefits

Beneficiary designations matter because they often control where assets go after death. In many cases, they can override what a will says.

That means outdated beneficiaries can create serious problems.

For example, if an old retirement account still lists a former spouse, deceased family member, or outdated beneficiary, the money may not go where you intended.

You should also review estate documents, including:

- Will

- Revocable living trust, if applicable

- Durable power of attorney

- Healthcare power of attorney

- Living will or advance directive

- HIPAA authorization

- Trust funding documents

- Property titling

These documents are not just for death. They also matter if one spouse becomes incapacitated.

If you are alive but unable to make decisions, your spouse may need legal authority to act for you. Without proper documents, they may face delays, court involvement, or unnecessary stress.

Account access matters too.

Your spouse should know:

- Where accounts are held.

- How to access online accounts.

- Where passwords are stored.

- Which bills are automatic.

- Which bills require manual payment.

- Where tax returns are located.

- Where insurance policies are located.

- Where estate documents are stored.

- Who to call if something happens.

This is also a good time to simplify.

If you have old 401(k)s, unused bank accounts, scattered investment accounts, outdated insurance policies, or accounts your spouse does not know about, cleanup may be wise.

The more complicated the financial life, the harder it may be for the survivor.

Simplicity is not about being unsophisticated. It is about reducing unnecessary stress.

You should also review titling.

Are accounts individually owned, jointly owned, trust-owned, or beneficiary-designated? Does the titling match the estate plan? Does your spouse have legal access if needed?

This is where a financial advisor, estate attorney, and CPA may need to work together.

A Retirement Readiness Review can help identify the financial accounts and beneficiary issues that should be coordinated with your legal documents.

- Beneficiary designations should be reviewed regularly.

- Beneficiaries may override a will.

- Estate documents should cover death and incapacity.

- Your spouse should know how to access accounts and documents.

- Simplifying accounts can make life easier for the survivor.

5. Test the Surviving Spouse Scenario Before Something Happens

The fifth and most important step is testing the surviving spouse scenario before something happens.

This is where real planning happens.

A retirement plan should not only answer, “Can we retire?”

It should also answer:

Can my spouse stay retired if I’m gone?

That question changes everything.

You should test both scenarios:

- What happens if you die first?

- What happens if your spouse dies first?

The numbers may look very different depending on who dies first.

For example, if one spouse has the larger Social Security benefit, a pension, or handles the investments, the impact may be different than if the other spouse dies first.

A good survivor test should include:

- Remaining Social Security income

- Pension survivor income

- Annuity survivor income

- Investment withdrawals

- Taxes

- Medicare premiums

- Healthcare costs

- Housing costs

- Debt

- Life insurance

- Emergency cash

- Estate settlement costs

- Long-term care concerns

- Survivor spending needs

Taxes deserve special attention.

When both spouses are alive, they may file jointly. After one spouse dies, the survivor may eventually file as single. That can create higher taxes even if income does not drop much.

This is sometimes called the widow’s penalty or survivor tax penalty.

For example, the surviving spouse may have the higher Social Security benefit, pension survivor income, IRA withdrawals, investment income, and required minimum distributions. But they may no longer have married filing jointly tax brackets.

That can increase the tax burden.

Medicare premiums may also become an issue if the surviving spouse’s income crosses IRMAA thresholds as a single filer.

This is why survivor planning is connected to Roth conversions, IRA withdrawal strategies, Social Security timing, pension elections, and annuity choices.

None of these decisions stands alone.

For example:

- Delaying the higher earner’s Social Security may improve survivor income.

- Choosing a joint pension option may protect the surviving spouse.

- Roth conversions during married years may reduce future tax pressure.

- Life insurance may fill an income gap.

- Cash reserves may give the survivor breathing room.

- Simplified accounts may reduce confusion.

- A written income plan may prevent emotional decisions.

The goal is not to predict everything perfectly.

The goal is to avoid obvious problems.

A Retirement Readiness Review can help test the survivor scenario so you can see whether your spouse would truly be okay.

- Test what happens if either spouse dies first.

- Survivor income may be lower than expected.

- Taxes may become less favorable for the surviving spouse.

- Social Security, pensions, annuities, and investments should be coordinated.

- A plan that protects the survivor creates real peace of mind.

Conclusion

So, will your spouse be okay if something happens to you?

That question deserves a real answer.

Not a guess. Not a hope. Not “I think so.”

A real answer.

Your spouse may be okay if income continues, expenses are manageable, taxes are planned for, accounts are accessible, documents are organized, beneficiaries are correct, and the survivor understands the plan.

But if you have not tested the survivor scenario, there may be hidden risks.

One Social Security check may go away. Pension income may stop or reduce. Taxes may rise. Investment withdrawals may need to increase. The surviving spouse may be left managing accounts they do not understand during one of the hardest times of life.

That is preventable.

If you’re married and within a few years of retirement, survivor planning should be part of your retirement plan now. Not later.

A Retirement Readiness Review can help test whether your spouse would be okay if something happened to you. We’ll look at income, taxes, Social Security, pensions, investments, insurance, account access, and survivor needs so you can make decisions with more confidence.

You don’t have to move your money. You don’t have to buy a product. You just need clarity before life makes the decisions for you.

FAQs

What happens to retirement income when one spouse dies?

Retirement income may change significantly. One Social Security check may go away, pension income may continue, reduce, or stop, and investment withdrawals may need to increase. Taxes may also become less favorable for the surviving spouse.

How can I make sure my spouse is financially protected?

Start by reviewing survivor income, Social Security, pension options, life insurance, beneficiaries, estate documents, account access, and monthly expenses. Then test whether the surviving spouse can maintain their lifestyle if one spouse dies first.

Should both spouses understand the retirement plan?

Yes. One spouse may handle most of the details, but both spouses should understand the basic income plan, where accounts are located, who to call, what income continues, and what steps to take if something happens.